The PRI and Baker McKenzie undertook a review during mid-2017 of how the TCFD’s voluntary recommendations integrate into existing regulation and soft law in Brazil, Canada, the EU, Japan, the United Kingdom and the USA.

Focus of the market reviews

The review papers produced for each market consider:

- private sector regulation – disclosure regulation for various kinds of companies as well as policy statements or guidance;

- climate change-related aspects of pension fund/investor regulation, and discuss the relevance of the TCFD recommendations in the context of each market’s regulation and policy for those companies and investors/funds.

Summaries of each country’s Nationally Determined Contributions (NDCs) associated with the Paris Agreement are also included as Appendices to this report.

Overall findings across markets

Each market has taken a different approach to regulation and policy dealing with the disclosure of climate-related risks. Despite these differences, the review found that the TCFD’s recommendations would be likely to both:

- assist companies in understanding and moving towards best practice climate risk disclosure as part of broader financial disclosures;

- assist investors in assessing portfolio risk assessment and providing information on this to clients and beneficiaries, through normalising and improving the consistency of corporate climate risk disclosures.

The PRI’s perspective on Baker McKenzie’s findings

Overall, in the six markets reviewed by Baker McKenzie, existing material risk disclosure regulation and/or guidance for companies and investors clearly either requires or encourages material financial risk disclosures.

Baker McKenzie’s analysis highlights that TCFD’s framework will bring consistency and comprehensiveness to material risk disclosures with respect to climate change. Better climate disclosure will assist investors significantly in understanding the financial impacts of climate change on their investments.

Action PRI will take to drive TCFD implementation

In 2017-18, the PRI will support investors in enhancing climate disclosure:

- Active ownership: We will convene collaborative global investor engagement to encourage companies to adopt the TCFD fs recommendations. We will also encourage regulators and stock exchanges to endorse these.

- Investment practices: We will encourage investor use of company disclosures that are aligned with the TCFD recommendations, and advance investment practices in assessment and management of climate-related risks and opportunities.

- Investor disclosure: We will update the PRI’s Reporting Framework to align with the TCFD fs guidance for asset owners and asset managers, thereby supporting the quality of investor ESG reporting to clients and beneficiaries.

- Addressing barriers around responsibility investment: The PRI has set out its priorities for the next 10 years in its Responsible Investment Blueprint, published in 2017. These include climate action, supporting investors in incorporating ESG issues and challenging barriers to a sustainable global financial system.

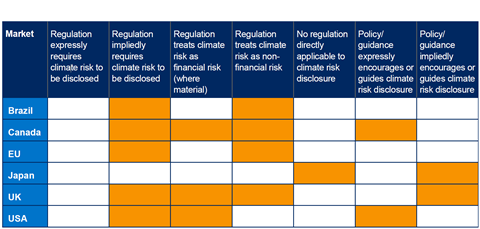

Differences between markets

The table below contains a general summary of how climate-related risk is currently covered in each market’s regulation and policy on corporate disclosure. Note given the differences between the nature of the various corporate and financial sectors in each jurisdiction and how each sector is regulated in each case, the conclusions are intended to provide broad guidance only.

Similarities – climate change is relevant to material financial risk disclosure

Where compulsory financial disclosure rules require disclosure of material financial risks, a company’s disclosures should include any climate change-related financial risks which meet the materiality threshold under those rules.

In all jurisdictions considered, there is no explicit requirement for climate change-related risks to be disclosed by companies as part of mainstream financial filings. In some cases, climate change tends to be considered as a non-material factor. The rigour and detail required for non-material disclosures is generally lesser than that required for mainstream financial filings. From an investor/pension fund perspective, the position is similar, in that there is little or no explicit requirement to consider climate risks to an investment in the markets considered.

However, it is clear that climate change risks will and do have relevant implications for many companies and investors in jurisdictions where material climate change-related risks would be properly categorised as financial risks.

Across markets, TCFD will assist corporate entities and investors

The TCFD’s recommendations for comprehensive risk analysis and disclosure around climate change would be likely to result in:

- corporate entities better understanding the real financial implications of climate-related risks and their potential impacts on business models, strategy and cash flows;

- investors grasping if, and how well, companies are conducting this analysis;

- normalising this analysis as part of good corporate governance in each jurisdiction.

TCFD will enable more consistent disclosures

In all jurisdictions considered, it is evident or likely that climate risk disclosure is not consistent across or within corporate sectors, in part because there is no or limited guidance on the scope of analysis and reporting, on which companies seeking to provide climate risk disclosure can rely. This is one area where adoption of the TCFD recommendations by companies (and governments) has significant potential to educate companies and investors regarding best practice climate disclosure, and lead to more reliable and uniform disclosures being made by companies to which disclosure frameworks apply.

TCFD provides clarity on scope of disclosures

Beyond the issue of consistency, the extent and scope of climate risk analysis companies in each market should undertake is not yet clearly signalled in any of the jurisdictions reviewed. The TCFD recommendations on the information needed by investors to properly assess and price climate-related risks include detailed discussion of forward-facing assessment tools such as scenario analysis. This aspect of the TCFD’s review would be of particular relevance in jurisdictions such as the USA, the UK, Canada and Brazil, which have reasonably comprehensive financial disclosure requirements but where the applicable regulation does not expressly prescribe how climate risks must be considered or disclosed.

TCFD is compatible with existing requirements

Even in jurisdictions where there is limited or no express requirement for, or guidance encouraging, corporate climate risk analysis, adoption of key TCFD recommendations does not conflict with existing disclosure requirements. In these markets, companies may be better positioned for the transition of their economies (as part of the wider global transition to a lower carbon economy) as companies and investors begin to appreciate the risk management benefits of implementing comprehensive climate change risk-related analysis and disclosure, and the consideration of financial risks of ESG factors becomes more comprehensively integrated into business strategy.

Investor demand for climate disclosure is set to continue

We expect that in all markets covered by the review, climate change disclosure requirements will continue to evolve. This will eventually lead to a more consistent and comprehensive coverage of the material financial risks (and opportunities) presented by climate change in corporate disclosures. This evolution is likely to be driven by the global momentum towards lower carbon economies. It will also be fostered by investors increasingly expecting a higher and more consistent standard of climate risk-related disclosure by companies.

Produced in collaboration with Baker McKenzie

![]()

Downloads

TCFD Recommendations: Country reviews

PDF, Size 1.91 mb