This article summarises key points from a workshop held in 2022 for private equity general partners (GPs) that are at an early stage in developing their climate-related investment practices.

The session brought 21 participants together with two industry experts to provide practical guidance and address common questions related to integrating climate considerations in private equity.

The participating private equity GPs were located across Europe, the US, and Latin America; varying in strategy, size, and AuM. They also differed in their level of climate sophistication.

Although most attendees (92%) incorporated climate considerations in their ESG policies and had an ESG committee, only 23% had a senior/board-level representative responsible for firm-level ESG incorporation and carbon footprint tracking.

Around 15% offset their firm-level Scope 1 and 2 carbon emissions; while 8% had firm-level climate targets and requested Scope 3 carbon footprint data from portfolio companies.

Key take-aways

1. Incorporating climate risk in investment decision making

GPs can begin by identifying climate risks for incorporation into their investment decisions. Considering the relevant sector(s) and specific aspects of each deal can help them determine which risks are most applicable.

2. Carbon footprint data

GPs need to engage with their employees and investees to determine their Scope 3 emissions, which are likely to represent the largest part of their carbon footprint. The quality of investee data will vary – GPs can play a role in collecting the data or help investees improve its quality through their engagement.

3. Target setting and engagement with portfolio companies

Broader uptake among GPs is needed at the firm level, something industry initiatives can help to facilitate. Portfolio companies’ science-based targets are independent of their investors; engaging companies to set these targets can have a lasting impact after exit.

4. Carbon offsetting

Carbon offsetting is difficult for GPs, and further industry collaboration is needed to consider how the net-zero transition will be achieved (and how offsetting should happen in practice).

5. Seeking external support

GPs should collaborate with peers and external partners and use industry guidance and standards to start integrating climate considerations into their investments.

About the experts

The session was led by two senior responsible investment professionals from investment managers referred to in this summary as GPI and GPII. Both GPs are active members of the Initiative Climat International (iCI), a global, practitioner-led community of private equity investment managers and asset owners that seek to better understand and manage the risks associated with climate change.

GPI is a private equity investment manager primarily focused on European and US buyouts in software and services. GPII is an investment manager offering private equity, credit, and real asset strategies across multiple regions and sectors. Both firms have had their science-based targets (SBTs) validated by the Science Based Targets Initiative.

1. Incorporating climate-risk in investment decision making

The discussion started with an overview of how the experts incorporate transition and physical climate risks into their investment decision making, in line with the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD).

They presented some questions that GPs can consider when determining how their existing and potential investments may be impacted by these risks, which we highlight below.

Transition risks

Policy and legal risks

- Which regulations apply to you on a firm level[1] or to investees?

- How will future regulations affect your firm or investees? Will operating costs increase?

For example, enhanced emissions reporting obligations may lead to higher compliance costs internally and for portfolio companies, while new regulations on existing products may lead to increased insurance premiums for portfolio companies, and asset impairment for the investors.

Technology risks (from transitioning to lower-emission technologies)

- Are there lower-emission substitutes for investees’ existing products and services? How much do they cost?

- Will investees have to write off any existing assets?

- What is the likelihood that investments in new technologies will be unsuccessful?

The experts recommended that GPs consider the industries that their existing and potential holdings service, and whether those technology offerings will remain relevant or viable. For instance, a company with an oil and gas trading platform is likely to face reduced demand as the global economy moves away from fossil fuels.

Market risks (changing customer behaviour, uncertain market signals, increased raw material costs)

- What are the inputs in an investee’s supply chain for its core product or service and how will they be affected by market risks?

For example, if investing in a technology company that produces B2B software, GPs could consider the company’s data centres, the energy they consume, the potential future cost of this, and whether to outsource their management or not.

Reputational risks

- Does a sector face scrutiny by stakeholders or broader society? Is this likely in future?

The experts recommended that before making an investment, GPs should assess whether an investee’s individual products could contribute to a negative sustainability outcome (for example, climate change) to determine the extent to which they face reputational risks.

Physical (acute and chronic) risks

Acute risks concern extreme weather events that are predicted to increase in severity and frequency. Chronic risks refer to longer-term changes such as rising temperatures, sea levels, and ocean acidification. GPs can consider if their existing or potential investees are likely to face:

- reduced revenues because of decreased production capacity, caused by issues such as transport and supply chain disruptions;

- reduced revenues and increased costs due to negative impacts on workforce health and safety and increased employee absenteeism; and

- damaged assets, leading to write-offs and increased capital expenditure.

Putting theory into practice

“How do you practically understand what those risks are in an investment?”

Participants noted that it can be difficult to understand which climate risks are applicable to an investment in practice. The experts suggested that considering the relevant sector(s) can help inform this process.

