By Hannes Boehm, Halle Institute for Economic Research

Regulatory bodies, rating agencies and financial analysts have warned that climate change and associated extreme weather events can threaten the sovereign creditworthiness of countries. Indeed, some nations have faced legal charges for not disclosing climate risks in their sovereign bond disclosures. But can rising temperatures and associated weather events really drive up the borrowing costs of governments, or even push countries into default? Which countries would be affected, and how could they develop resilience towards these threats?

Approach and related literature

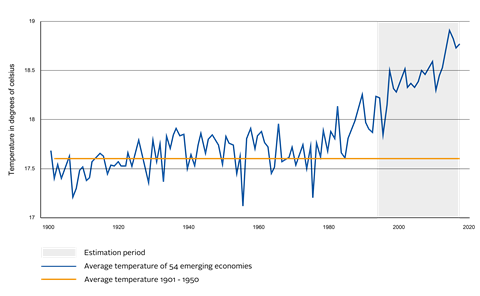

In a recent paper, I show that, for vulnerable emerging market economies, rising temperatures are indeed linked to significantly lower sovereign creditworthiness. I construct a simple proxy for the degree of global heating that countries have experienced so far, as Figure 1 illustrates. It depicts the mean annual temperature of 54 emerging market economies, from 1901 to 2018, showing an upward trend in global temperatures since the second half of the 20th century. From 1994 onward, I calculate the countries’ temperature deviation from their 1901-1950 average. With a mean of 0.84°C, this deviation is close to the 1°C global heating trend that the IPCC (2018) has estimated since pre-industrial levels.

Figure 1: Average annual temperature of 54 sample countries and 1901-1950 temperature average.

Climate-related natural disasters, infectious diseases and other threats to natural and human livelihoods are projected to increase dramatically with further warming, while the warming trends seen so far have already led to more extreme weather events that can cause significant economic damage (IPCC 2018).

This development is confirmed by a wide literature that links temperature increases to lower GDP growth in poorer and warmer countries (Burke et al. 2015, Dell et al. 2012), reduced firm productivity and output (Zhang et al. 2018), decreasing labour supply (Graff Zivin & Neidell 2014) and more interpersonal and civil conflict (Hsiang et al. 2013). As these factors affect countries’ economic performance and political stability, they should also have an impact on the pricing of sovereign bonds in financial markets.

Initial results

Some initial statistics seem to indicate a negative relationship between temperature and economic performance across the 54 countries. Table 1 shows that temperature anomalies, i.e. the difference between current and past temperature, are much higher when a country suffers from heat-related natural disasters such as droughts or wildfires. It is straightforward to assume that such disasters can cause massive economic damages and thus affect sovereign risk. Table 2 indicates that during periods of high temperature anomalies (>75th percentile), stock market returns are lower, GDP growth is weaker, and governments run into higher deficits, compared to low temperature anomalies (<25th percentile).

Table 1: Mean temperature anomaly measure during natural disaster periods.

| Full sample mean | Drought | Drought with reported damage | Wildfire | Heat wave | Cold wave or severe winter | |

|---|---|---|---|---|---|---|

| Historical temperature anomaly full sample | 0.842 | 0.898 | 0.946 | 0.989 | 0.988 | 0.0623 |

Source: International Disaster Database

Table 2: Mean of economic variables during high and low temperature anomalies.

| Overall mean | Mean if historical temperature > 75th percentile | Mean if historical temperature < 25th percentile | |

|---|---|---|---|

| Stock market returns (38 countries) | 0.233 | -0.0478 | 0.434 |

| Quarterly GDP growth (full sample) | 0.981 | 0.937 | 1.061 |

| Government primary surplus in % of GDP (42 countries) | -0.235 | -0.693 | 0.400 |

Source: MSCI, S&P, Oxford Economics, IMF Fiscal Monitor. Note: This table shows the overall mean of economic variables (stock returns, GDP growth, and government primary surpluses) and their differentiation during high and low temperature anomalies.

To establish more formal evidence and to link climate trends specifically to sovereign creditworthiness, I analyse monthly data for the 54 emerging economies from 1994 to 2018. I regress the market returns of the Emerging Market Bond Index (EMBI), a common measure for sovereign debt performance, on the described temperature anomaly fluctuations, controlling for precipitation and including country and region-time fixed effects on the month-year level. The captured temperature shocks are thus idiosyncratic and account for weather trends common to each region.

