- Signatory type: Investment manager

- Asset class focus of case study: Fixed income

- HQ Country: Netherlands

Robeco is committed to contributing to the 2015 Paris Agreement and acknowledges the responsibility of the asset management industry in addressing climate change. With the launch of the RobecoSAM Climate Global Credits strategy, Robeco has translated this commitment into an investment strategy that strives to keep the temperature rise well below 2°C above pre-industrial levels, and pursues efforts to limit the temperature increase to 1.5°C.

The RobecoSAM Climate Global Credits strategy invests globally in corporate bonds following an active and contrarian investment strategy and has explicit climate targets in line with the goals of the Paris Agreement. Practically, this means that the strategy was designed to start with a 50% lower greenhouse gas (GHG) emission intensity[1] compared to the global market universe and subsequently decarbonise at an average rate of 7% per annum.

To monitor that the strategy remains in line with the goals of the Paris Agreement, the strategy is managed against the Solactive Paris Aligned Global Corporate Index, a global credit index compliant with the criteria of the EU Benchmark regulation for Paris-aligned benchmarks. This is a newly created benchmark jointly developed by Robeco and Solactive.

The strategy combines top-down analysis of credit markets with bottom-up issuer analysis to identify the best investment opportunities within the Paris-aligned framework, and has climate change considerations fully incorporated throughout the investment process.

Exclusions

The strategy applies a tailored exclusion list compliant with the EU Paris-aligned Benchmark regulation. Exclusions include controversial behaviour based on international standards, controversial products, and fossil fuels. Specifically, coal, oil, natural gas, and electricity generation with a GHG emissions intensity of more than 100g CO2 e/kWh are excluded.

Investment analysis

For the investment analysis, the considerations of climate change in the bottom-up fundamental issuer analysis can be split into three steps:

-

Where is the company currently at?

Robeco seeks to determine a firm’s level of climate risk exposure by analysing the company’s current GHG emissions intensity performance across scope 1 and 2 as well as material scope 3; the main drivers of emissions; and the company’s ability to change.

-

Where does the company want to go?

In this second step, Robeco strives to assess how a company is dealing with its climate risk exposure. It does so by analysing information available on, for example, a company’s climate strategy, decarbonization targets, climate-related governance framework, capex plans, product launches, physical risks, and comparisons with the Transition Pathway Initiative and Science Based Target initiative.

-

Is it financially feasible?

Lastly, Robeco looks to conclude how climate-related risks and opportunities will impact the company’s fundamental. For example, by assessing whether the issuer’s climate strategy and targets are sufficient, or to what extent the capex plans are financially feasible.

Within the bottom-up fundamental issuer analysis, Robeco also analyses other ESG factors and the potential impact on an issuer’s fundamental credit quality. These ESG factors are determined based on financial materiality.

Portfolio construction

From devising a portfolio construction process that incorporates climate change considerations, the result was a three-dimensional approach which combines the regular performance target and risk budget with a budget to stay in line with the decarbonization pathway needed to be Paris aligned. This became achievable because the process aims to:

- Meet the carbon budget

Robeco targets that the strategy at all times complies with the aim of staying below the GHG emissions footprint of the Paris-

aligned index;

- Remain flexible within the carbon budget

It weighs the footprint against the attractiveness of the credit to meet risk-adjusted return targets; and

- Focus on decarbonisation pathways

It strives to be forward-looking in its footprint analysis, favouring those issuers that are on a credible decarbonisation pathway.

Outcomes

At the time Robeco was developing this Paris-aligned global credit strategy, no benchmark fully compliant with the criteria of the EU Benchmark regulation for Paris-aligned investments was available to the market. Therefore, Robeco joined forces with the benchmark provider Solactive to co-develop a new index.

The Solactive Paris Aligned Global Corporate Index is structured around the following principles:

- It reflects a process of year-on-year corporate decarbonisation, equalling at least 7% on average per annum, based on Scope 1, 2 and 3 GHG emissions;

- All industries except fossil fuels are included, and sector weights are kept close to the broader market index; and

- Emissions are normalised by the total capital of issuers, measured in terms of book value.

Despite the GHG-related constraints, the index characteristics mimic those of the general market over time. Specifically, back-testing of the Solactive Paris Aligned Global Credits Index against the Solactive Global Credits Index gives favourable results, confirming that the behaviour and nature of the two indices are very similar, with the important exception that the former has a strongly reduced GHG emissions footprint.

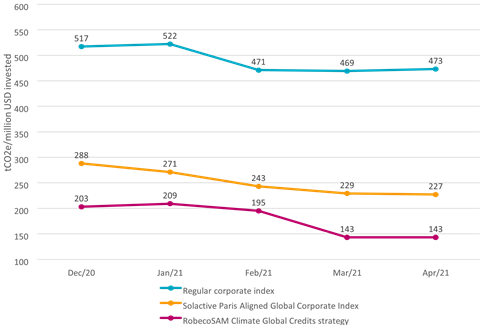

Since launch in December 2020, the GHG emissions intensity of the RobecoSAM Climate Global Credits strategy has been well in line with a Paris-aligned decarbonisation pathway. By the end of April 2021, the GHG emissions intensity of the strategy was 37% below the Solactive Paris Aligned Global Corporate Index and 69.8% below the regular corporate index (see the chart below).

Greenhouse Gas footprint performance

Figure 1: Source: Robeco, Bloomberg, Solactive. Greenhouse gas emissions data source: ISS, Scope 1+2+3/EVIC BOOK. Data end of April 2021

Challenges

One challenge is the complex task of attributing GHG emissions to fixed income instruments. GHG emissions are primarily linked to the equity issuing company, while fixed income instruments most often are issued by a financing entity under the equity issuing company. Moreover, it is not yet possible to use realised emissions for financed projects. This is especially relevant for instruments such as green bonds.

A second challenge is the opaqueness of the financed emissions of the banking sector. At approximately 35%, the banking sector is by far the largest sector in the investment-grade credit universe. To work towards overcoming this issue, Robeco’s Active Ownership team has started engaging with the sector as part of its ‘Climate Transition of Financial Institutions’ engagement theme. More generally, we also see corporate disclosures are improving. This paves the way for better data.

References

[1]Measured as EVIC book normalized GHG emissions, including Scope 1, 2, and 3 (tCO2e/mUSD invested)