For example, the software sector does not have much exposure to transition risks, so before making an investment, GPI will screen for those transition risks most relevant to the industry of a company’s customers. Post-investment, it determines risks based on where a company, its suppliers, and data centres are located. The GP uses a bespoke tool developed with a consultant, which is designed to be simple but also considers the main climate-risk models in the market.

GPII takes a different approach. Every deal under consideration by the investment committee receives a climate score that incorporates physical and transition risks. It uses a tool that weights risks 60-40 in favour of transition risk, as physical risk information is generally available at a country level only.

The tool uses publicly available data and identifies chronic and acute physical risks in whichever region assets are located, with reference to SASB climate metrics.

Higher-scoring companies – those that exhibit higher climate risks – are asked more specific questions about the governance arrangements they use to manage these (e.g. who is responsible and how sophisticated is their understanding of the risks?).

The experts emphasised that GPs do not need to use bespoke tools unless they are screening a large number of companies. Smaller private equity managers can embed third-party tools into their investment processes and refer to them in deal documentation shared with their investment committees.

The SASB climate bulletin is a useful starting point for GPs as it maps physical and transition risks of 77 sectors, along with key metrics. Although this indicates what a GP should consider for an investment in a particular sector, participants noted that it is imperative to consider the nuance of each deal.

“Do you encounter any resistance from deal teams when implementing climate-related considerations?”

Participants also raised concerns about investment teams being reluctant to implement climate-related considerations. The experts noted that having good governance structures in place, with leadership teams that understand the importance of doing so, can help avoid or reduce such barriers.

Demonstrating that climate considerations can highlight opportunities as well as risks can also help to overcome investment team scepticism. For instance, a company producing grape-derived goods had a high physical risk score due to the potential impact of drought conditions on its suppliers.

Consequently, GPII employed specialist wine consultants who identified that certain climate scenarios would increase the grapes’ sugar concentration, and actually improve the quality of the company’s products.

2. Carbon footprint data

According to a survey conducted at the beginning of the session, 23% of participants did not track their firm-level carbon footprint. The experts provided a brief overview of carbon footprinting: namely, that a footprint is calculated by multiplying operational activity (which results in GHGs) data by an emissions factor (a ratio of the amount of GHGs emitted per unit of a given activity), resulting in tonnes of carbon emissions.

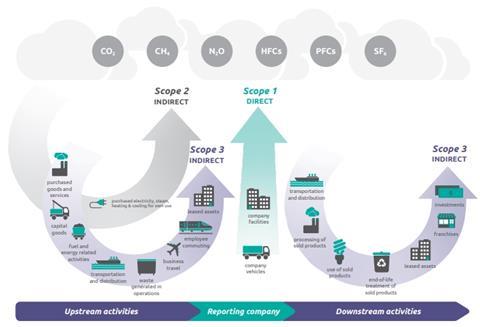

To capture a firm-level carbon footprint in compliance with the Greenhouse Gas Protocol, GPs need to calculate emissions resulting from their direct and indirect activities, as highlighted in Figure 1.

Figure 1. Overview of GHG Protocol scopes and emissions across the value chain. Source: Greenhouse Gas Protocol

Scope 3 emissions

For many GPs, Scope 3 emissions will represent most of their firm-level carbon footprint, especially those derived from their business travel and – crucially – their investments (known as financed emissions). As such, much of the discussion focused on how participants could measure these.

Noting that pre-COVID business travel represented over 85% of their Scope 3 footprints, the experts emphasised that GPs need to engage their employees to better understand the impact of their own activities, and more importantly, engage with, and set targets for, their portfolio companies.

Figure 2: Example GHG emissions inventory for a GP. Source: ERM

GPI looks at the Scope 3 emissions of all its portfolio companies, covering five out of 15 GHG Protocol categories.

GPII has recently made firm-level commitments to the SBTi that require it to engage with portfolio companies around all Scope 1 and 2 emissions and some Scope 3 emissions. It prioritises engaging portfolio companies that are covered by its SBTs, as these are required to develop and validate its own targets within a certain period of investment.

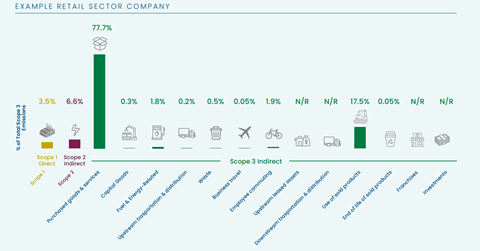

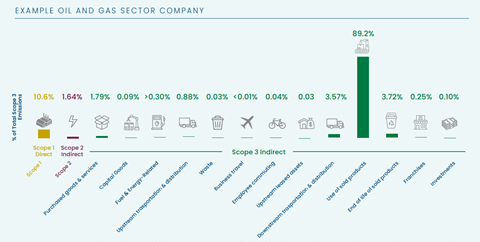

The discussion highlighted that sectors have different footprint breakdowns across the Scope 3 emissions categories, and GPs should tailor their company engagements accordingly.

