Toby Belsom, Director of Investment Practices, PRI

At the end of July the PRI launched a discussion paper around the coalescence of two of the fastest growing strategies within asset management – passive and ESG. These trends are overlapping and merging in various ways but – as with many new markets and financial products – issues remain. Our survey is starting to yield interesting starting points across a range of topics, such as regulation, benchmark selection, benchmark construction and the EU taxonomy.

ESG incorporation: new products, new benchmarks – new issues…

There are now thousands of ESG indices available to institutional and retail clients – with a plethora of criteria for index construction, ranking of corporates and reporting to clients about index or benchmark construction. But many of these funds struggle with the ‘sniff’ test – would the consumer agree with the inclusion of company X or Y in their ESG fund?

Initial feedback from our survey includes discussion around issues such as:

- How should service providers or asset managers improve the lack of clarity around benchmark construction?

- What is, or should be, the role of financial regulators in developing and policing ESG indices or benchmarks, to improve transparency around how they are constructed?

- How can the industry raise disclosure standards around benchmarks?

- Do asset owners understand possible portfolio skews introduced when selecting an ESG benchmark?

- What is the possible impact of the EU taxonomy?

- Answering some of these challenges will be a crucial and timely step if the industry is not to be caught up in accusations of greenwashing.

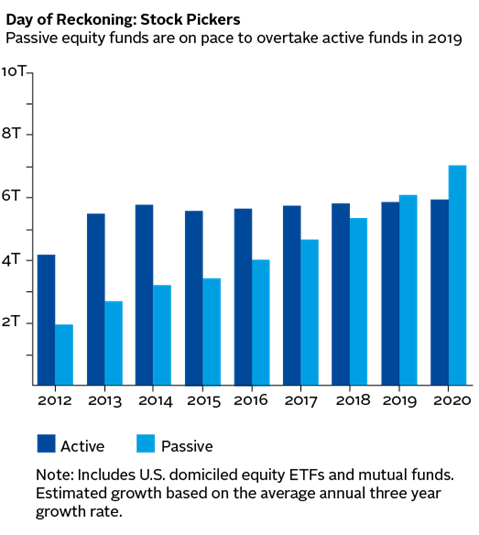

Active ownership vs passive management

The rise in AUM invested under passive strategies has raised questions from industry experts and academics about what the impact will be on the governance of listed companies, and from the concentration of shareholder power among a small group of passive investors. Perhaps these concerns are what’s driving some of the most pessimistic responses to our survey: that passive strategies are fundamentally incompatible with active ownership – a view that would have important implications for the passive managers’ ability to implement Principle 2 of the six Principles for Responsible Investment.

“Principle 2: We will be active owners and incorporate ESG issues into our ownership policies and practices.”

Other areas of discussion include:

- Do financial regulators need to revisit the role and influence of proxy advisers?

- Is divestment due to ESG issues a viable strategy for passive investors?

- How do asset managers resource proper engagement programmes on portfolios that are diverse and include thousands of companies?

- Should active and passive investors look to work together more effectively in the promotion of ESG-relevant issues such as disclosure?

One interesting discussion around some of these responses has been around the role of asset owners. On one hand asset owners are attracted by the siren of passive investing – low costs, evidence of the relative benefits of active versus passive management and new financial products such as exchange-traded funds. But how can asset managers properly resource engagement teams when clients are demanding ever cheaper products? Should asset managers be more explicit about the costs (and benefits) of well-resourced engagement programme?

Get involved

Our survey is starting to reflect a broad range of comments, and we encourage anyone operating in this area who hasn’t already done so to respond. The results will guide the PRI’s thinking, and the support and guidance we will provide on how the investment industry can bring these two huge trends together.

This blog is written by PRI staff members and guest contributors. Our goal is to contribute to the broader debate around topical issues and to help showcase some of our research and other work that we undertake in support of our signatories.

Please note that although you can expect to find some posts here that broadly accord with the PRI’s official views, the blog authors write in their individual capacity and there is no “house view”. Nor do the views and opinions expressed on this blog constitute financial or other professional advice.

If you have any questions, please contact us at [email protected].