Case study by Kartesia

Climate change is one of the highest priority ESG issues facing investors globally. As reported by the PRI in its recent Investor action on climate change report, in 2017 nearly 400 investors – representing US$22 trillion in AUM – stood by the Paris Agreement. The group urged governments to drive investments in the low-carbon transition and support climate reporting frameworks such as the recommendations of the Financial Stability Board Task Force on Climate-related Financial Disclosures. As an investment fund working with those investors, we believe that it is our fiduciary duty to incorporate climate change concerns into our investment process. The challenge is to continue to engage on climate issues and subsequently maintain our position as a private debt specialist, in a sector where access to management and influence on companies might be more restricted than for private equity sponsors.

Kartesia’s perspective on ESG

We are confident that companies with high ESG standards are typically managed better, have fewer business risks and ultimately deliver better value. Responsible investment is therefore a vital part of our investment philosophy and process. We launched in 2013 and when starting to fundraise for our first Credit Opportunities Fund, our Limited Partners requested that we engage on responsible investing and become a signatory of the PRI.

With regards to climate change, we decided to assess the climate change footprint of our portfolio, the reason for which is two-fold: a) as a basis for informational exchange with our portfolio companies; and b) to report on this pressing topic to our LPs.

Tackling climate change using models

Our mission is to provide liquidity and credit solutions to European small/mid-market companies. We currently observe a relatively low level of ESG reporting by those companies. Additionally, our position as a lender may not always lead to discussions with management or increased ESG reporting, as it is, unfortunately, not often front-ofmind for target companies, particularly in secondary deals. We decided to compensate for the lack of ESG data from our portfolio companies by using statistical models.

Since 2015, we have teamed up with the service provider Sustainalytics to annually assess the carbon footprint of our portfolio companies. As our portfolio comprises private companies that seldomly report on carbon emissions, Sustainalytics uses statistical models to estimate the carbon footprint of the total portfolio and compare it with an appropriate benchmark. This model considers several criteria for each portfolio company, including size, industry and FTE, and estimates the overall weighted carbon intensity of each fund. The resulting report allows us to drill down to the sector and peer level.

Methodology

To address the reporting gap and help mitigate uncertainty around carbon performance at the portfolio level, Sustainalytics has developed a model to estimate Scope 1 (direct) and Scope 2 (indirect, associated with purchased energy) greenhouse gas emissions for companies.

Modelled groups

A modelled group refers to either a sub-industry or peer group for which the estimation model is developed for Scope 1 and Scope 2 respectively. A specific scenario for each modelled group in the coverage universe is applied, ensuring that relationships between input factors and greenhouse gas emissions are effectively captured. As the global population of reporting companies has increased, Sustainalytics is able to validate more models at a more comparable sub-industry level.

Estimation model

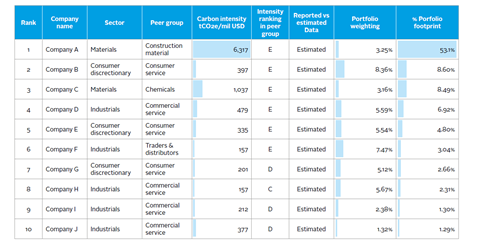

The estimation model incorporates three different factors per modelled group, using three input variables: total revenue, gross property and plant & equipment (PP&E), and employee count. Input factors are average emissions per million USD total revenue, average emissions per million USD PP&E and average emissions per employee. These factors are then multiplied by respective total revenue, gross PP&E value and employee count of the estimated company. A last step comprises Sustainalytics’ final estimate based on the average of the three different factor outcomes. While the service provider performed extensive correlation analysis to determine specific weights for these factors, the results were inconclusive. Hence the three factors are equally weighted and averaged to determine a final emissions estimate. The emissions estimates per company can also be weighted based on the total portfolio contribution of the carbon footprint (see Table 1). Important insights are gained from comparing footprint contribution associated with the loan amount of a portfolio company. This helps us prioritize our dialogue with polluters on a relative basis.

When determining a benchmark to compare the results, Sustainalytics offered several in-house indexes with carbon metrics. However, our portfolio did not show sufficient overlap with any of these indexes. Further investigation regarding the geographical zone of our investments led to the decision that MSCI Europe would be the most appropriate benchmark.

Outcome and actions taken

Sustainalytics assesses the carbon footprint of our portfolio annually. The report is first shared and discussed internally. High-emitting borrowers are discussed in more detail and contacted by Kartesia’s responsible investment manager to conduct additional assessment and interpret the results.

We also discuss the results with Sustainalytics by comparing them to market, peer and previous years’ reporting. Based on that, we issue a final version of the carbon assessment report. An example of adjustment that we made this year is adjusting down the carbon footprint of one of our high-emitting portfolio companies as it decided to offset emissions by purchasing green certificates. The final version of the report is then shared internally and made available to our LPs.

We monitor the yearly results of our carbon assessment report. For the years 2015-2018, we observed a slight improvement in the weighted carbon intensity of our portfolio compared to the benchmark. However, we do not market any improvement in our carbon emissions as the estimation model used is quite dynamic and is not an exact science. This report is a good starting point to get a sense of our carbon intensity, but it is too early to claim an improvement against a virtual benchmark.

Looking ahead

Our partnership with Sustainalytics is still in its early working stages and we are continuously learning about the process of analysing and processing our portfolio. The estimation model used is evolving substantially and we believe it is an excellent starting point to get a clearer sense of our carbon footprint and to make progress in discussions with companies currently having the most negative impact on emissions in the portfolio. Today, it is vital that our investors have the relevant information required to monitor their footprint or to reach carbon neutrality by balancing their investments via carbon credits. The next logical steps are to have the carbon footprint factored into our investment decisions – in the pre-investment and monitoring phase.

Downloads

Private-debt-case-study_Kartesia

PDF, Size 0.11 mb

Spotlight on responsible investment in private debt

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

Currently reading

Currently readingCase study: Kartesia

- 9

- 10