By Marshall Geck, Senior Specialist, Stewardship (Climate Action 100+), Washington DC

Climate Action 100+ has released its first sector strategy, with a focus on aviation. This is the first in a series of sector strategies the initiative is seeking to develop to help investor signatories push for greater ambition from focus companies.

Aviation is a carbon-intensive mode of transportation, accounting for around 2.5% of global carbon dioxide emissions from fossil fuel use, or roughly the same amount as Australia and Canada combined. At the same time, aviation is projected to grow rapidly in the 21st century and is considered a “hard to abate” sector, meaning it currently has few cost-effective and readily available options to decarbonise.

The new Climate Action 100+ sector strategy consists of recommended investor expectations to guide investor engagements with aviation companies and help ensure they are implementing robust decarbonisation plans. The strategy also contains two supporting documents: an in-depth landscape report of the aviation sector and a list of case studies showcasing good practice by aviation companies against the recommended expectations.

The strategy, which was developed by the PRI, will serve as a major new resource for investors engaging aviation companies on climate change. Investors are encouraged to use the strategy to help aviation companies align with the Climate Action 100+ goals.

Setting recommended investor expectations for the aviation sector

The recommended investor expectations are where the rubber hits the tarmac in the new strategy, helping to translate the Climate Action 100+ goals to the specific circumstances of the aviation sector.

The recommended expectations build upon the PRI’s Investor Expectations Statement on Climate Change for Airlines and Aerospace Companies published in February 2020 and align with the new Climate Action 100+ Net Zero Company Benchmark. They are intended to serve as guiding standards to support aviation companies in managing climate-related risks and opportunities, as well as proactively positioning themselves for the transition to a net-zero emissions economy. They include five detailed expectations related to specific actions aviation companies can take to decarbonise, two expectations related to climate governance, and one expectation related to climate disclosures.

Among other things, the recommended expectations call for aviation companies to set robust targets to achieve net-zero emissions by 2050. Along with this, they call for aviation company climate strategies to clearly specify the extent to which companies plan to meet their targets by cutting their own flight emissions compared to the extent which they plan to rely on carbon offsets. This is a notable request given the heavy reliance the sector has placed on offsetting to achieve many of its decarbonisation goals to date.

Also of note is an expectation for companies to lobby the major aviation trade associations—the International Air Transport Association (IATA) and the Air Transport Action Group (ATAG)—to set a net-zero emissions by 2050 strategy for the sector as a whole. These trade associations hold substantial influence and coalescing power in the aviation industry. A strategy forged under their leadership would help to secure buy-in for net-zero from the many actors in the sector and minimise the disincentive for individual aviation companies to set higher climate ambitions.

A deep dive into decarbonising the aviation sector

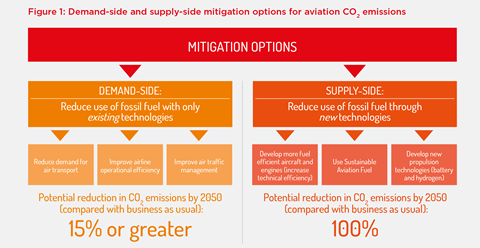

The landscape report is where the detail behind the recommended investor expectations lies. The report provides a comprehensive overview of the aviation sector and how decarbonisation can be achieved. It points to three main conclusions for investors to keep in mind during their dialogues with aviation companies:

- Supply-side solutions, such as new fuels and technologies, are the key to decarbonising the aviation sector, but these are costly and will take time to develop. Many are still at the very early stages of development and need strong policy intervention.

- Demand-side measures, such as actions to slow air transport demand, improve operational efficiencies and improve air traffic management have less overall mitigation potential. However, if combined with supply-side measures, they will reduce the overall cost of decarbonisation. Nevertheless, limiting growth in air transport demand becomes more important in a 1.5°C global warming scenario.

- Investment in Sustainable Aviation Fuels, including advanced biofuels and synthetic fuels, is the most pressing priority for action. However, there are currently limits to the availability of sustainable biofuels and high demand from other sectors. The development of synthetic jet fuels, derived from low carbon hydrogen combined with CO2, will therefore be essential.

Grounding the recommended investor expectations in real-world company actions

Before encouraging companies to take certain actions, it is natural for investors to ask: “has any company actually done this before?” Enter the case studies.

They outline examples of activities aviation companies have undertaken to date that could help align them with the recommended investor expectations for the sector. They are intended to equip investors with the power of peer pressure to push their investee companies for more ambition in their climate strategies. Featured actions include IAG’s commitment to net-zero emissions by 2050 as well as Airbus’ research into zero-emission flight technologies.

Investor engagements with aviation companies are taking off

Both the PRI and Climate Action 100+ intend to lean heavily on the new strategy in the years ahead to make progress in investor engagements with aviation focus companies. With airline and aerospace companies from American Airlines to Rolls-Royce setting net-zero emissions strategies in recent years, there’s no shortage of interest in addressing the climate impact of aviation. The aviation sector undoubtedly has a long way to go and will have its hands full addressing the fallout caused by COVID-19. However, it is our hope that the new strategy will allow investor signatories to accelerate the momentum to decarbonise, push for more aviation companies to increase their climate ambitions, and ensure that company net-zero transition plans are as robust as possible.

This blog is written by PRI staff members and guest contributors. Our goal is to contribute to the broader debate around topical issues and to help showcase some of our research and other work that we undertake in support of our signatories. Please note that although you can expect to find some posts here that broadly accord with the PRI’s official views, the blog authors write in their individual capacity and there is no “house view”. Nor do the views and opinions expressed on this blog constitute financial or other professional advice. If you have any questions, please contact us at [email protected].