Case study by Legal & General Investment Management

| Author | Catherine Ogden, Manager, Sustainability & Responsible Investment |

|---|---|

|

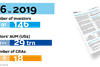

Market participant |

Asset Manager |

|

Total AUM |

US$934.2 billion (as at June 2018) |

|

FI AUM |

US$227 billion (active); US$261.2 billion (passive) |

|

Operating country |

UK, US and Hong Kong |

Action areas:

- Materiality of ESG factors

- Organisational approach

- Time horizon

The investment approach

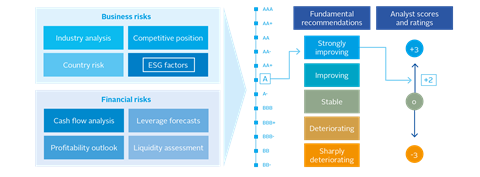

Across asset classes, Legal and General Investment Management (LGIM) sees unmanaged ESG factors as posing potential risks and opportunities, which can have a material impact on the performance of investments. In FI, we look for risks that could affect the credit quality of a bond and therefore its returns, as well as how ESG integration in fundamental credit analysis may unlock opportunities through identifying market mispricing, for example.

However, it is not easy to discern whether an ESG factor will affect credit quality. To conduct a review of our ESG framework, we had an open discussion about materiality with ESG, credit and equity professionals. We brought together working groups to debate materiality at a sector level and then upgraded our framework of analysis/tools accordingly. This helped to improve knowledge across the board and equip investment teams to apply ESG analysis to a specific investment security and strategy.

The result is that the same ESG assessment can yield different outcomes across credit portfolios, as well as credit and equity investment decisions.

For example, certain issuers are not considered in our Buy and Maintain funds because of potential longer-term ESG risk, but may still be held by other funds. Others may be held in a core fund despite a poor ESG profile because the ESG risk is not seen as likely to materialise as a financial risk that would affect credit quality or default risk – or indeed because the risk is already priced. However, for our Future World fund range – where we go further in addressing ESG issues – we would only incorporate a company with a weak ESG status if we expect to see improvements as a result of successful engagement.

We have not made organisational changes to our investment processes but have given more responsibility to the credit team and individual credit analysts:

- We have gone through a year-long process of reviewing our ESG structures, processes and tools to improve the robustness of our framework for assessment and to broaden understanding and knowledge of ESG across all areas of the business.

- The review has been a joint effort by our active investment teams and ESG professionals. The credit team has been particularly involved as we sought to improve the way in which our ESG tools and processes help to meet their requirements. Responsibility for reviewing the outputs of the tool on an ongoing basis sits across all teams, requiring cross-team discussion and collaboration. Responsibility for assessing the implications at the issuer and issuance levels sits with credit analysts.

- This approach has also involved drawing on the expertise of broader teams across the company – from data and technical teams to sales and distribution, and we have extended formal and informal training for these teams.

- Although the investment process within our core funds has not changed, we now have a more systematic, sophisticated and structured framework for assessing the materiality of ESG factors and monitoring changes, and have developed a culture in which ESG is valued and supported.

- As the ESG landscape evolves, it is important to adapt our approach and processes, driven by increasing regulatory and fiduciary pressures, growing evidence of the relationship between ESG and corporate financial performance, and greater client demand for evidence of ESG integration, particularly as ESG data and analytics improve.

The investment process

We believe that a company’s ESG profile is most comprehensively assessed by looking at two drivers of investment returns. The first is how business activities can impact the bottom line; for example, the risk of pollution by a miner leading to the loss of a licence to extract resources from a country. The second is how long-term trends may determine consumer demand for products and services; for example, the implications of the global battle against plastic for petrochemical companies and demand for oil.

Thinking about these issues is not new; however, we have been working to develop and enhance our tools and processes for assessing how companies are managing ESG factors, as well as how to integrate these findings into active fund management. This has involved:

- Firstly, evaluating long-term themes; in our working groups on energy, demographics, technology and politics, we generate insights into how companies are adapting to a rapidly-changing world. Secondly, through considering LGIM’s Active ESG View.

- Our Active ESG View seeks to identify and represent the ESG risks and opportunities within each company. It is an essential component of the overall active research process. It takes the inputs that form the LGIM ESG Score as a starting point for assessing ESG quality, and then goes a step further by incorporating additional quantitative and qualitative inputs.

