The incorporation of ESG factors within the investment process has evolved from a nice-to-have to a necessity. Client demand has grown strongly, with 68% of the PRI’s asset owner signatory base addressing ESG considerations in their requests for proposals (RFPs).1

This means that many asset owners expect investment managers to include financially material ESG factors within their funds and investment strategies. In addition, policy makers around the world are introducing regulatory requirements for both investment managers and asset owners to disclose and report on responsible investment practices.2

The PRI Leaders’ Group

The PRI has identified The PRI Leaders’ Group 2019, which highlights the asset owner leaders that have a thorough and systematic process for investment manager selection.

The PRI believes that responsible investment principles should be at the core of the relationship between the asset owner and the investment manager. To reflect their importance, they should be incorporated into all stages of the investment manager selection process.

The PRI has produced guidance to help asset owners address responsible investment principles and ESG factors in their relationships with their investment managers. The guidance comprises five modules (see Figure 1). They should be read in conjunction and will act as road map for asset owners to thoroughly embed ESG issues in their investment processes and at the core of the relationship between them and investment managers.

Module 1 describes a process followed by an asset owner to develop a responsible investment policy and strategy. This also includes the development of a strategic approach to asset allocation that incorporates ESG considerations.

Module 2 addresses the internal process of establishing mandate requirements, including key ESG considerations that will govern the investment manager, and drafting the RFP to reflect those requirements at a high level.

Module 3 focuses on the manager selection process to identify the investment manager that has the responsible investment attributes in place to meet the ESG requirements specified by the asset owner in Module 2.

Module 4 describes the manager appointment process to transfer the requirements specified in the mandate into legal documentation.

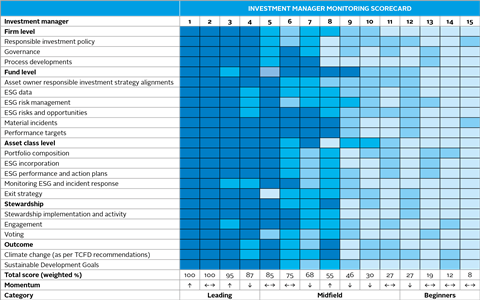

Module 5 sets out a harmonised approach to investment manager monitoring, including tools and practical recommendations.

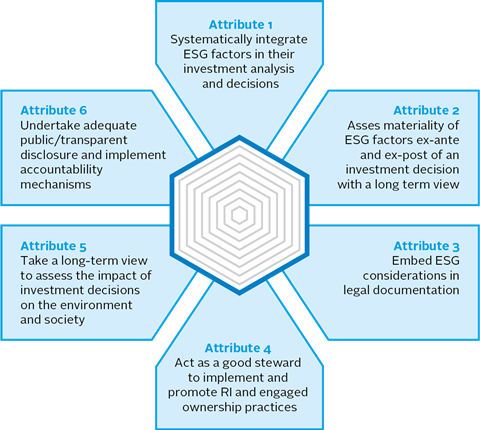

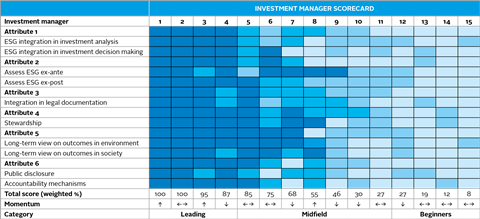

As identified in this technical guide and to feed into a comprehensive decision-making process, an asset owner should identify a manager which:

- is aligned with its investment principles and beliefs;

- systematically integrates ESG factors into investment decisions;

- analyses ESG materiality before and after investment decisions;

- acts as a good steward and implements responsible investment and engagement practices;

- addresses positive and negative outcomes caused by its investments; and

- undertakes adequate public/transparent disclosure and implements appropriate accountability mechanisms.

Investment manager selection guide toolbox

- CORE-ATTRIBUTES

- DDQ

- MONITORING-FRAMEWORK

- MONITORING-RANKING

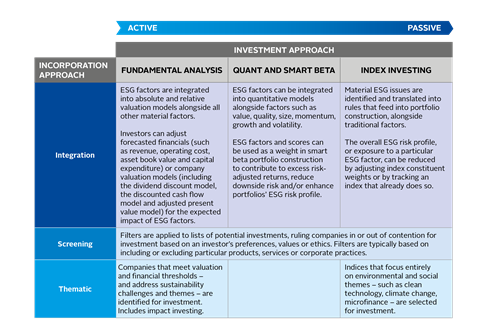

- ESG incorporation in listed equity across the active-to-passive spectrum

- Core-attributes visual

- Example of ESG-integrated firm and fund due diligence

- Investment manager ESG scoring methodology example

- Investment manager Monitoring scorecard

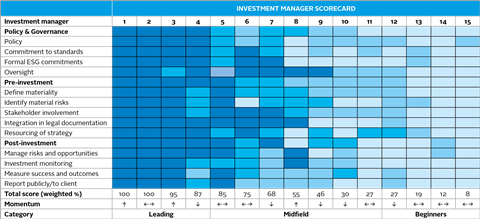

- Investment manager sample score card

- Investment manager sample score card DDQ

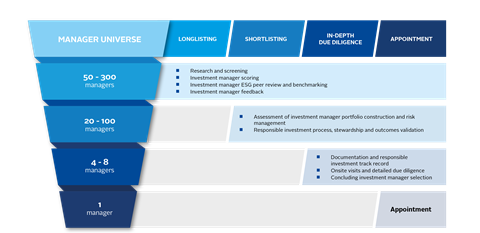

- The investment manager selection process

Downloads

References

1 Source: PRI 2019 Reporting and Assessment Framework results.

2 See more on the PRI’s Responsible investment regulation map

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}