This short paper by Kaya, a specialist climate policy consultancy, has been commissioned by the Inevitable Policy Response (IPR). It assesses the initial implications for climate policy as a result of Russia’s invasion and war in Ukraine.

The Ukraine war, in all its horror, will mark a substantive elevation of security in the energy policy mix, triggered by the urgent intent to curtail Western dependence on Russian fossil fuels. The importance of this shift cannot be understated.

New leadership focus, and impetus for renewables, will emerge as a stronger, long-term policy trend. Balanced against this will be short-term demand for more fossil fuels to alleviate strategic exposure to record high prices. Increasing the resilience of renewable energy supply chains will receive laser focus.

Global policymakers are now dealing not only with a full-blown energy crisis but also skyrocketing prices for products ranging from agricultural commodities and fertilizers to semi-conductors and metals, all of which are essential in the effort to reduce greenhouse gas emissions.

This note focuses primarily on Europe, which is being impacted by the energy dilemma most acutely and touches on implications for the US and China. Before we continue, please let us first express our heartfelt sympathies with the peoples of Ukraine.

The climate policy ramifications of this moment should be contextualized within broader climate developments prior to the invasion. COP26 signalled a renewed push by nations to tackle the climate crisis including global pledges to halt and reverse forest loss, reductions in methane emissions, ‘phasing down’ coal and an historic net-zero commitment from India. Energy prices began bubbling behind the scenes as the covid pandemic subsided (ex-China) and global energy demand increased accordingly.

Enter the war. Against most expectations, Russia invaded the sovereign nation of Ukraine. It was at this point that the world, notably Europe, and especially countries like Germany and Italy, realized their huge miscalculation in allowing their dependence on Russian gas to grow to over 55% and 40% respectively.

The impacts of the war will be long lasting. As the Russian aggression continues, unprecedentedly severe sanctions against a member of the G20 from the West threaten to devastate Russia’s economy. Measures taken from either side which impede the flow of oil and gas from the world’s second largest hydrocarbon producer1 and exporter2 could have significant ramifications for the transition.

Such a large fossil fuel supply shock has implications for the renewables build-out as well. China owns a dominant global position in green technologies, components, and materials, and is the critical actor in any attempt by the West to accelerate electrification and clean energy buildouts. Policymakers are responding to the crisis in ways that attempt to solve energy and critical asset security while insulating citizens from the surge in energy prices. The resultant climate policy measures will have direct consequences on emission mitigation pathways.

Policy Implications, Energy: It is impossible to ignore that beyond the human tragedy, the war in Ukraine will disrupt energy flows and outcomes in the next few years, particularly in the EU. As described below, short term emissions could rise beyond our 2021 assumptions for the 2020s, if for example coal is used as a substitute for Russian gas, although much might depend on how overall economic growth responds. Longer term we see the shift to low carbon reinforced.

On all time frames, the concept of security will become a more dominant driver of energy markets. The debate has begun to rage about the energy security aspects of electrification. On one side, locally sourced renewables lessen dependence on unreliable, or antagonistic, hydrocarbon states. But this clean energy angle has the potential drawback of being exposed to supply chain risks, notably from China. In contrast, addressing the security of energy simply by doubling down on fossil fuel sources could stall climate progress by locking in oil and gas infrastructure, thus prolonging reliance on adversarial regimes such as Putin’s.

Our view is that an ‘all of the above approach’ will emerge, certainly short-term: Fossil fuels as a strategic back-up for a cleaner energy might persist longer, but in order to reduce emissions, not run at high-capacity levels. This leaves the expansion of electric vehicles, renewables and hydrogen as key medium-term drivers. Accelerated efforts for carbon capture and storage (CCS) would directly address fossil fuel emissions. In this world, simple ‘least cost’ approaches are overridden to some extent by the strategic imperative of security. Fossil fuel back-up costs become almost a defence budget cost, as illustrated recently by Germany proposing that financing for two LNG terminals come from the increased defence budget.

One solution is obvious: Energy efficiency is crucial and yet again needs accelerating. Heat pumps in the EU have received special attention and we would encourage policymakers to support these further. The European Commission has proposed speeding up negotiations on energy efficiency legislation. Our FPS forecasts call for significant efficiency savings from both industry and consumers.

Policy Implications, Land Use and Food systems: The Ukraine war’s impact on food security has also emerged as a focus point prompting an examination of the disruptions in global agriculture markets. Short term the issue is how to replace Ukrainian and Russian wheat, especially if the war extends through planting seasons. Again, no easy answers. The European Council and G7 are seeking to address such issues by all means at their disposal.

Longer-term, the IPR FPS has argued for a peak in animal protein production by 2030 which implies far less need for feedstocks such as wheat and frees up land for Nature Based Solutions (NBS) like reforestation. Food security may well depend on plant-based proteins (For further detail, please see this post from IPR land use specialist Tanya Khotin).