- It involves teams leveraging their sector expertise, knowledge of company dynamics and corporate access. This leads to a status being created for each company ranging from very strong to very weak. The degree to which this ESG View drives bond and equity selection will depend on the fund design.

- For our core active products, the Active ESG View is fully integrated into how we fundamentally assess a company and is considered alongside all other components of investment analysis. Within core products, it remains at the portfolio manager’s discretion as to whether a company with a weak ESG status offers the necessary level of return for the given level of risk.

- However, for our Future World fund range – where we go further in addressing ESG issues – we would only incorporate a company with a weak ESG status if we expect to see improvements in the future as a result of successful engagement.

The investment outcomes

Digital Realty (DLR) is an example of a corporate issuer we consider appropriate for core funds and our Future World fund range, based on considering ESG factors as part of our credit analysis. DLR is a real estate investment trust that invests in data centres and provides colocation and peering services (see figure below).

Long-term themes: we believe the fundamentals of the alternative property space that DLR operates in (data warehouses) are strong. DLR is doing more than adapting to the rapidly-changing world, with demand for the company’s services driven by long-term technology trends, the cornerstone of LGIM’s long-term view on the issuer.

Active ESG View for our Core Funds: the company performs well on our governance assessment, while environmental and social performance is weighed down by a lack of disclosure. However, our meetings with the company and recent site visits have provided valuable insights into its environmental and social practices. We were particularly encouraged to hear of the company’s initiatives to improve energy efficiency (for example, by using locally-focused air conditioning and using river water in the cooling process), its targets for renewable energy procurement, and move from diesel back-up generators to batteries. We believe that focusing on energy efficiency can create customer value for DLR and translate into greater profitability. Overall, we view the sector as low risk.

Active ESG Views for Future World Credit Funds: LGIM considers DLR to comfortably meet the standard required; we see long-term trends as beneficial to the sector, and we are reassured by the responsibility DLR is assuming to manage environmental impacts. DLR issued its first green bond in June 2015 (the first data centre REIT to do so), allocating $493 million of net proceeds to nine global green building projects. Moving forward, we expect issuance of a green bond from the company; if pricing is appropriate, we will consider including it in our Future World Credit Funds.

Engagement with the company: although we consider the sector to have relatively low ESG risk, and despite being reassured about environmental and social practices during our visits, we are asking the company for better disclosure in these areas. This will enable us to monitor and evaluate company ESG performance consistently and regularly, and will provide the wider market with the tools to do so. If the ESG risk status changes, we will be better equipped to factor this into our credit assessment in a timely manner.

LGIM’s credit recommendation: as stated above, we believe that DLR’s global positioning stands to benefit from broader developments in technology and strong global demand for data centres. It has solid credit fundamentals and is attractive on a relative value basis versus its peers. We also think that the company’s focus on energy efficiency and sustainability has medium to long-term benefits for its stakeholders and can ultimately create value for customers. DLR has made a conscious effort to increase the amount of renewables in its fuel mix (doubling since 2014), and a continuation along these lines could help to increase asset values and reduce operating costs in the future. The potential launch of a new green bond underlines the company’s commitment to green initiatives.

Key takeaways

The key takeaways from our work on integration to date are:

- that the process and path to integration is not linear;

- if starting out, be prepared for bumps along the way; if already up and running, be prepared to review your approach, take on board criticism and listen to suggestions from colleagues and stakeholders;

- a structured framework of analysis and application for ESG is extremely valuable, but build in flexibility so that it can evolve as data, information, understanding of ESG and the nature of risks and opportunity change;

- be prepared for ESG outcomes to be applied differently across portfolios and investment strategies;

- build efficient and accessible tools that are intuitive for all relevant teams across the business; and

- draw on expertise from across investment teams and from around the business, including technical teams.

Download the report

-

Shifting perceptions: ESG, credit risk and ratings: part 3 - from disconnects to action areas

January 2019

ESG, credit risk and ratings: part 3 - from disconnects to action areas

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

- 11

- 12

- 13

- 14

- 15

Currently reading

Currently readingCase study: Legal & General Investment Management

- 16

- 17

- 18

- 19

- 20

- 21

- 22

- 23

- 24

- 25