By Hazell Ransome, Policy analyst, PRI

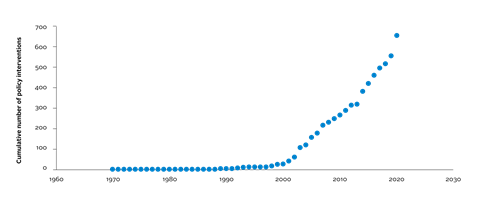

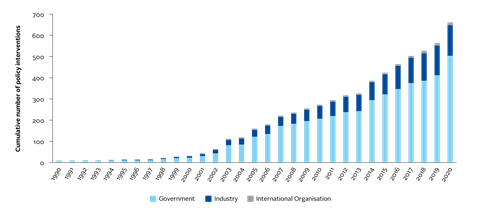

While 2020 put many plans on hold, there was no pause in the rapid growth of global responsible investment policy. Last year, over 120 new or revised policy instruments were established, the highest number ever recorded and over 30% more than in 2019. This growth is a reassuring sign that, even in times of crisis, regulators are not taking responsible investment off the agenda. Increasingly they understand the crucial role it will play in our recovery from the COVID-19 pandemic.

To track this trend and others, the PRI Policy team has updated and expanded its regulation database, which contains sustainable finance policy tools and guidance for investors to consider all long-term value drivers, including environmental, social and governance (ESG) factors. These policies and regulations can:

-

Support national policy goals on climate change and the SDGs;

-

Enhance the resilience and stability of the financial system and the economy;

-

Improve market efficiency by clarifying and aligning investor and company expectations; and

-

Increase the attractiveness of countries as investment destinations.

Since its last update in September 2019, we have increased the scope of the regulation database to cover all countries as well as international guidelines. This will allow us to track the uptake in responsible investment policy in countries that have recently started their responsible investment journey, and see which approaches are more popular. In the future, we hope that this could lead to tracking the effectiveness of policies and their alignment with each other, which is vital to achieving sustainable, inclusive and zero-carbon economies.

Let’s take a look at some of the trends so far.

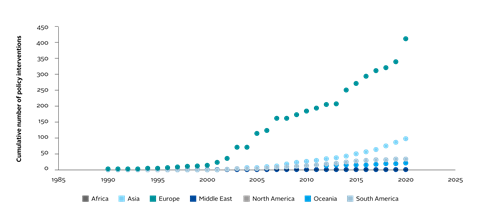

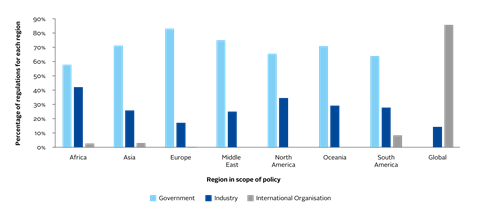

How does uptake in responsible investment policy vary between regions?

As expected, Europe is leading the way ahead of all other regions in terms of responsible investment policy, showing the sharpest increase over the past year as many of the regulations emanating from the European Green Deal, such as the Taxonomy and SFDR, start to appear[1]. However, we can see an increase in policy interventions across all regions.

In Asia there has been a significant upturn in the last 5 years. We look forward to seeing this grow further as the Japanese Green Growth Strategy, Taskforce on Preparation of Environment for Transition Finance and Expert Panel on Sustainable Finance take effect, and regulations materialise from the environmental proposals of China’s 14th 5-year plan, as well as the jointly issued guiding opinions to promote climate investment and finance from 5 Chinese regulators.

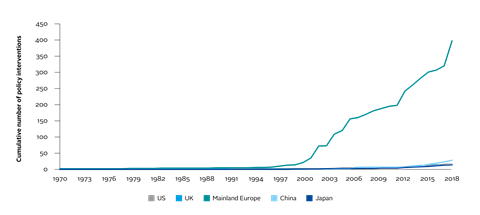

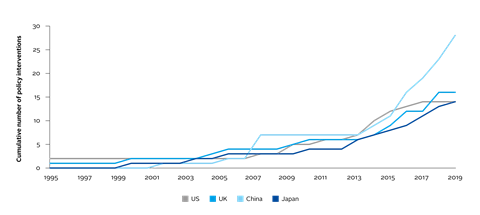

The graphs above show the trends for 5 key jurisdictions[2]which the Policy Team focuses on. As expected, during the Trump administration we saw a plateau in the number of policies promoting sustainable finance in the US. However, since the inauguration, the new Biden-Harris administration has signed a number of executive orders, including re-joining the Paris Agreement and addressing the climate crisis. The Securities and Exchange Commission has also announced a review of previously issued guidance on climate-related corporate disclosure requirements and an enhanced focus on climate and ESG-related risks. We wait to see the expected growth in responsible investment policies following this promising start.

Who are the main issuers of responsible investment policy?