Implications for the IPR FPS and IPR 1.5°C RPS scenarios: On this basis, the outcomes for the FPS scenario, which currently predicts a 50% chance of a 1.8°C warming, and the extra requirements for our 1.5°C RPS do not change substantively in terms of emissions outcomes. The fossil fuel supply mix, however, will change. More hydrocarbon capacity may stay in the system but at reduced capacity utilization rates. This means it will not be added to generation except in an emergency. The push to simultaneously build out a cleaner energy system will continue and even accelerate medium term, in areas such as EVs and renewables as supply chains catch up.

In the words of the G7, the long-term aspiration has not changed: “This crisis reinforces our determination to meet the goals of the Paris agreement and of the Glasgow climate pact and limit the rise in global temperatures to 1.5°C by accelerating reduction of our reliance on fossil fuels and our transition to clean energy.”

Mark Fulton, IPR Project Director

The Ukraine War, Implications for Climate Policy: A Kaya Policy Analysis

- Energy and food security are moving inexorably under the wing of ‘national’ security in Europe, the US, China, and beyond. This has direct implications for climate policy and offers new impetus to the renewables build-out.

- The achievement of energy independence now dominates European energy policy formation, profoundly changing the approach of policymakers. In direct response to the war in Ukraine, the European Commission has suggested to reduce Russian gas imports by 2/3rds by the end of 2022 and 100% by 2027. The ongoing game of chicken over paying in Roubles raises the ante towards an early shut off.

- European leaders are pivoting towards industrial policy to achieve their aims. State aid, procurement, joint storage, subsidies, incentives, and potentially even caps on energy prices will be deployed in addition to the traditional reliance on regulation.

- Getting off Russian gas is a major task for the EU. Immediate focus is on diversification of supply sources, achieving energy efficiency and reducing roadblocks to renewable projects. All means will be utilized in the near-term, including more coal and nuclear.

- While heavy polluting fossil fuels will be more dominant short-term, the significant impetus for the renewables agenda should, if successful, keep Europe on track for net-zero. The biggest challenge to Europe is tackling supply chain issues and dependencies, not least in relation to China, as well as incentivizing member states to deliver what is needed.

- Record-high energy bills, a potential recession and the biggest refugee crisis in Europe since WW2 is forcing policymakers to mobilise around support measures. New rounds of public joint borrowing may materialize.

- Depending on its duration, the war in Ukraine could have harsh consequences for global food security. The impact would be most felt in developing countries, posing significant challenges to the ‘Just Transition’ agenda. In Egypt, the host of the next COP, the price of wheat has risen 44%, posing an existential threat to the economy. The government will struggle to sustain subsidies.

- In the US, the sanctions response has been resolute and decisive. Domestically, two competing policy narratives are emerging: ‘Drill, baby, drill’ vs the continued push for a ‘whole of government’ climate agenda ahead of pivotal mid-term elections.

- Chinese leadership is walking a tightrope. Given their dominance of the clean energy supply chain and role as fossil fuel importer, which way they fall will have consequences for global emissions pathways.

- The deployment of extreme sanctions by the West has implicit yet large implications for the climate transition. The severity of this impact will be determined by the duration of resultant changes in energy or food prices, backlash trading bans (e.g., potash), or an erosion of general levels of cooperation between nations.

- Policymakers in Europe and China will be inclined to take a heavier hand in the power market while in the US, which is more energy independent, market forces will dominate.

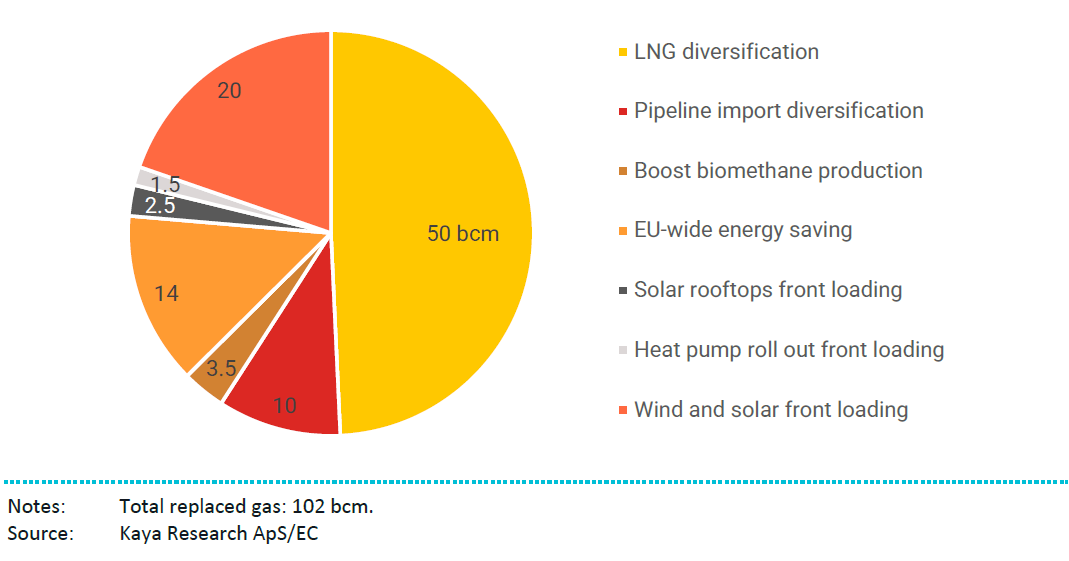

What do current actions tell us about the shift in policymaking direction? In the non-legislative Communication from 8th March, the EU Commission proposed a ‘RePower EU’ plan (see Figure 1) with a target of reducing dependency on Russian gas by 2/3rd by year end and achieving full independence from Russian fossil fuels well before 2030. This proposal makes clear the intention for a more active use of industrial policy. REPower EU’s direction is multi-pronged, focusing on the diversification of fossil fuel imports, law-enshrining gas storage commitments and a more aggressive roll-out of renewables.

