Overview

- This guide provides a quick summary of how an investor can consider environmental, social and governance (ESG) issues when assessing fixed income instruments and their issuers.

- It outlines options for how to include ESG issues when building a fixed income portfolio and when working with issuers on how they manage ESG issues.

- For more information on anything on this page, or responsible investment more broadly please get in touch.

The PRI defines responsible investment as a strategy and practice to incorporate environmental, social and governance (ESG) factors in investment decisions and active ownership.

It complements traditional financial analysis and portfolio construction techniques. Investors need to assess ESG factors that are relevant to issuers, as well as to individual securities.

This guide will take you through the following approaches to managing ESG issues in fixed income:

| CONSIDERING ESG ISSUES WHEN BUILDING A PORTFOLIO (known as: ESG incorporation) | INTERACTING WITH ISSUERS ON ESG ISSUES (known as: active ownership or stewardship) | |||

|---|---|---|---|---|

| ESG factors can be incorporated into existing portfolio construction practices using a combination of three approaches: integration, screening and thematic. | Although not owners of the entities they invest in, fixed income investors are still important stakeholders that can encourage issuers to improve their ESG risk management or develop more sustainable business practices and economic growth models. | |||

| Integration | Screening | Thematic | Engagement | |

| Explicitly and systematically including ESG factors in investment analysis and decisions, to enhance riskadjusted returns. In fixed income investments, the focus is typically on managing downside risk. | Applying filters to lists of potential investments to rule issuers, or specific securities, in or out of contention for investment, based on an investor’s preferences, values or ethics. | Seeking to combine attractive riskreturn profiles with an intention to contribute to a specific environmental or social outcome. Includes green bonds. | Discussing ESG factors with issuers to improve their handling, including disclosure, of such factors. Can be done individually or in collaboration with other investors. Often undertaken across asset classes, though fixed income investors have different access to management and no ownership rights. Engagement differs between sovereign and corporate issuers. | |

Considering ESG issues when building a portfolio (ESG incorporation)

ESG factors can be incorporated into fixed income investment strategies using three approaches: integration, screening and thematic. Investors select between, or combine, these approaches based on their desired outcomes. This may be to enhance their risk-return profile, avoid specific sectors or drive capital towards particular environmental and/or social goals.

The actions investors take to include ESG factors when building a portfolio are covered by Principle 1 of the six Principles for Responsible Investment: “We will incorporate ESG issues into investment analysis and decision-making processes.”

Comparing key characteristics of ESG incorporation approaches in fixed income

| INTEGRATION | SCREENING | THEMATIC | |

|---|---|---|---|

| Gives a more complete picture of the risks and opportunities faced by an issuer | ● | ||

| Is applicable to investors that have no interest in considerations outside of their risk-return profile | ● | ||

| Largely about managing downside risk | ● | ||

| Can fit within existing investment processes | ● | ● | ● |

| Restricts investment in certain industrial sectors, geographic regions or individual issuers, typically for ethical reasons | ● | ● | |

| Non-financially material ESG factors or ethical considerations are incorporated into investment decisions | ● | ● | |

| Directs capital towards issuers or securities that contribute to environmental or social outcomes | ● | ||

| Largely about identifying opportunities | ● |

This table gives a broad overview of some of the differences between the major types of ESG incorporation. It is not a detailed or exhaustive classification.

ESG incorporation across issuer types

| ISSUER TYPE | |||

|---|---|---|---|

| INCORPORATION APPROACH | CORPORATE | SOVEREIGN | SUB-SOVEREIGN |

| Integration | Integrating material ESG factors into credit research and assessments, forecasted financials/ratios and relative value/spread analysis. | Governance and political factors have long been a part of sovereign credit analysis. Social and environmental factors – such as inequality, climate-related risk and the energy transition – are becoming increasingly relevant. | |

| Screening | Filters are applied to lists of potential investments, ruling issuers in or out of contention for investment based on an investor’s preferences, values or ethics. Filters are typically based on including or excluding particular products, services or practices. | ||

| Thematic | Selecting issuers that address sustainability challenges, or securities that fund sustainability projects. These issues might be accredited by specific bond standards (e.g. those for green bonds). | Investing in fixed income securities where the proceeds are used to fund a sustainability project or budget item (e.g. green sovereign bonds) | |

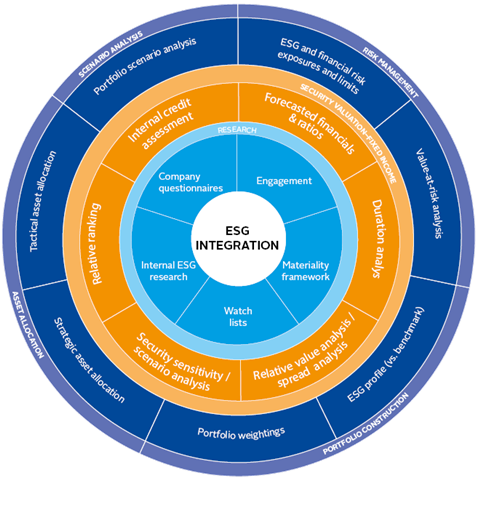

Integration: adding ESG factors to financial analysis

Material ESG factors are identified and assessed alongside traditional financial factors when forming an investment decision about a specific issuer or security, or the overall portfolio structure. In fixed income, this is primarily done to manage downside risk. Investors apply a range of techniques to identify risks that might remain undiscovered without the analysis of specific ESG data and broad ESG trends.

Integration typically has three steps:

- Investment research: Identifying material ESG factors (at the issuer level, as well as for individual securities) that may impact downside risk (or provide topics for engagement).

