Approximately 50 delegates gathered at a recent investor workshop at PRI in Person to explore how investors are approaching sustainable outcomes in their investments.

Translating sustainability objectives to investor practice

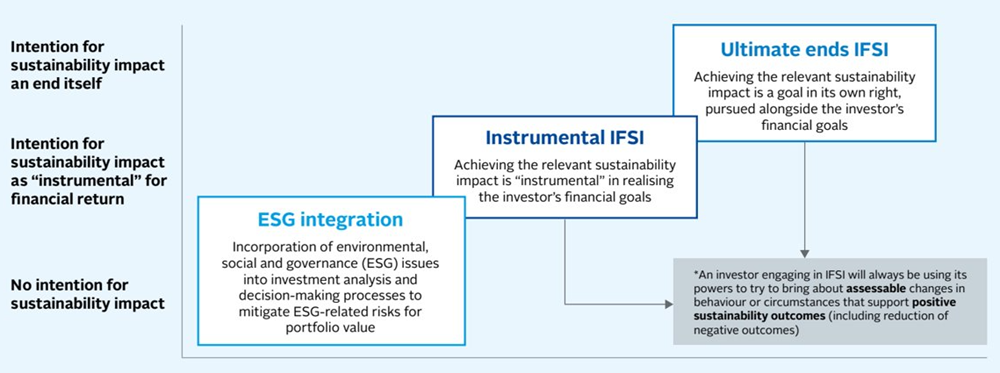

Investing for sustainability impact means investing which is orientated towards addressing sustainability challenges – either to achieve financial investment goals, or independently of those goals. This approach is described in a 2021 report A Legal Framework for Impact authored by Freshfields Bruckhaus Deringer and commissioned by the PRI, the United Nations Environment Programme Finance Initiative and the Generation Foundation. This involves establishing clear objectives for influencing investees’ behaviour, assessing progress, and understanding their contributions to broader sustainability objectives such as the Paris Agreement’s climate goals.

These challenges were central to discussions at the recent PRI in Person conference in Tokyo, where approximately 50 delegates gathered to explore how investors are approaching sustainable outcomes in their investments.

Key insights shared by discussion participants are summarised below.

Investor approaches to investing for sustainability outcomes

Two pivotal considerations guiding investment strategies for sustainability outcomes emerged in the session’s discussions:

- Alignment with Sustainability Commitments: Investors aim to align their strategies with various sustainability goals, such as climate action and social justice.

- Alignment with Client Objectives: The specific approach to sustainability is guided by the objectives of clients, which can dictate a focus on areas like climate change, particular social impacts, or other outcomes.

Practical approaches outlined by participants for implementing these strategies include:

- Portfolio approach to sustainability objectives: Investors integrate specific sustainability goals into their overall investment strategies, such as including climate and nature-related goals. Some prioritise social outcomes, such as gender and racial equity, and actively engage with investee companies to promote these objectives, such as increasing gender diversity on corporate boards.

- Sustainability-linked investment products: Impact investments allow investors to target specific sustainability goals, such as addressing climate change, community development, and public health. However, there is room for improvement in measuring these outcomes, particularly social impacts and sustainability-linked product performance indicators. Developing an impact taxonomy focusing on sector-specific results can help address these challenges.

- Engagement with companies: Engaging with investees is considered a critical element of investing for sustainability outcomes, as divestment eliminates the investor’s ability to influence change. Participants emphasised the importance of ongoing engagement beyond the initial screening process to address portfolio risks, including adverse financial and ESG outcomes.

- Engagement with governments: Engagement with governments is essential for advancing investors’ sustainability objectives, given the system-wide implications of these goals. For instance, investors assess sovereign bonds based on various factors, including countries’ contributions to sustainability outcomes. Engagement methods may differ by region, with potentially different levers and touchpoints. Screening out poorly performing countries from portfolios was seen as an option, but it needed to be considered alongside other factors.

Guidance and policies needed for investing in sustainable outcomes

Participants also highlighted priority enablers for more effective investment in sustainable outcomes:

- A common taxonomy for sustainable investment: A common taxonomy for sustainable investment is crucial for shifting investment priorities beyond financial metrics and incorporating factors like climate and social impacts. The EU’s taxonomy provides a clear starting point, but successful implementation depends on regulatory changes and mechanisms like efficient carbon markets. Interoperability between regional taxonomies is essential for global progress, requiring government leadership to ensure economies align with sustainability goals.

- Government leadership and coordination: Government leadership is pivotal for advancing sustainable outcomes in the market. Governments must set clear expectations for investor roles in national sustainability goals. Coordination, especially at the federal level, is essential for effective transition planning aligned with sustainability objectives. International policy consistency is needed, particularly on carbon pricing, 1.5-degree targets, and interim sustainability goals. Reporting and measuring sustainability outcomes are necessary for accountability. Legal obstacles, such as anti-trust issues hindering investor collaboration, require clear guidance from policymakers to give investors clarity on their fiduciary duties and permissible engagement in sustainability initiatives.

- Investor ecosystem education: Continuous education for investors on sustainable investment outcomes, particularly on social and governance issues, is essential. Advisory professionals who influence investment beliefs, such as lawyers and investment consultants, also need to understand the benefits and legal aspects of sustainability. This education can help promote consensus and awareness among investors. As consumer awareness shifts toward sustainability, corporate leaders play an important role in promoting sustainable practices and emphasising corporate awareness of sustainability impacts.

- Data and valuation: Data collection and disclosure efforts need to focus on systematic sustainability issues that are not yet effectively covered, such as gender and diversity data. Third-party data assurance is vital to ensure data accuracy. To mitigate the potentially higher cost of some sustainable investments (the “greenium”), valuation should be guided by realistic supply and demand factors. A balanced pricing approach should focus on whether the world is genuinely moving toward 1.5-degree targets.

- An equitable approach to transition planning and investing in developing markets: The needs of developing countries, including their longer timeline to achieve Sustainable Development Goals, must be considered in sustainable investment strategies. For example, planning the transition to renewables is important for mineral-based economies that are phasing out fossil fuels as well as supplying critical minerals for renewable technologies: all of which have environmental and social consequences. This is especially important for investment in emerging markets, to consider how their activities can mitigate burden-shifting and continue to meet “Do No Significant Harm” principles. Guidance and a shared understanding of good investor practices can help investors address these challenges and opportunities.

Next steps

Building on these insights, the PRI will continue to engage policymakers on investing for sustainability impacts, including on regulatory tools such as sustainable finance taxonomies. Recognising that localised support is needed for an effective shift to sustainable investment, the PRI will continue supporting investors as they progress in their responsible investment practices within the parameters of their local regulatory and economic climates.

Two different types of Investing for Sustainability Impact:

Source: A Legal Framework for Impact

Downloads

Investing for Sustainability Outcomes workshop at PRI in Person 2023

PDF, Size 0.24 mb