Figure 1: How to replace 2/3rds of Russian gas imports to the EU by the end of 2022, according to measures proposed by EU Commission

This plan met support at the Versailles Summit by Heads of States on the 10th and 11th of March, where the Commission also advanced the proposal that the EU should be fully independent of Russian fossil fuels in 2027. At the March 24-25th EU Council this agenda gathered further momentum as President Biden announced that the US would aim to provide the EU with 15 bcm(billion cubic meters) of LNG this year, while aiming for as much as 50 bcm in coming years.

No legally binding agreement has yet been made on the REPower EU plan, but the Commission is now tasked with following through and drafting concrete proposals by May. This will entail action in areas that sit only partially within Commission competence. As such, the role of member states will be to rapidly decide on and implement a full range of required policies.

As mentioned, the suite of proposed tools will focus less on regulation and more on industrial policies, which is a jealously guarded domain of member states. If member states agree to the framework of the RePower EU plan, they will:

- embark on ambitious efforts to diversify LNG supply;

- boost biogas and green hydrogen;

- streamline the authorization process for renewables;

- improve gas and power interconnectivity, bolster security of supply contingency planning;

- ensure minimum levels of seasonal gas storage and improve energy management and efficiency;

- accelerate building refurbishment, notably insulation of houses; and

- ccelerate instalment of heat pumps

Reducing demand for energy will become an important goal in itself. After all, the cheapest energy is the energy not used. To that end, we expect further incentives and subsidies will be put in place, not least to support households and industry to move forward on retrofitting buildings and installing new energy sources to secure efficiency gains.

To meet energy conservation targets, an increase in heat pump production would need to resemble ‘war-footing’ efforts. An IEA estimate for speeding up anticipated deployment by doubling current EU installation rates of heat pumps would save an additional 2 bcm of gas use within the first year and require a total additional investment of EUR 15 billion.

A potential catalyzing agent for enlisting much-needed private investment could be the so-called ‘Carbon Contracts for Difference’ (CCfD’s). These give governments an opportunity to guarantee a fixed carbon price to investors in need of revenue clarity when planning green energy projects. The system would resemble traditional feed-in premium/tariff policies for renewable energy projects but would differ in that instead of ensuring a power price, it would guarantee producers of low-carbon products a fixed carbon price.

The REPower EU plan reveals a heavy reliance on member states and their willingness and ability to carry out measures. Accordingly, we should expect to see a ‘marketplace’ of interests develop, where member states push agendas unique to their situations. An example of this is Spain and Portugal achieving leniency for temporary interventions in the energy market in the Iberian Peninsula due to its high share of renewables and high payments for spot price gas.

Getting the member states on board will have another, potentially historic, impact; not only will pressure increase for prolonged leniency of fiscal rules, new rounds of joint EU borrowing may finally materialise. Indeed, momentum behind this is already present in EU meetings. ‘Grand bargains’ and mobilised financing should serve to accelerate the green agenda and could deliver unprecedented European collective action in energy and industrial policy.

We are witnessing history as the EU shifts from a heavy reliance on regulation to embedding decarbonisation into the fabric of European industry via industry policy, state aid and procurement.

The EU is also on track to deliver more robust measures to protect both consumers and industries from the impacts of higher energy prices at a broader level. These can include windfall taxes on companies, reduced taxation, state aid, price caps, and direct income support or vouchers to households.

Such measures were part of the discussion at the March 24-25th EU Council, where Commission President von der-Leyen advocated for joint purchasing to enable the use of the EU’s collective bargaining strength in the power market. The Commission is expected to present a proposal by May on an energy market reform to decouple gas prices from overall electricity prices with the aim of cushioning consumers, along with broader proposals on REPowerEU.

We look for these types of measures in the EU to be more enacted and accepted given the lack of energy self-sufficiency in the bloc.

The EU and its members are more inclined to state-led type measures than would be possible in the more market-driven and energy self-sufficient US. In this way, the EU and China are more alike than the US. Mechanisms and conditions are more conducive to active intervention than in the US. In the EU, it is not inconceivable to imagine nationalization of utilities if the crisis worsens, a prospect that would be more difficult to imagine in America.

Before the war, the big EU climate legislative package ‘Fit for 55’, with 15 separate policy proposals, was well underway in terms of negotiations. Some of these ‘files’ (e.g., content areas) could be accelerated given the urgency at hand, not least those aiming to increase energy efficiency. Examples of these advanced files are the Energy Performance of Buildings Directive (EPBD) and the Renewable Energy Directive (RED) as well as several infrastructure and transport files.

