By Thorsten Beck, City’s Business School, University of London, and CEPR, Burton Flynn, Terra Nova Capital, Evli Group and City’s Business School, University of London and Mikael Homanen, PRI and City’s Business School, University of London

The economic fallout from the COVID-19 pandemic has been severe, with research confirming substantial declines in aggregate jobs, output, and investment. Most of the evidence so far, however, has been focused on developed markets. In our paper, we look at the impact of COVID-19 on ten emerging markets, combining survey answers with financial statement information and stock price returns.

Survey

In early April 2020, we sent out a 13-question survey to 630 firms across ten emerging markets: Bangladesh, Indonesia, Malaysia, Pakistan, Philippines, Saudi Arabia, South Africa, Thailand, Turkey, and Vietnam. All our firms are listed on stock exchanges and are active across all sectors of the economy.

The survey questions were divided into three blocks. In the first block, we asked firms whether their operations were affected by the pandemic, e.g., if they needed to raise capital. A second block considered whether firms had to adjust their operations and plans and whether they had reduced investment, laid off staff, made changes to employee benefits or executive compensation, amongst other changes. Finally, we asked questions on how firms dealt with business partners and society more generally: whether they had voluntarily taken any measures to protect their employees and other stakeholders, continued to pay employees or service providers for disrupted services, provided financial flexibility to any customers or business partners and made any donations to help fight the pandemic or shifted business operations to fulfil pandemic needs.

Out of the 630 firms, 488 (78%) responded, 98% of them between 2 and 24 April.

Corporate responses

The survey responses provide some interesting insights into how firms reacted to the pandemic.

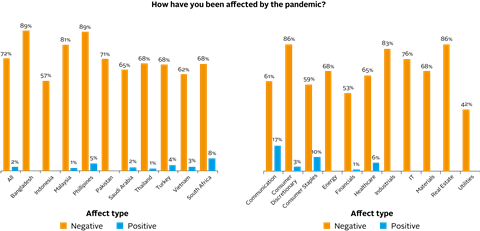

Three out of four firms were negatively impacted by the pandemic, with significant variation across countries, sectors and firms in impact and reaction (as shown in Figure 1). Surprisingly few firms, however, expected to breach their covenants or saw a need to raise additional capital. About half of the firms received or expected to receive government support. Firms reacted primarily by reducing investment spending and much less through layoffs. Meanwhile, some firms cut back on executive compensation, and more firms expanded employee benefits than cut them. Most firms acted before their governments had imposed measures, although there is no correlation of such action with how fast governments acted.

Firms were flexible vis-à-vis customers and stakeholders, provided donations to support society at large or shifted business operations to fulfil pandemic needs. This paints a picture of firms focusing on the short-term needs of stakeholders, protecting labour and long-term relationships – consistent with placing longer-term value maximisation for shareholder and other stakeholders above shorter-term gains.

In total, 91% of respondents took measures to protect stakeholders, 78% made donations to fight the pandemic, 46% continued to pay employees or service providers for disrupted services and only 8% had made layoffs.

While they might not have been the final reactions to the pandemic, these immediate reactions suggest that firms were stakeholder-centric in nature.

Several companies shifted their operations to fulfil pandemic needs. An underwear company in Thailand began making face masks – initially distributing them for free to help the government, before selling various designs. An Indonesian lifestyle retailer also shifted their garment factory to make masks and PPE for medical professionals. A hydrogen peroxide producer in Pakistan launched a disinfectant, which has not only seen an overwhelming market demand but also was donated in large amounts to the government.

A South-African self-storage asset owner and operator made its properties available, free of charge, to NGOs for the storage of coronavirus-related supplies. Furthermore, consumer staples companies, such as a Malaysian egg producer and an Indonesian rice business, donated the foods that they make. A Malaysian semiconductor company paid overtime rates to those who came to work, while a Saudi IT distributor continued to pay those who couldn’t come to work because of lockdown, and a South African minibus taxi financing business provided loan payment relief to its taxi owners. These are just some examples documented in the qualitative responses of our firm-level survey.

Corporate valuations

We find that stock markets priced in the need for firms to raise capital, reduce investment, make changes to the dividends or share buybacks, and make lay-offs between late February and late April (the initial outbreak period of the global pandemic). However, we find further negative stock reactions between late April and late June (two months after the majority of survey responses had been received), suggesting that stock markets were slow to react to the negative impact –and available information – of the pandemic on firms.

We also document that more stakeholder-centric firms (e.g. those which did not reduce employee benefits, took measures to protect stakeholders, or made donations to fight the pandemic) experienced lower stock price declines and did not significantly underperform between April and June, suggesting that the financial markets valued these stakeholder-centric corporations more than their counterparts during the crisis.

Conclusions

Our results point to the quick reaction of firms in emerging markets (often before governments), their focus on accommodating their labour force and maintaining long-term relationships with stakeholders. We also find evidence of markets being slow to incorporate publicly available information and valuing stakeholder-centric activities. Our findings provide a snapshot of the current situation – another stock-take later this year might provide different results – but they show that corporations are trying to make the best of a very bad situation.

The full paper can be found here.

This blog is written by PRI staff members and guest contributors. Our goal is to contribute to the broader debate around topical issues and to help showcase some of our research and other work that we undertake in support of our signatories.

Please note that although you can expect to find some posts here that broadly accord with the PRI’s official views, the blog authors write in their individual capacity and there is no “house view”. Nor do the views and opinions expressed on this blog constitute financial or other professional advice.

If you have any questions, please contact us at [email protected].