Case study by RBC Global Asset Management

Rather than having separate ESG analysts, our Global Equities team’s portfolio managers perform and integrate ESG analysis to allow us to better fundamentally value and asses stocks, completely integrate ESG information into our investment process and meaningfully engage with the companies in which we are invested. We also use multiple sources of ESG information as it represents a plethora of ESG-related opinions that require interpreting, and portfolio managers are best placed to filter this advice and ascertain how it relates to a company’s business model and valuation. (In our experience, the ratings of two major ESG research providers only correlate just over half of the time and proxy voting agencies occasionally take opposing views on proxy votes.)

We start with a fundamental analysis to identify any material positive or negative ESG factors. We embed that assessment into an analysis of the competitive position and the sustainability of the business, which we then put into our valuation models. We invest only in companies that perform strongly in all four areas of our model: business model; market share opportunity; end-market growth; management & ESG.

Our Global Equities team identified several ESG risks (contingent liabilities) and opportunities (contingent assets) for UnitedHealth (UNH), a leading healthcare insurer and healthcare cost management and IT provider managing 5% of US healthcare spending.

Risks

As custodians of the personal and medical details of millions of people UNH needs to keep this data secure: false savings here can have long-term consequences, including regulatory risks, political risks and the potential impairment of the company’s social contract with customers and wider society.

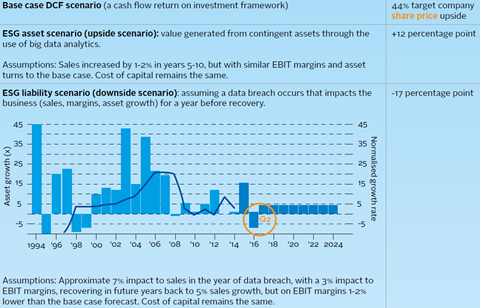

We challenged management on the risk of privacy data breaches, asking how that risk is being managed and what policies are in place to mitigate that risk. Management acknowledged that information about their data security was not available on their website, but several management members reassured us about the quality of the policies, training and general operation management of data handling and security that are in place. Nevertheless, we still modeled a discounted cash flow (DCF) valuation scenario looking at the possible impact of privacy data breaches.

We learned that UNH had a historic stock option accounting problem (backdated without disclosure to lower the strike prices for the then CEO), which came to light in 2006. However, we noted that many other companies, such as Apple, had similar stock option accounting problems in the late 1990s to mid-2000s. We also discovered that in UNH’s case it led to the start of a complete turnaround in the company’s corporate governance policies and practices, and determined that the current compensation structure was fair and, importantly for us, included a return on capital/ equity component.

Our conversations with UNH gave credence to the recent positive reports from two proxy voting agencies regarding the company’s governance practices; there do not appear to be remaining accounting or management problems that had been indicated in earlier analysis.

Opportunities

We viewed UNH’s Optum data analytics business, which allows it to create cheaper, better healthcare options for businesses, governments and patients, as a strong competitive advantage and an ESG contingent asset. For instance, it identified 150 diabetic patients not taking their medication properly, 123 of whom were in Texas, which enabled its client to implement location-specific measures utilising preventative health techniques. Using Optum’s data analytics, the state of Maryland discovered clusters of patients with asthma in certain streets and buildings, and found that those buildings correlated with cockroach infestations, allowing it to successfully prosecute deficient landlords and ultimately raise living standards for tenants.

Impact on analysis

We assessed the materiality of all of this information and assigned a rating for the four components of the company’s strengths (business model; market share opportunity; endmarket growth; management & ESG). We then performed a DCF scenario analysis embedding the material ESG risks and opportunities. We prefer DCF and explicit model scenarios for sales, margins, asset turns, etc. as we see them as a more accurate method of modeling than an adjustment to a discount rate or terminal value. We also perform sum of the parts and standard financial ratio assessments.

The analysis was peer reviewed within our team, and the assumptions were stress-tested, challenged and refined before the rating and valuation were confirmed. In our peer review, assumptions are flexed in real time to see how further valuation scenarios change. These include increasing EBIT margins and sales growth for the upside scenario, and for the downside scenario normalising sales to a lower growth rate (3%) and looking at the sales impact over more than one year.