Other major components of Fit for 55 might become imperilled however with high energy prices placing too much of a burden ahead of a slowdown in economic growth. This is true especially for the proposed extension of the European Trading Scheme (EU ETS), the so-called ‘EU ETS2’. Implementing the EU ETS2 would increase carbon pricing, placing larger financial burdens on both industry and consumers at a time when policymakers are now planning for ways to reduce these very burdens.

As the proposals for a Carbon Border Adjustment Mechanism (CBAM) and a Social Climate Fund are intrinsically linked to the EU ETS and the expansion, respectively, these two proposals may also be subject to increased scrutiny.

None of this is to say that the EU legislative package or the ambitious EU climate goals will be abandoned as reaffirmed by European leaders of the G7 on March 24th. However, given Fit for 55 was not designed with an energy crisis of this magnitude in mind, additional or altered measures will materialize to use all levers, such as means of investment support for renewables, as laid out above.

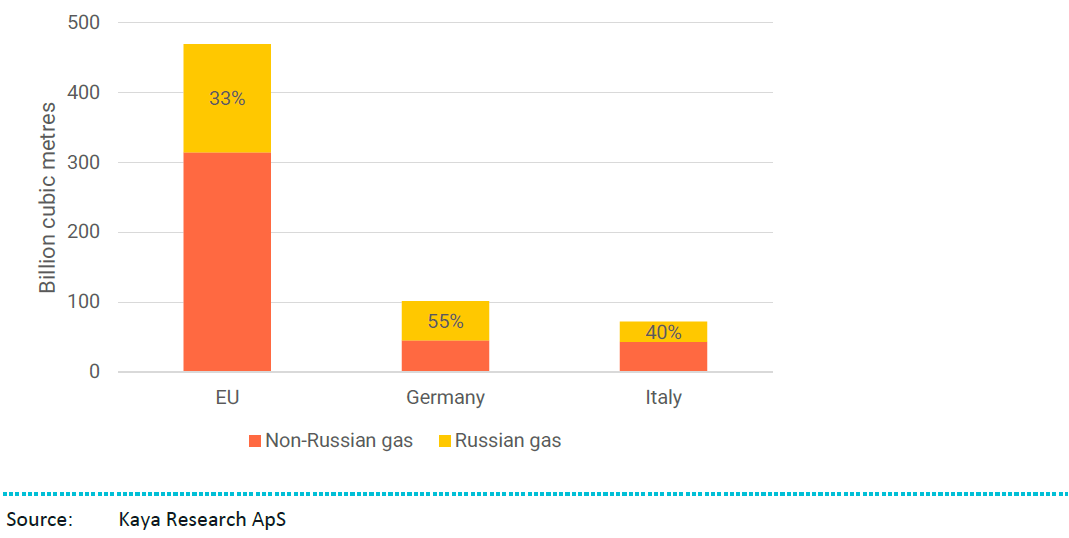

The European Union is critically dependent on Russian fossil fuel imports. Figure 2 shows Russian gas imports to Germany, Italy, and the EU as a whole. At the bloc level, the share of Russian gas imports was 1/3rd in 2021.

Figure 2: Proportion of natural gas imports from Russia into the EU, Germany, and Italy

As illustrated in the REPower EU Communication, the EU’s immediate strategic focus will be on alternative gas supplies, principally LNG imports and pipeline gas from existing providers. According to the Commission, diversified imports from non-Russian geographies could potentially replace over 60 bcm of gas over the next year but this would only represent 1/3rd of Russian imports (see Figure 2). The recent announcements by the increase of US supplies may raise this figure. However, logistical hurdles still prevent a rapid increase of EU gas imports, most notably the lack of sufficient LNG terminals or pipeline infrastructure within the bloc. Beyond physical shortages, the long-term contractual nature of the LNG market creates structural challenges for supplying the EU with the needed volumes. On top of this, the market is subject to capacity constraints and competition from growing Asian demand.

The bottom line is that even with increased flows from non-Russian producers, we do not expect diversification of gas supplies to be a sufficient substitute in the short-term. Other measures will be taken. Europe is still capable of seeing itself through next winter with a combination of current record-high LNG imports, accelerated storage, energy efficiency measures and increased coal consumption.

Additionally, demand is likely to be curtailed by behavioural changes and, potentially, by demand destruction from slower growth and higher energy prices.

As the energy crunch will be hard felt already this year, there will be a need for continued growth of coal burn, just as in 2021. While this runs counter to climate goals, coal will likely need to be burnt due to the simple fact that there is not enough installed green capacity. Reversing planned coal phase-outs taking place in 2025 or earlier could save 50 TWh of energy per year, equivalent to 2.6% of Russian gas imports. Rationing of energy to intensive industries is another option for driving down demand, albeit one with political implications.

