Case study by AXA Investment Managers

- Signatory type: Investment manager

- Region of operation: France

- Assets under management: €804bn

Why investors should ramp up the integration of climate in their strategic asset allocation decisions

Global warming poses a range of both physical and transition risks as the energy sector shifts from fossil fuels to low-carbon alternatives.

Climate science has shed light on the needed efficiency gains to keep the global temperature rise by the end of the century at +1.5°C compared to the pre-industrial era. The Paris Climate agreement implied that annual global net CO2 emissions will have to be neutralised by 2050 and halved by 2030. This effort is being distributed differently among industries and countries.

Investors are incentivised to increasingly integrate climate into their allocation decisions due to a range of drivers:

- Perceptions of investment risks are shifting with climate change now being a leading concern. In the latest Global Risks Perception Survey, environmental worries dominated the list of major long-term risks identified by members of the World Economic Forum’s multi-stakeholder community.

- Growing evidence that climate change is financially material. A study by Mercer showed why a scenario where global warming was kept to below +2°C was the best outcome from a long-term investor perspective compared to +3°C (current Paris Pledges) and +4°C scenarios (business as usual). Looking ahead to the start of the next century, a +4°C scenario would leave diversified portfolios down more than 0.10% per year compared to a +2°C scenario.

- Regulation and prudential oversight incorporating global warming concerns. Climate change is important for long-term investors to consider from a regulatory viewpoint. For example, there are regulatory discussions in Europe around the integration of a green or a brown factor into capital requirements.

How to align strategic asset allocation (SAA) with a 1.5°C trajectory

Let’s look at our approach to climate change SAA:

Climate change is having an unequal impact on different investment assets. In this research, we present a first approach based on current carbon intensities data and a climate-related typology of assets to enable a consistent SAA.

This is exploratory as relatively little research has been performed to date on the subject. By onboarding financial engineering teams and climate experts, we have developed the following step-by-step approach to a 1.5°C aligned strategic asset allocation framework.

Step 1: Identify a base multi-asset portfolio consisting of listed equity and bonds. We start with the base of a traditional multi-asset portfolio composed of 44% global equity, 30% global investment grade corporate bonds, 6% high yield bonds and 20% government bonds.

Step 2: Re-adjust asset classes according to carbon emissions intensity (for corporate investments, we used carbon intensity in CO2e Tons/ Mns $ revenue from Trucost-S&P covering scope 1 and scope 2) and expected climate impact. We classified assets according to their exposure to sectors “at stake” (high and intermediate impact) and sectors “not at stake” (low impact) in global warming. This new typology of assets replaces the traditional dimensions usually involved in the SAA optimisation process namely sectors/countries indices.

Step 3: Conduct SAA according to optimising carbon objectives - Shift along the efficiency frontier.

Step 4: Refine and calibrate methodology

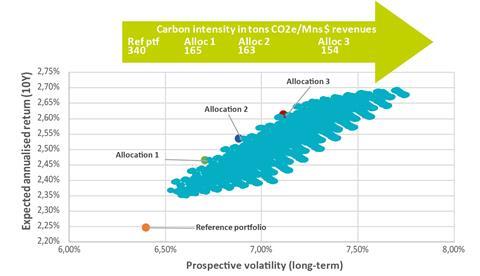

Our simulations showed that halving carbon emissions into the SAA did not deteriorate risk adjusted returns. Through having a greater amount of assets less exposed to climate change (but also to those assets qualified as “not at stake”), optimised allocations enabled the halving of carbon intensities while also presenting higher returns and higher volatilities. In total, these allocations are shifting favourably along the efficient frontier while at the same time not impacting the Sharpe ratio.

Alternative allocation optimised on climate KPIs

Limitations remain – The optimisation process above can be achieved but this will induce biases in the allocation away from sectors at stake and particularly high emitting sectors which are also those which will be necessary for energy transition. To ensure reasonable investment exposure to sectors at stake in global warming and generate the desired contribution to energy transformation, the following considerations are necessary:

- Metrics used to materialise climate impacts need to be enriched and to be more forward looking

- SAA frameworks and market indices need to be further adapted to better reflect various levels of an asset’s maturity in the transition.

- Through its alignment investment principles, we propose an introductory framework for further research to better align an SAA with the +1.5°C trajectory.

Example: Building a climate-aligned portfolio

The SAA optimisation process we tested succeeded in respecting financial objectives and achieving the climate goal of halving carbon intensities.

The climate-aligned portfolio needs to ensure sufficient diversification in its investment exposure between asset classes, sectors, and regions.

By adopting an SAA approach focused on decarbonisation, it is important that we are not inadvertently overly exposed to a single sector or region. Using carbon intensities as the sole KPI to reflect the climate objective does not guarantee a sufficient exposure to sectors at stake in the transition.

To counter these issues, we need to refine and calibrate our methodology, and explore the possibility of a +1.5°C aligned SAA methodology that will allow for investment diversification while contributing enough to the transformation of sectors at stake.

As part of our climate strategy, we have drafted 10 alignment investment principles a portfolio could incorporate to best contribute to the Paris goals.

These principles are based on breaking down the universe into 3 categories of issuers depending on their level of alignment with the Paris Goals and on their ‘greenness’.

- Carbon industry leaders: best carbon performers in sectors at stake (that is the most climate impactful industries)

- Transition leaders: issuers in transition to a Paris aligned trajectory

- Green leaders: core green issuers (companies already low carbon and contributing fully to the energy transition)

Selection of issuers inside each of these new categories will be achieved by combining quantitative and qualitative eligibility criteria. There is no one single metric but rather multiple dimensions to consider. This includes direct and first tier indirect carbon emissions (scope 1 and 2) but also those along all the value chain and from the use of products (scope 3).

It’s also about more forward looking KPIs such as carbon reduction objectives set by companies, the share of green products in business/operations or future capex mix and finally the warming potential of companies. Combined to these quantitative frameworks, a thorough analysis of the capacity of business models to transition and management quality will also be crucial.

The next step will see climate experts and financial engineering teams working together to explore ways to align an SAA with the 1.5 °c trajectory along this proposed framework redefining asset classes.