- Security valuation: Integrating the material ESG factors into financial analysis and valuation, e.g. through internal credit assessments, forecasted financials and ratios, relative ranking, relative value/spread analysis, and security sensitivity/scenario analysis.

- Portfolio management: Including the ESG analysis in decisions about risk management and portfolio construction, e.g. through sector weightings.

Credit ratings

Many ESG factors have traditionally featured in credit rating methodologies, but the role they play is often not well communicated. As part of their commitment to the PRI’s ESG in Credit Risk and Ratings initiative, large global rating agencies are now increasing transparency over how they consider ESG factors as part of their assessments.

Screening: filtering the investable universe

Screening uses a set of filters to determine which issuers, sectors or activities are eligible or ineligible to be included in a portfolio based on an investor’s preference, values or ethics. For example, a screen might be used to exclude the highest carbon emitters from a portfolio, or to target only the lowest emitters. ESG scores can be obtained from specialist ESG service providers, or by creating a proprietary scoring methodology.

| NEGATIVE SCREENING Avoid the worst performers | NORMS-BASED SCREENING Use an existing framework | POSITIVE SCREENING Include the best performers |

|---|---|---|

| Excluding certain sectors, companies or projects for poor ESG performance relative to industry peers, or based on specific ESG criteria, e.g. avoiding particular products/services or business practices. | Screening investments against minimum standards of business practice based on international norms. Useful frameworks include UN treaties, Security Council sanctions, UN Global Compact, Universal Declaration of Human Rights and OECD guidelines | Investing in sectors, companies or projects selected for positive ESG performance relative to industry peers. |

Thematic: allocating capital towards environmental or social outcomes

Thematic investing identifies and allocates capital to themes or assets related to certain environmental or social outcomes, such as clean energy, energy efficiency or sustainable agriculture.

Green bonds

Green bonds are a rapidly-growing category of fixed income securities that finance environmental projects. In 2018, global green bond issuance totalled over US$167.6 billion.1 These might be issued in accordance with various international standards and frameworks for green bonds, including: Green Bond Principles, Green Loan Principles, Climate Bonds Standard or local standards such as Japan’s green bond guidelines and taxonomy. Green bonds have been issued by corporates, sovereigns, supra-nationals, agencies and sub-nationals.

Other types of thematic bonds include social bonds, sustainability bonds and Islamic bonds (sukuk).

Interacting with issuers on ESG issues (active ownership or stewardship)

The actions investors take to encourage the entities they are already invested in to improve their ESG risk management or develop more sustainable practices is covered by Principle 2 of the six Principles for Responsible Investment: “We will be active owners and incorporate ESG issues into our ownership policies and practices.”

While not enjoying equity investors’ position (and legal rights) as owners of the entities in which they invest, fixed income investors are still important stakeholders with clearly defined legal rights. They can interact with issuers over a) what activities issuers engage in, and b) how they behave and operate. Through this process – known as active ownership or stewardship – investors can encourage issuers to:

- better manage material ESG risks;

- increase the quality of information they disclose on ESG factors, allowing investors to make more informed decisions;

- improve issuer practices to promote financial or nonfinancial objectives.

An initial step is to publish a policy outlining the investor’s overall active ownership approach, the priority issues, plans for reporting and views on escalation.

Investors should consider not only ESG risks that are relevant to individual issuers or securities, but also risks that affect the whole portfolio, such as climate change.

As fixed income investors do not have voting rights, engagement is the key form of active ownership.

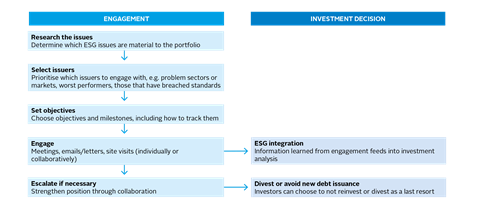

Engagement: working with issuers

Engagement sees investors working with issuers to gather information, improve disclosure of ESG data and, for corporate issuers, to encourage better management of ESG risks. Engagement can be a proactive attempt to address something an investor’s own research and analysis has highlighted, or a reactive move, such as in response to a controversial event.

Investors can engage individually or in collaboration with other investors (including across asset classes). Engagement typically involves private meetings or letters between investors and issuers, but can also include dialogue during investor roadshows, and at debt origination and reissuance. When engaging corporates, a challenge for debt investors compared to their equity counterparts is that their meetings with CFOs or treasurers are likely to be too narrowly focused on technical, debt-related matters to encompass the broader strategic considerations that can be important to ESG discussions.

For sovereign debt investors, the engagement process might involve meeting not only government officials, but also trade unions, employers’ associations, media representatives and supranational entities such as the IMF, the World Bank or the OECD. This non-issuer engagement can often be equally or more important than engagement with the issuer themselves.

Good engagement requires identifying relevant ESG factors, choosing issuers to engage, setting objectives, tracking results and feeding those results back into investment decision making. Persistence, consistency and listening are key.

If initial engagement efforts are unsuccessful, investors can consider escalation strategies such as collaborating with other investors, contacting the board, issuing a public statement, seeking legal remedies, choosing to avoid new debt issues, underweighting or divesting.

Downloads

An introduction to responsible investment: fixed income

PDF, Size 0.82 mbIntroduction à l’investissement responsable : obligations (French)

PDF, Size 0.84 mbIntroducción a la inversión responsable: renta fija (Spanish)

PDF, Size 0.83 mbIntroduçăo ao investimento responsável: renda fixa (Portuguese)

PDF, Size 0.83 mb负责任投资简介:固定收益 (Chinese)

PDF, Size 0.92 mb