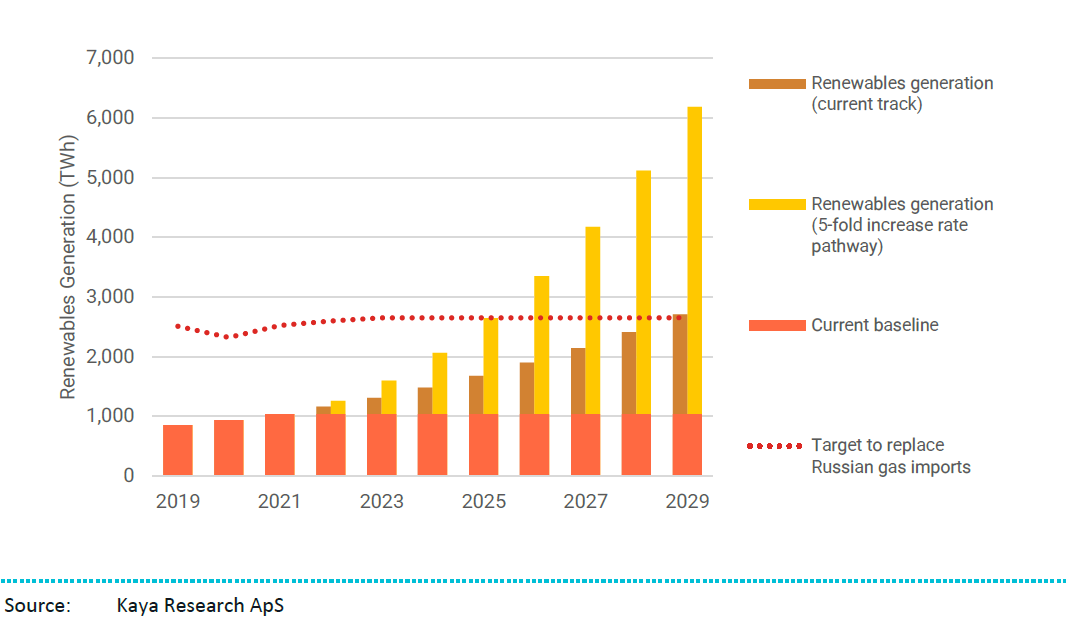

An increase in renewables will play a huge part in the medium and longer-term efforts to completely rid Europe of its Russian gas dependency. To date, the renewables roll-out has been slow and inconsistent. Recent efforts towards meeting the EU’s emission reduction targets put the deployment rate of new renewables on a more commendable, though ambitious track.

However, the war in Ukraine has placed far greater burdens on this rollout effort. With the threat of a loss of Russian imports to the EU’s generation mix, replacement is a top priority and yet only achieved in 2029 on the current pathway, assuming new renewables service only replacement and not any new demand.

Even a five-fold increase in this already-generous deployment rate would only hasten the replacement by four years (see Figure 3), not soon enough to deliver the immediate solution for the EU’s new strategic objectives in the REPower EU plan.

Figure 3 Renewables generation. A five—fold acceleration is needed to replace Russian gas by 2025

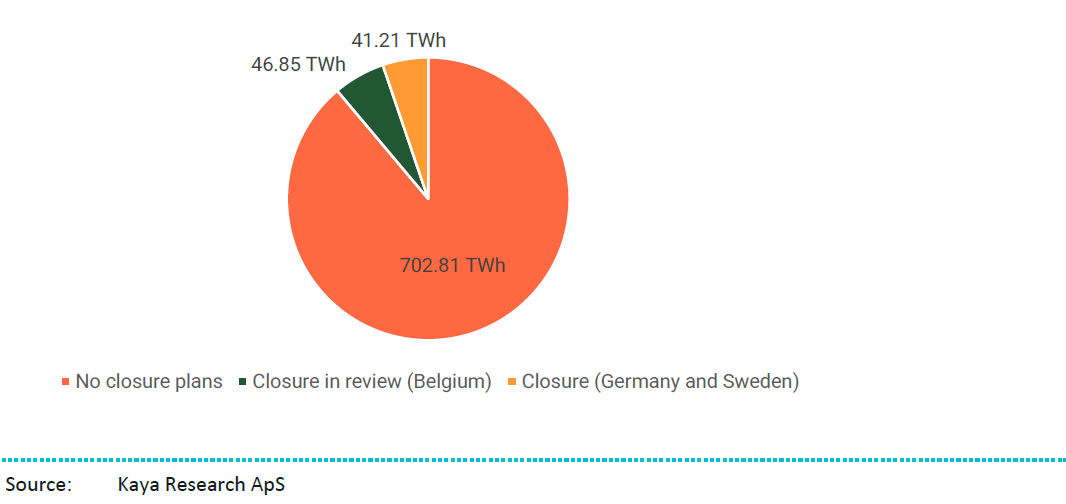

We expect that nuclear energy will play a supporting role, with the short-term contribution being only marginal. This could take the form of delayed decommissioning of existing plants.

As shown in Figure 4, reversing planned closures of nuclear plants in Belgium, Germany, and Sweden would make up for just 4.6% of the gas imports from Russia (88 TWh). France recently announced a programme to build at least six new reactors by 2050, with an option for another eight. Since it takes approximately 15 years to build a nuclear reactor, this is still not a solution for the short-term.