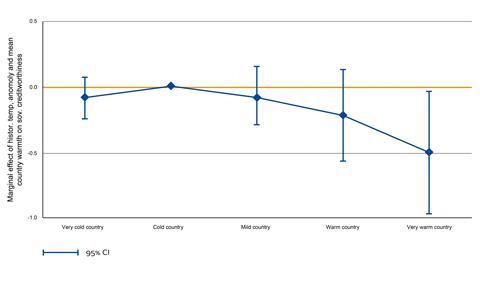

My results show that warm countries are significantly more susceptible to temperature shocks than cold or mild-tempered countries. Figure 2 depicts this relationship. For very warm countries – those in the highest quintile of average annual temperature – a temperature increase has a negative and statistically significant effect on sovereign creditworthiness (i.e. lower EMBI returns).

Figure 2: Estimated effects of temperature increases on sovereign creditworthiness

The effects of temperature increases for the warmest countries can be substantial – a 1°C increase in monthly temperature lowers EMBI returns by 0.432 percentage points on average. This corresponds to 11.1% of the EMBI returns’ overall standard deviation. Thus, in a 2°C global heating scenario, EMBI returns could be lowered for affected countries by roughly a quarter of their overall standard deviation.

While such future projections must be treated carefully, this magnitude is considerable and could lead to rising sovereign borrowing costs, or even defaults, for warmer countries in the next decades.

How can countries strengthen their resilience towards climate-induced sovereign credit risk?

My results indicate that improving institutional quality can be a promising measure to curb temperature-induced sovereign risk. Countries with stronger rule of law, control of corruption, civil rights, democratic governments or more progressive tax systems face a statistically significant weaker marginal effect of temperature increases on sovereign creditworthiness. Climate-related metrics yield a similar conclusion – countries with higher values in the ND-GAIN index, which measures a country’s adaptiveness and vulnerability towards climate change, face significantly lower temperature shock effects on their sovereign risk level.

These results suggest that higher climate-related institutional quality could improve the resilience and adaptiveness of emerging economies towards climate change. This can be the case, for instance, if droughts or floods lead to physical damages that require swift government intervention, or if distributional consequences of temperature-induced costs and losses need to be managed efficiently.

Conclusion

My evidence suggests that historical temperature deviations, approximating physical climate change, can significantly lower the sovereign bond performance of those emerging economies that are already warmer on average. Investors and regulators should monitor these risks carefully because, if past trends are any guidance, affected countries could face meaningful increases in their sovereign debt costs as climate change intensifies. In addition to lowering global CO2 emissions, strengthening institutions could provide resilience towards rising temperatures.

This blog is written by academic guest contributors. Our goal is to contribute to the broader debate around topical issues and to help showcase research in support of our signatories and the wider community.

Please note that although you can expect to find some posts here that broadly accord with the PRI’s official views, the blog authors write in their individual capacity and there is no “house view”. Nor do the views and opinions expressed on this blog constitute financial or other professional advice.

If you have any questions, please contact us at [email protected]

References

Burke, Marshall; Hsiang, Solomon M.; Miguel, Edward. 2015. Global non-linear effect of temperature on economic production. Nature 527(7577), 235-239.

Dell, Melissa; Jones, Benjamin F.; Olken, Benjamin A. 2012. Temperature shocks and economic growth: Evidence from the last half century. American Economic Journal: Macroeconomics 4(3), 66-95.

Graff Zivin, Joshua; Neidell, Matthew. 2014. Temperature and the allocation of time: Implications for climate change. Journal of Labor Economics 32(1), 1-26.

Hsiang, Solomon M.; Burke, Marshall; Miguel, Edward. 2013. Quantifying the influence of climate on human conflict. Science 341(6151).

IPCC. 2018. Global Warming of 1.5°C. An IPCC Special Report on the impacts of global warming of 1.5°C above pre-industrial levels and related global greenhouse gas emission pathways, in the context of strengthening the global response to the threat of climate change, sustainable development, and efforts to eradicate poverty (Summary for Policymakers).

Zhang, Peng; Deschenes, Olivier; Meng, Kyle; Zhang, Junjie. 2018. Temperature effects on productivity and factor reallocation: Evidence from a half million Chinese manufacturing plants. Journal of Environmental Economics and Management 88, 1-17.