Case study by ASR Nederland / ASR Asset Management (a.s.r.)

- Signatory type: Asset owner / investment manager

- Region of operation: The Netherlands

- Assets under management: €70bn

a.s.r. is a signatory to both the Paris Agreement and the Dutch Climate Agreement and wants to play a leading role as a sustainable investor. We believe that keeping the increase in global average temperature to 1.5 °C above pre-industrial levels requires scenario analysis and should be considered alongside the full investment process.

Why we include climate factors in strategic asset allocation

Empirical research shows that over a longer time horizon (10+ years) more than 80% of returns and risks are the result of Strategic Asset Allocation (SAA) and the portfolio’s positioning over three to four risk drivers such as growth, inflation and interest rates.

Over that long-time horizon climate-related risks will have a significant impact on these macroeconomic risk drivers and therefore on the risks and return of the portfolio.

A strong climate-risk management from the start of the investment process at the SAA level is a must for long term investors. This Top-Down perspective should be complemented with a Bottom-Up approach for portfolio construction including company/sector research incorporating climate exclusions, engagement and impact investing supported by analysis of ESG profiles, carbon footprint or Value-at-Risk.

The combination of the Top Down and the Bottom Up approaches provides a deeper understanding of the determining factors to help construct winning and resilient portfolios in the medium/long term.

Including climate scenarios in the SAA analysis provides support to the narrative for regulators & The Task Force on Climate-related Financial Disclosures (TCFD) reporting on the shorter term. This is essential for transparency and accountability.

How we quantify climate risks by looking into the future

In the Top Down approach, we have looked at four future climate scenarios combining both physical and transition effects.

The first envisions a 1.5°C temperature rise (approximately Representative Concentration Pathways (RCP) 2.6 of the Intergovernmental Panel on Climate Change (IPCC)) with an orderly transition towards a low carbon economy.

To achieve the ambitious reduction in carbon emissions, significant investments are made in low-carbon technologies with fossil fuels being replaced by clean energy sources. Globally, this transition would have a positive impact on GDP growth in the short and medium term of 7%.

The second scenario is a 1.5°C temperature rise with a disorderly transition towards a low-carbon economy. The difference between this and the orderly transition is that during the energy transformation additional shocks to the economy because of stranded assets are added.

The third is a 2.0°C (approximately RCP 4.5 of the IPCC) temperature rise with an orderly transition towards a lower carbon economy. The current low-carbon and energy measures are expanded, and investments made in energy efficient measures, renewable technologies, and market instruments. Globally, this transition has a positive impact on GDP growth in the short and medium term of 1%.

The final scenario sees a 4.0°C+ temperature rise and assumes no action has been taken to limit global warming. This results in no additional economic growth. The impact of physical and transition impacts slowly enters the global economy reducing asset returns.

We carried out this detailed analysis on our Assets Under Management (AUM) for the own account of ASR Nederland as insurer to test the resilience of the investment strategy and policy.

In the SAA, our balance sheet in its entirety was projected forward 20 years. Each scenario set consisted of 2,000 scenarios and these were fed into a stochastic financial model which in turn translated the impacts of these climate-adjusted GDP shocks on a range of more than 600 financial and economic variables.

Following this approach, we were able to quantify climate risk-aware economic outlooks per pathway, applied to the neutral economic scenario. The result is the impact of the different economic environments and climate scenarios on the RAS (Risk Appetite Statement).

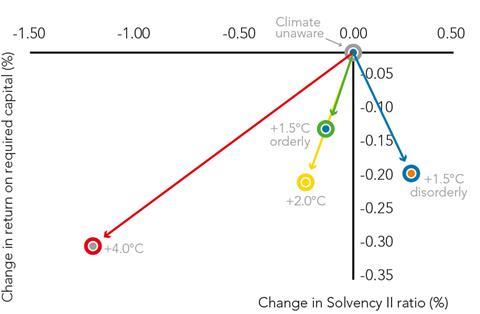

Example: Solvency II

Impact of the global warming scenarios on the average Solvency II scenario

The above graph shows the average impact of the four climate change scenarios on the Solvency II ratio and the return on required capital (annualised) over 20 years, relative to the climate unaware outlook. On average, there is little difference between the impact of the climate scenarios on the Solvency II ratio:

In the 1.5°C disorderly scenario, sudden sales of stranded carbon-related investments occur around 2025. This causes a financial crisis in which the portfolio is de-risked in accordance with the dynamic investment policy to maintain the Solvency II ratio. This leads to lower returns, but the de-risking is on average slightly more than required causing the Solvency II ratio to increase slightly by approximately +0.3%.

As global warming rises the returns on the asset portfolio decrease due to an increase of the impact of the materialising physical risks.

In the 4.0°C+ orderly scenario, the decrease of risk and return is slightly less than is required to perfectly maintain the Solvency II ratio, causing a decrease of approximately 1.2%.

For a.s.r., the average impact on the Solvency II ratio is less than 2% which is considered limited. The small impact is due to three reasons:

- In a dynamic investment strategy, the portfolio is de-risked (re-risked) when the Solvency II ratio decreases (increases). This results in lower (higher) returns and lower (higher) capital requirements, leading to a stable Solvency II ratio.

- Tilt towards European investments. Europe is more resilient to climate change than other economies around the world, resulting in a lesser effect of global warming on the economy. Under the Paris Agreement, developed economies are moreover required to do more to limit carbon emissions than developing economies, leading to higher investments in the 1.5°C and 2.0°C pathways.

- Our SRI policy reduces exposure to sectors with high transition risks and increases exposure to sectors with high transition opportunities. This is indirectly observed in the SAA climate scenarios.