A renewed interest in nuclear is not confined to Europe. South Koreas new president, Yoon Suk-Yeol, has vowed to reverse his predecessor’s policy to steer away from nuclear.

Figure 4 EU annual nuclear generation

While the longer-term outlook shows some promise, the short-term crisis, as stated above, necessitates emergency measures to ensure energy supply via any means, dirty or clean. The resultant trajectory of emissions is best left to modelling but it is plausible that emissions will spike in the next 1-2 years, conceivably succeeded by steeper reductions thereafter.

We note that both the IPR Forecast Policy Scenario (FPS) and 1.5°C Required Policy Scenario (RPS) see rising emissions over the next 2-3 years as a starting point.

As the EU deploys more industrial policy tools to address the needed roll-out of renewables, the concepts of strategic autonomy and industrial resilience will acquire more momentum. This will include addressing Europe’s dependence on China for renewable products and technologies. Figure 5 highlights the position China holds in export of critical minerals, but the dominance extends further into the supply chain. China manufactures 85% of global solar-grade polysilicon, going on 90% in the next 2 years. 75% of the EU’s solar panels were from China in 2020.

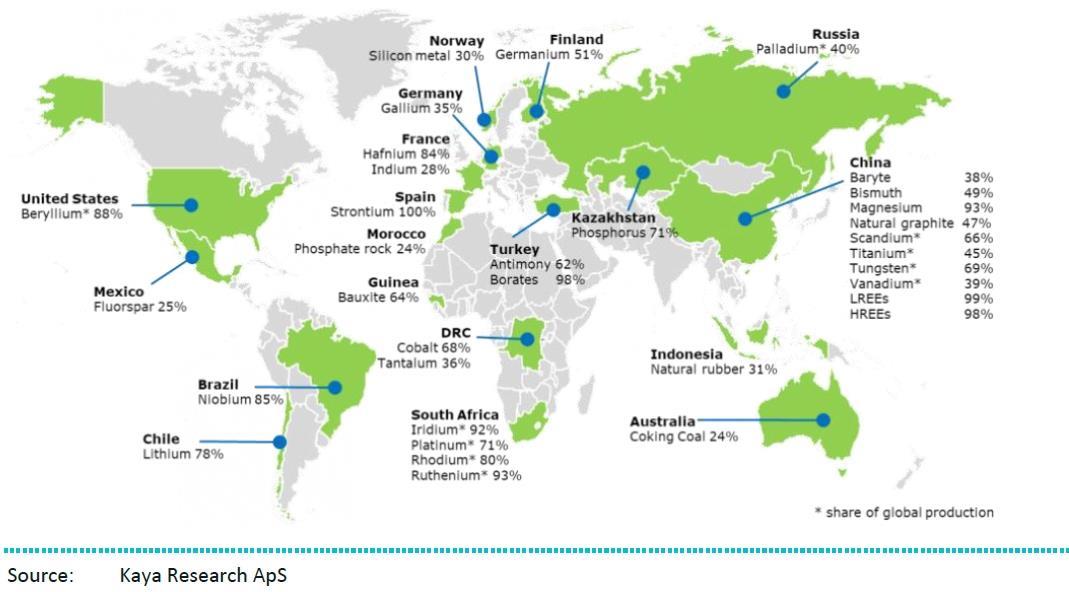

Developing resilient supply chains for renewable technologies in Europe must be underpinned by raw material and component sourcing, including efforts to build up domestic production capacity.

Figure 5 Countries accounting for largest share of EU supply of critical raw materials

The economic ramifications stemming from the war in Ukraine are not just about energy, but also about securing critical assets such as agricultural products and fertilizers. The supply chains of these items are as important as gas and also critical to the achievement of climate goals. For example, land use for biofuel or food production might become prioritized as opposed to being preserved for carbon sequestration.

Regarding food security, Russia is the world’s biggest exporter of wheat and, together with Ukraine, accounts for approximately 1/4th of global wheat exports. Ukraine is also a major producer of the barley, rye and corn that Europe, the Middle East and Africa heavily depend upon.

An international food crisis would have serious consequences in addition to being a humanitarian risk for Europe and the world. World leaders are increasingly attentive to this risk and sent strong signals at both the G7 meeting on the 24th of March and at the EU Council on the 24-25th of March that a global food crisis need to be avoided using all instruments and funding mechanisms available. Concretely, the European Commission recalled the EU’s pledge to provide at least 2.5 bn Euros until 2024 to help regions most affected by food insecurity.

It should not be lost on the international community that Egypt, the host of the next COP, is one of the most severely impacted countries by the war in Ukraine. Egypt relies on large volumes of heavily subsidised imports to ensure food security for its 105 million population.

The Russian invasion has catapulted prices, increasing the price of wheat by 44% and sunflower oil by 32%. With around 80% of the supply of these items originating from Russia and Ukraine, the consequences of a failed spring harvest and trade disruptions are enormous.

