By Lubos Pastor, University of Chicago; Robert F. Stambaugh and Lucian A. Taylor, University of Pennsylvania

Investors often cite improved returns as a top motivation for applying ESG criteria, and investment managers often market sustainable investment products as offering superior returns.

Moreover, during the last decade, environmentally friendly stocks outperformed those at the opposite end of the environmental spectrum.

Of course, managers must warn clients that past performance does not necessarily predict future returns, and we believe investors should heed that warning when it comes to green assets.

Indeed, the wedge between historical returns and what investors should expect is central to our study.

What does the theory say?

Investors should expect green assets to underperform brown assets, not outperform them. As we have shown previously (Pastor, Stambaugh, and Taylor, 2021), investors should expect green assets to have lower returns because:

• many investors get satisfaction from feeling that they are investing responsibly by allocating more to green assets, while reducing or divesting their brown holdings. This relatively higher demand means that green assets command higher prices, thereby implying lower expected returns.

• green assets perform better than brown in the face of adverse climate news. These superior returns thus soften the blow of that news for green asset holders. This hedging ability also drives investor preferences, again resulting in higher prices and lower expected returns for green assets relative to brown.

What does the practice (data) show?

Lower expected returns on green assets are more than just theoretical, as our analyses of the data demonstrate.

We compute the rate of return that equates an asset’s current price to the discounted stream of its future payoffs. For a bond, this rate of return is simply its yield to maturity. For a stock, we use its implied cost of capital (ICC), as the expected stock return is not directly observable.

In both cases, this computed rate of return corresponds to the future return on the asset that an investor should expect. We then compare these expected returns for green versus brown assets.

For bonds, starting in 2020, the German government bond market has offered a clean comparison between green and non-green bonds, and the former have consistently had lower yields. For stocks, green stocks consistently had lower ICCs than brown stocks over the previous decade, with their greenness measured using MSCI environmental ratings.

Removing unexpected returns

We also look at what has driven realised returns, recognising that what was expected can differ from what really happened. Green stocks have outperformed over the previous decade because their prices rose unexpectedly, relative to brown. The principal driver of that outperformance was adverse climate news, as measured by Ardia et al. (2021).

During months in which major news outlets ran especially negative climate news, green stocks significantly outperformed brown ones. In fact, if we remove those climate-news shocks along with unanticipated earnings news, we find that green stocks would have underperformed brown stocks.

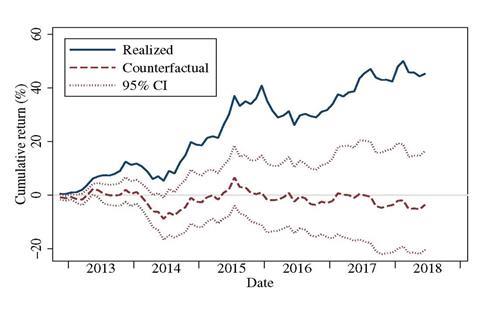

Figure 1 displays this result. The solid line shows a strongly positive realised performance of a green-minus-brown (GMB) portfolio, which goes long green stocks and short brown stocks.

The dashed line shows a modestly negative counterfactual performance of the GMB portfolio, which we estimate would have occurred in the absence of shocks to the climate and earnings. The figure shows that the realised performance substantially exceeded the counterfactual performance.

The dashed line provides a better estimate of the GMB portfolio’s expected performance going forward than the solid line. The solid line lies well above the 95% confidence interval for the counterfactual performance, indicating that the realised performance of green stocks relative to brown was significantly higher than expected.

Figure 1. Realised vs. counterfactual GMB performance

Why should adverse climate news raise the prices of green stocks and lead to unanticipated outperformance? Heightened climate concerns:

• can increase investors’ desire to hold green assets; and

• are likely to raise the expected future profits of green companies and lower the expected profits of brown companies, for example, by raising expected electric vehicle sales while increasing the likelihood of carbon taxes and regulations.

Value vs growth

Our study also offers a new insight into the contrasting styles of value and growth investing. For nearly a century, value stocks outperformed growth stocks on average. During the last decade, however, value stocks sharply underperformed growth, to an extent previously not experienced.

This historic underperformance of value stocks can largely be attributed to the outperformance of green stocks versus brown. Once we control for our green factor – the theoretically motivated difference between green and brown stock returns – most of this underperformance disappears. The simple reason is that value stocks tend to be brown on average, while growth stocks tend to be green.

Overall, our findings suggest that investors should not expect to earn superior returns on green assets in the future. Green assets did earn superior returns in the past, but this was driven by unexpected shocks that cannot be expected to repeat in the future.

The full version of our study is available on SSRN, which was presented at the PRI Academic Network Week 2022.

WATCH HERE

The PRI’s academic blog aims to bring investors insights from the latest academic research on responsible investment. It is written by academic guest contributors. Blog authors write in their individual capacity – posts do not necessarily represent a PRI view.

References

Ardia, David, Keven Bluteau, Kris Boudt, and Koen Inghelbrecht, 2021, Climate change concerns and the performance of green versus brown stocks, Working paper, National Bank of Belgium.

Pastor, Lubos, Robert F. Stambaugh, and Lucian A. Taylor, 2021, Sustainable investing in equilibrium, Journal of Financial Economics 142, 550–571.

Pastor, Lubos, Robert F. Stambaugh, and Lucian A. Taylor, 2022, Dissecting green returns, Journal of Financial Economics, forthcoming.