By Pilar Garcia-Gomez (Erasmus University, Rotterdam), Ernst Maug (University of Mannheim), and Stefan Obernberger (Erasmus University, Rotterdam)

Private equity buyouts have often been associated with a large turnover of the labour force, while the sources of value creation in buyouts have been the topic of much debate.[1] The academic literature on buyouts attributes value creation to gains in productivity and operational improvements. By contrast, public commentators often cite transfers from other stakeholders, notably employees, as a major source of value creation. Meanwhile, little is known about the impact of restructuring on employees, beyond income and employment, and even less is known about how companies identify those employees that are laid off during restructuring.

Our paper puts employees’ health at the centre of both questions. Health is a critical component of human capital, and human capital plays a major role when firms restructure their operations by laying off workers and reassigning jobs. Poor health makes employees less productive, and we expect that it makes them more vulnerable to wage cuts and job losses, especially during restructuring. Conversely, a more demanding work environment and job insecurity may negatively affect employees’ well-being and their health.

The main result of our study is that if an employee’s health condition negatively affects his or her productivity, then the buyout will dramatically increase their human capital risk. Surprisingly, we do not find evidence that private equity buyouts make employees sick.

Our data set includes 55,752 employees of 274 Dutch buyout targets in the period from 2007 to 2013. We match buyout employees to a control sample based on a range of firm-level and individual-level characteristics. We track employees until the fourth calendar year after the buyout and analyse data on their detailed consumption of prescription medicines (such as antidepressants or cardiovascular), the total number of medications they take, and their total annual health expenditure. Furthermore, we collect data on employees’ employment history after buyouts and record their main source of income (employment, self-employment, disability insurance, retirement income, unemployment insurance), job changes, and the wages of those who are employed.

Employees in poor health have the highest human capital risk

In a first step, we analyse how private equity buyouts affect the human capital of buyout employees. Our results are similar to those of an earlier study of German private equity buyouts: buyout employees have higher human capital risk. Employees in our sample of Dutch private equity buyouts lose about €1,300 per year by the fourth calendar year after the buyout, or about 3.7% of the median wage of target employees. Our analyses also reveal that the loss in earnings is driven by loss of employment; there is no evidence that wages are cut.

In the next step, we investigate whether job losses and income affect employees in poor health more. We expect that employees in poor health are less productive, and that buyout firms identify – and then lay off – less productive workers.[2] This argument does not assume that buyout firms have access to employees’ health records, which are confidential; only, that firms observe their employees’ productivity. We find this to be the case, and the effect is large: in addition to the baseline loss experienced by all buyout employees, employees on cardiovascular medication lose another €2,500 per year and those on antidepressants another €2,000 per year in the fourth year after the buyout, relative to matched control employees. The losses for employees on multiple medications are even larger.

There is a strong link between health, productivity, and career paths

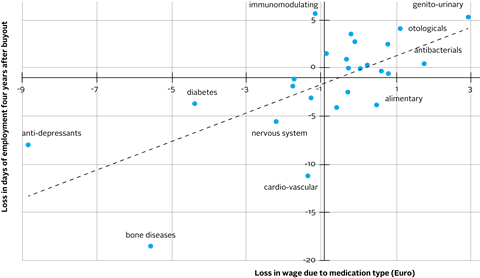

We relate the income reduction and employment of employees in poor health to their productivity using a two-step procedure. In the first step, we estimate the link between the consumption of a wide-range of medications and wages for the entire Dutch population. These estimates provide us with measures of how sensitive individual productivity is to certain types of medications in the general workforce. In the second step, we use these estimates to predict how much less our sample employees would earn compared to healthy employees if their wages fully reflected their health status. We do this analysis for 25 groups of medications for which we have data and find a remarkably strong correlation, depicted in Figure 1. If buyout employees are prescribed medications that are associated with a negative (positive) impact on the wages of the entire Dutch workforce, then these employees are also significantly more (less) likely to lose employment at the buyout firm. For example, taking anti-depressants is associated with a reduction of €8.61 in the average Dutch employee’s daily wage, and the employees of private equity targets on anti-depressants lose on average 8.06 days of employment per year by the fourth year after the buyout.

Figure 1: Medication-based estimates of loss in productivity (wages) and employment outcome after private equity buyouts

Finally, we ask whether buyouts have a negative impact on employees’ health. Based on prior literature, we expect that buyout-related restructuring has a negative impact on employees’ health by creating a more demanding and stressful work environment and job insecurity associated with layoffs, which should lead to anxiety-related stress for those who remain employed with the target company. Our findings do not support this conjecture. However, we find a strong association between career paths and health outcomes for buyout employees and control employees alike: the health of those who find new jobs tends to improve, whereas the health of employees who become unemployed deteriorates. Buyouts affect employees’ career paths, and those who move to new jobs are in better health, whereas those who become unemployed are in poorer health. Importantly, those who stay with the target company do not experience a significant change of their health.

Does the social security system encourage employees in poor health to leave their jobs?

Our results may bring along some interesting insights for policy makers. We find that about half of the impact of buyouts is buffered by social transfers through retirement benefits, disability insurance, and unemployment insurance. Therefore, total income losses are cushioned by the Dutch social transfer system, and this protection is larger for previously unhealthy workers. The social transfer system may alleviate some of the adverse health consequences of buyouts on affected employees. Unfortunately, we cannot further test these theories with our data and within our institutional setting, so they remain open for further research.

Our paper is available here.

Agrawal, A., Tambe, P., 2016. Private equity and workers’ career paths: The role of technological change. Review of Financial Studies 29, 2455–2489.

Antoni, M., Maug, E., Obernberger, S., 2019. Private equity and human capital risk. Journal of Financial Economics 133, 634–657.

Contoyannis, P., Rice, N., 2001. The impact of health on wages: Evidence from the British household panel survey. Empirical Economics 26, 599–622.

Currie, J., Madrian, B. C., 1999. Chapter 50 Health, health insurance and the labor market, Elsevier, pp. 3309–3416.

Davis, S. J., Haltiwanger, J., Handley, K., Jarmin, R., Lerner, J., Miranda, J., 2014. Private equity, jobs, and productivity. American Economic Review 104, 3956–90.

Flores, M., Fernández, M., Pena-Boquete, Y., 2019. The impact of health on wages: evidence from Europe before and during the great recession. Oxford Economic Papers pp. 1–28.

Jäckle, R., Himmler, O., 2010. Health and wages: Panel data estimates considering selection and endogeneity. The Journal of Human Resources 45, 364–406.

Olsson, M., Tag, J., 2017. Private equity, layoffs, and job polarization. Journal of Labor Economics 35, 697–754.

This blog is written by academic guest contributors. Our goal is to contribute to the broader debate around topical issues and to help showcase research in support of our signatories and the wider community.

Please note that although you can expect to find some posts here that broadly accord with the PRI’s official views, the blog authors write in their individual capacity and there is no “house view”. Nor do the views and opinions expressed on this blog constitute financial or other professional advice.

If you have any questions, please contact us at [email protected].

References

[1] See Davis et al. (2014) for an establishment-level analysis and the earlier literature they cite. See Olsson and Tag (2017), Agrawal and Tambe (2016), and Antoni et al. (2019) for individual-level studies.

[2]E.g., Currie and Madrian (1999), Contoyannis and Rice (2001), Flores et al. (2019), Jäckle and Himmler (2010).