Can an Egypt COP deliver long-term solutions when confronted by such short-term problems, especially when experienced by the host country itself? As a minimum it suggests agriculture and land use may be a prominent theme in Sharm el-Sheikh.

The larger climate ramifications are profound. A radical and global price acceleration in food and other items essential for everyday life, if sustained, makes the prospect of a ‘Just Transition’ more challenging.

Billions of the planets poorest inhabitants produce little in the way of emissions yet spend a disproportionate amount of their income on energy and food. After the acute energy needs of the developed world are dealt with – Europe has 7% of the world’s population but uses 17% of the world’s energy - policymakers will need to re-focus quickly on ensuring the developing world has sufficient support to come out of this crisis strong enough to tackle social and climate issues. By now, this will go well beyond the underdelivered commitment from developed countries to contribute $100bn annually to developing countries.

European leaders will need to deliver new and ambitious policies to meet the challenges faced by the confluence of these multiple systemic risk factors.

The challenge of delivering appropriate policies is now complicated by a new aggressive usage of sanctions by the West. Whether they be targeted at energy - as shown by the US and UK banning Russian oil imports - or not - evidenced by Chancellor Scholz refusing to do the same - sanctions have implicit impacts on the climate transition.

Higher fossil fuel prices, ceteris paribus, serve as a price signal which can speed up transition to green energy.

Running through one mixed example: Russia banning potash exports in response to sanctions increases fertiliser prices, and by extension, food input prices. This can induce either positive land use change (technology solutions increasing crop yields) or negative land use change (clearing forests to plant more crops), elicit behavioural change (e.g., away from the meat made more expensive), or lead to hard-hit developing countries being unable to afford food imports which forces them to abandon other initiatives including those which mitigate climate change.

A more general issue with sanctions, and indeed the conflict in general, lies in the potential for cooperation between nations to diminish. Pledges on deforestation, money for the ‘Just Transition’, sharing of clean energy technology and the resultant implications for learning curves are all exposed to the risk that countries become more estranged and combative.

Succinctly, policy reactions to the effects of sanctions have morphed into a salient vector for climate policy. Although no new rounds of sanctions have been announced at the latest discussions (EU Council on the 24-25th of March), we cannot rule out further expansion of sanctions if the situation on the ground deteriorates further.

This may include an oil import ban by Europe, actions directed at Belarus, potentially banning road and maritime freight transport to Russia as suggested by Poland and the Baltic countries, or in the extreme, secondary sanctions on any company dealing with Russian entities. This is particularly pertinent if Chinese companies are impacted.

The reaction by the US administration to Russia’s invasion has been resolute and decisive. More so even than closing access to the SWIFT payment messaging, freezing nearly half of Russia’s foreign currency reserve war chest is having devastating consequences for Russia’s economy. These measures are popular on both sides of the domestic political divide and the US has the luxury of being energy self-sufficient - indeed in February becoming the largest exporter of LNG.

It is worth highlighting that the sanctions and Russian energy import bans are being carefully constructed to minimise the negative side effects on the global economy, Europe, and China. The US is not impeding on the ability of Europe to import Russian fuel. This may change, however, if Europe’s stance hardens as the severity of the war intensifies.

Domestically, two competing policy narratives are coming to a head. Facing 8% annualised inflation and looming mid-terms, the US administration is pursuing aggressive measures to reduce the price of energy to the consumer. This includes releasing strategic reserves, making drilling leases easier to acquire and even meeting with Maduro in Venezuela. At the same time, Biden and Democrats continue to push forward on a reconciliation bill which may have substantial climate incentives such as a renewables tax credits. US Energy Secretary Granholm recently called for a ‘global clean-energy Marshall Plan’, which met heavy push-back from a number of Republican Senators arguing that gas was the answer to combat higher fuel prices. The name of any climate legislation may change from ‘Build Back Better’ but success in passing this would be hugely consequential to the US’s emission reduction ambitions and enshrine legislation ahead of a likely set-back to Democrats in November’s mid-terms. It is of note that pundits on both sides of the fossil fuel vs. renewables debate are referencing use of the Defense Protection Act to support their arguments.

In either case, this supports our assertion that energy policy and security policy are now fatefully entwined. This should ultimately be positive for renewables with more access to funding becoming available, which helps ensure energy independence.

One wild card and potential danger to the climate agenda in America is the decision by the US Supreme Court to hear the case of West Virginia vs. EPA. The conservative-leaning bench could rule in a variety of ways that impede the ability of regulators to carry out environmental and climate policy. This would leave Congress and market forces driving change including in response to Ukraine.

Leadership in China is a vocal bystander in Russia’s aggressive manoeuvres, to date issuing statements which are more supportive of Putin than not. Hawks would argue this is not surprising when seen in the light of China’s potential interest in re-incorporating Taiwan. However, China is walking a tightrope. On one side it is interested in being a global player, avoiding secondary sanctions, and generally participating in the world’s financial architecture. On the other side, supporting Russia strengthens a relationship with a partner who supplies an increasing, but small, part of its energy needs and serves to balance the US in the global world order. It would not surprise us to see China continuing to walk this tightrope for as long as they can. At the NATO summit on March 24th, there was another tug of war, with the summits clear message and warning that “China must not provide economic or military support for the Russian invasion but should use its significant influence on Russia to promote an immediate, peaceful solution”.

