Integrated analysis: How investors are addressing ESG factors in fundamental equity valuation focuses on fundamental equity analysis and the contribution that analysis of ESG factors can make towards an accurate valuation of a listed company.

The report showcases integrated analysis from several of the world’s leading financial institutions. It is designed to give an indication of the nature and quality of analysis available to investors seeking to make integrated investment decisions.

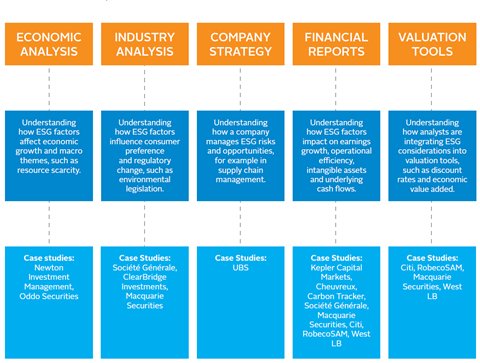

The structure of the document follows that of a stylised stock review. We use five stages from analysis of the economies in which a company operates, through the industries in which it operates, the way it conducts its operations, the financial impacts of those operations and finally the valuation tools used. While few of the pieces we assessed followed this process in its entirety, this structure allows us to highlight innovative analysis and common practices at each stage.

The review found advanced use of integrated analysis in all aspects of fundamental equity valuation, particularly in industry analysis, forecasting earnings and adjusting discount rates. These integrated approaches to estimating fair value point towards significantly improved valuation models that account for scarcity of resources, future regulatory directions and timeframe tensions.

Conclusions

Good news

There can be no doubt that the high quality integrated analysis that has been demanded by investors for so many years is now being delivered. Questions around structure, utilisation, resourcing and payment should now take the place of those which focus on whether it can be done.

Mainstream ready

Nearly all the analysis followed standard research structures mirroring the research output of any sell-side sector research team or investor. ESG issues may present new risks and opportunities but they are assessed through standard models of business performance and valuation. We believe that any investor could make use of the research we reviewed.

Timeframe tensions

The reliance on traditional valuation tools can create a tension between their relatively short timeframes and the longer timeframes needed for many ESG issues to impact companies. Much of the analysis focused on situations where ESG issues were becoming more urgent or where investors are beginning to look to the longer term.

Resource intensive

ESG information remains more resource intensive to acquire and assess than audited financial information. The difficulty of acquiring consistent, comparable, audited information remains a significant hurdle to integrated analysis.

Disclosure is trailing performance

The quality of reporting remains vital but it was noted that companies are frequently doing more than their public disclosure would suggest. This again raises issues of the resources needed to obtain an accurate picture of company performance.

Context is vital

With different regulatory regimes around the world in terms of disclosure requirements, it was noted that raw ESG data without context can be misleading. Carbon emissions were cited as potentially misleading if the location, carbon-penalising mechanism and any free allowances are not known. Integrating raw data into valuation without that context could prove misleading.

The role of ratings

Although we found widespread agreement on the value of ratings within responsible investment more broadly, they did not feature heavily in these examples of integration. The underlying performance on ESG metrics was instead used directly in assessing business performance and value. The lack of integrated research produced by independent ESG research providers was noted in the review.

Materiality

The identification of material issues remains an art rather than a science. Whilst for some ESG factors there is broad consensus that the issue could have a significant impact on a firm’s performance, the materiality of other aspects depends on individual investors’ processes, investment horizons, risk budgets and performance targets.

Downloads

Integrated analysis: How investors are addressing ESG factors in fundamental equity valuation

PDF, Size 0.91 mb統合分析: 株式のファンダメンタル分析において 投資家が環境、社会、ガバナンス要因 に対応する方法

PDF, Size 1.39 mb통합 분석: 펀더멘탈 주식 밸류에이션 시, 투자자들의 환경, 사회, 지배구조 요소 통합 방법

PDF, Size 1.87 mbAnálise integrada: como investidores estão abordando fatores ambientais, sociais e de governança na avaliação fundamentalista

PDF, Size 1.7 mb