The total amount of global institutional investment in forestry has surged from an estimated US$10 billion-US$15 billion in the early 2000s to over US$100 billion today.

While calls are growing for investors to turn to forestry to tackle climate change and associated issues, the main factors behind the growth in this asset class are more prosaic. Indeed, investors have traditionally allocated to forestry for similar reasons as for other real assets, particularly as an inflation hedge, as an asset with a relatively low correlation to equity and bond markets, and as a stable, long-term holding.

Other factors are more forestry-specific, such as long-term appreciation of the underlying land, the growth in value of trees as they mature, and the potential for multiple income streams from different uses of the assets, such as timber production and recreational activities.

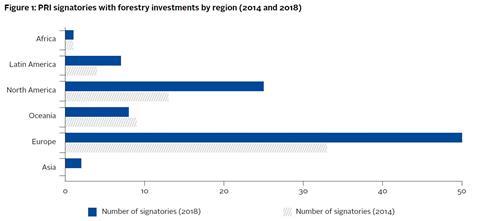

Figure 1 shows that 93 PRI signatories (out of over 1,400 total signatories), largely concentrated in Europe and North America, reported having forestry investments in 2018. This compares with 60 signatories in 2014.

Responsible investment in forestry

- 1

- 2

Currently reading

Currently readingForestry: a growing asset class

- 3

- 4

- 5

- 6

- 7