We see it as unlikely that China will significantly increase fossil imports from Russia. This is due both to interest in securing independent energy supplies and awareness of the risk of Westerns sanctions if China is seen to take advantage of the situation. China also suffers from infrastructure constraints in terms of terminal, transport and pipeline capacity and is carefully manoeuvring its geopolitical positioning to refrain from providing Russia assistance beyond the red lines established by the West. Indeed, Chinese state-owned enterprises have been advised “by banks and higher authorities” to stay away from Russian coal and Chinese controlled banks, to date, have refused to behave in a way that would alleviate the pain of sanctions on Russia.

For gas, China is a big market for Russia, but Russia is replaceable for China. This is a bit less true for oil given China’s dependency is much higher on oil (72%) than gas (44%) and coal (10%). China is also a huge buyer of LNG from the US on long-term contracts. Gas makes up a small (3-4%) part of China’s energy mix but is a critical clean peaking power source relative to coal. On the climate side, we see signs that China will continue to balance energy security with emissions reductions and may therefore leave coal capacity in the system but manage capacity utilisation to achieve emissions reductions. It will be worthwhile to watch how the Covid pandemic impacts a nascent economic recovery and resultant energy demand.

China generally has the upper hand in renewables, where it dominates nearly the entire supply chain. This dynamic is present in wind, solar and more basic supplies such as rare earths and steel for these and other sectors. China mines over 70% of the world’s rare earths – a set of 17 minerals used in a range of applications including electronics, defence and aerospace – and supplies Europe with 98% of its rare earth permanent magnets, used in wind turbines and electric vehicle motors. China also dominates in the production of other wind turbine inputs, such as 60% of global glass fibre production and 50% of global steel production in 2020.

As such, global industrial players remain heavily dependent on China for advancing global wind exploitation. While Europe has domestic capacity in steel production, the US production is significantly lower. As mentioned above, the EU is highly dependent on solar imports all along the supply chain, as China universally dominates. The US mainly imports from other markets, but it is likely that the components making up this production also has some origination in China: The US currently imports 5% of its photovoltaic solar capacity from China, with over 80% of modules coming through Vietnam, South Korea, Thailand, and Malaysia.

Conclusion

The Ukraine War has made energy and food security synonymous with national security. This brings new actors and impetus into an arena which is synonymous with climate change and the transition. Climate policymakers have new vectors of focus and stimuli to react to. The incredible price appreciation and volatility of both energy and food prices will necessitate new focus and innovative action by countries at the coal face of climate change.

Short-term energy security means doing whatever it takes, including burning of more polluting coal. This implication for emission pathways is likely ‘bad’ in the short-term, but hopefully ‘good’ in the long-term.

Global leaders are developing new policies to both cut dependence on fossil fuels and increase resilience of supply chains for a range of materials the world once took for granted. These are salient factors to incorporate into the IPR’s Forecast Policy Scenario.

This note has mostly focused on the acute situation in Europe, where a severing of dependence on Russia’s energy is factoring into and influencing climate policy in a most direct fashion. For Europe, being energy secure involves diversifying access to fossil fuels in the short-term and supporting the accelerated build-out of renewables in the long-term, while driving energy efficiency throughout. The resultant unprecedented push for alternative energy sources will lead to new industrial and fiscal policy initiatives steered by member states. This process will be guided by the Commission to ensure that all possibilities in the toolbox are exploited to help industry and consumers embark on an even speedier transition.

The task of weaning itself off Russian gas is an enormous one, as is the longer-term challenge of renewables build-out in a world where green supply chains are so dominated by China.

The US has been able to afford a resolute sanction response. A pro-climate democratic government has been forced to facilitate short-term hydrocarbon burn both to combat inflation and provide support to Europe. The ‘drill, baby, drill’ mantra vs. the Democratic administration’s continued push for emission reductions remain competing narratives. China is walking a tightrope, balancing its interests between the West and Russia. As China dominates supply chains for renewables, their leaning in the conflict will be essential for global emission reduction.

Globally, the consequences are being felt in regions further away, not least in a number of African and Middle Eastern countries who are critically dependent on wheat and other food supplies from Russia and Ukraine. Food prices are already soaring in some regions and the physical supply constraints pose a serious threat to developing economies.

As a result, further challenges will arise for a ‘Just Transition’ and the ability for developing countries to mobilise around the climate agenda. One hopes that the November COP in Sharm el-Sheikh does not prove itself to be a lost opportunity. Supporting the most vulnerable affected by the crisis will be an immediate task for policymakers both in and outside Europe.

The Ukraine war marks a seminal moment for the future of climate policy. Global leaders are realising that national security must now incorporate elements of energy self-sufficiency. This will have positive ramifications for clean energy and renewables. The decisions made on food security and supply chain logistics will need to be monitored for their climate impact.