The updated PRI regulation database allows users to filter by issuer. For all regions, most policies originate from the government. This has always been the case, but industry-led polices have also made up a significant proportion, which is roughly 20% of regulations since 1995.

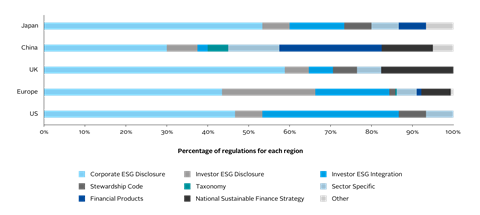

What types of policies are we seeing?

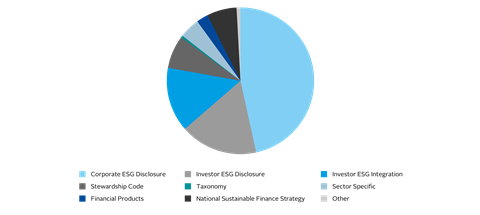

In all regions and jurisdictions, regulations requiring corporate ESG disclosure are amongst the highest in number.

However, in the past year, it appears the growth in corporate ESG disclosure regulations began to level off, whereas investor ESG policies grew rapidly. 2020 saw a huge increase in the number of investor-related ESG disclosure regulations (up by 74% from 2019) and investor-related ESG integration policies (up by over 100%). This is an important factor because corporate ESG disclosure is only one of five foundational sustainable investment policies and regulations. To create a sustainable financial system also requires stewardship, investor ESG duties, taxonomies and national sustainable finance strategies[3].

Taking another look at our 5 jurisdictions, we see there is a variation in the types of policies chosen, once we look beyond corporate ESG disclosure taking 1st place. For example, in Europe, non-corporate policies are mainly based around investor ESG disclosure, including the Taxonomy and SFDR regulation. In contrast, in China, after corporate ESG disclosure, most policies centre around financial products such as green bonds.

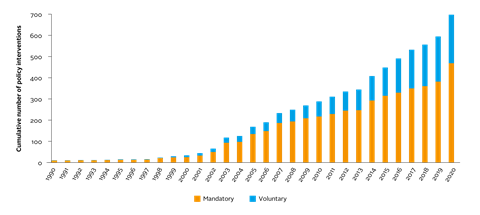

Are policies mainly mandatory or voluntary?

As responsible investment policy initiatives grow in number worldwide, we would expect to see the proportion of voluntary policies also increase, as they are often seen as a steppingstone towards hard law. Indeed, this has certainly been the case since the start of the century, but, in recent years, the proportion of voluntary policies plateaued to around one third of all regulations. We are yet to see whether this plateau is a long-lasting trend or not.

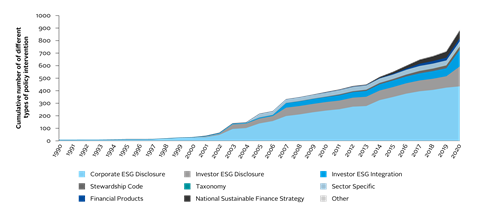

The updated regulation database showcases key trends and uptake in responsible investment policy. From the middle of the 20th century, not only has the number of responsible investment policies grown, but also the variety. We now see policies which are not about corporate or investor disclosure, but real-economy issues such as carbon neutrality goals, green bond standards, and modern slavery acts. Corporate ESG disclosure still dominates the scene but change seems to be on the horizon as numerous national sustainable finance strategies commence. It will be interesting to see how the different policy approaches vary region to region.

In a time of huge uncertainty, while social and governance issues have risen to the top of the agenda due to COVID-19 and climate change and biodiversity loss represent an ever-increasing threat, the unstoppable rise in responsible investment policy provides some comfort. Still, the work of the PRI’s Policy team continues. Increasing volumes of polices is crucial, but our work has been and will continue to be focused on the measurement of the practical impact of those policies, creating regulatory frameworks which not only acknowledge ESG opportunities and risks but, more importantly, manage them effectively to create a global sustainable and just society. We look forward to seeing our database continue to grow, and each datapoint becoming more successful in creating positive real-world outcomes.

This blog is written by PRI staff members and guest contributors. Our goal is to contribute to the broader debate around topical issues and to help showcase some of our research and other work that we undertake in support of our signatories. Please note that although you can expect to find some posts here that broadly accord with the PRI’s official views, the blog authors write in their individual capacity and there is no “house view”. Nor do the views and opinions expressed on this blog constitute financial or other professional advice.

References

[1] The total number of European policies equals the sum of national policies, plus EU regulations plus EU directives multiplied by the number of member states. This accounts for the fact that while EU regulation immediately takes effect in all member states, EU directives are transposed into national laws and thus create 27 different capital-market-specific laws.

[2] Note, Mainland Europe covers policies from all European Countries as well as those from the EU.

[3] To learn more about this please see our policy and regulation toolkit.