For example, most of an average retail sector company’s Scope 3 emissions will stem from the goods and services it purchases (see Figure 3), while the highest Scope 3 emissions from an average oil and gas sector company will come from the use of products it has sold (see Figure 4).

Figure 3: Example GHG emissions inventory for a retail sector company. Source: ERM

Figure 4: Example GHG emissions inventory for an oil and gas sector company. Source: ERM

Data quality, collection and calculation

Ideally, GPs use primary data from portfolio companies and supplier emissions – such as hours of electricity consumed, or kilometres travelled – to calculate a portfolio’s carbon footprint. The experts noted that investees’ data gathering abilities varied depending on their maturity, adding that GPs should use what is available while working with them towards obtaining more accurate primary data.

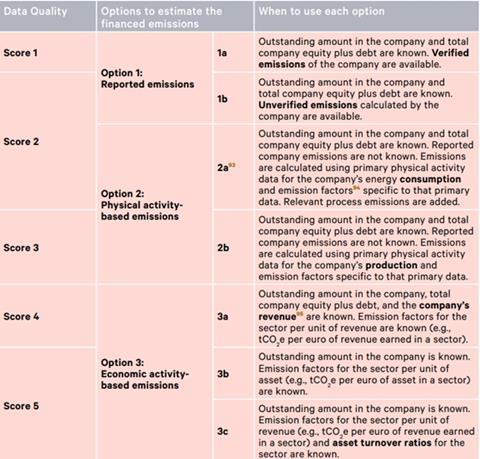

Where reported emissions are not available (which can often be the case with less mature companies), GPs must make more assumptions. The experts discussed how to do so through other means, outlined by the Partnership for Carbon Accounting Financials (PCAF) (highlighted in Figure 5).

Figure 5: Data quality score table for business loans and unlisted equity. Source: The Global GHG Accounting and Reporting Standard for the Financial Industry

(Score 1 = highest data quality; score 5 = lowest data quality)

GPI uses spend-based data – the expenses associated with a particular activity, e.g., USD spent on air travel – and multiplies it by the associated emissions factor. This is a more conservative approach and estimates a larger footprint, to account for potential errors.

Using an average data methodology can produce a more precise estimate. For example, substituting an area’s average footprint per square meter of office space for the kilowatt hour usage of an office. Where access to data is very challenging, GPII takes this approach, using proxy data from the CDP to produce estimates.

Data collection for a portfolio of companies is time consuming, and the timeline will vary depending on business size. As such, it is important to communicate with portfolio companies around data collection expectations as early as possible after acquisition.

Indeed, the experts explained that GPs can play a role in helping investees to calculate their footprints, for example, by creating a questionnaire on a footprint calculation platform, which includes the relevant GHG protocol emissions categories and associated emissions factors, and where the response fields request information around various operating activities. GPs can also take a hands-off approach, letting companies select the platforms, systems, or consultancies that can help them with these calculations.

GPII typically works with a consultancy to collate data from portfolio companies. The consultant prepares a data collection template that the GP asks its holdings to complete with primary data.

Engaging portfolio companies directly reduces GPII’s costs and the consultant’s time significantly.

Once the data is collected, GPs can use it to inform their firm-wide carbon footprint calculations. GPII noted that using a third party to review collected data is considered best practice as it strengthens the credibility of the calculations, especially when reporting to limited partners (LPs).

Fund-level reporting

The discussion also touched on fund-level reporting. As outlined in iCI’s recent GHG Accounting guidance, GPs should include 100% of scope 1, 2, and 3 emissions from portfolio companies when reporting their fund-level emissions.

GPs should include financed emissions (scope 3, category 15) associated with a fund in their public disclosures. These are calculated by multiplying an attribution factor (value of debt or equity in the portfolio company / total equity and debt) by the total portfolio company’s emissions. This provides the proportion of a company’s emissions for which the fund must report on.

“Do you use carbon footprinting software systems?”

Participants wanted to understand whether the experts use carbon footprinting software systems. The experts discussed that using such systems can empower portfolio companies to collect data and track it over time, while they are not always necessary.

The experts agreed that a portfolio’s characteristics (e.g. its size, sector and geographical exposure) determine whether to develop a bespoke, internal system, or to engage consultants to estimate a more complex carbon footprint manually.

Once a GP has estimated its firm-level and portfolio company emissions, it can set emission reduction targets at both levels and take action towards achieving them.

3. Target setting and engagement with portfolio companies

Roughly 90% of attendees did not set any firm-level climate targets. The experts highlighted that encouraging senior management at GPs to set targets is one way to improve firm-level carbon footprints.

GPs can start by setting a firm-level target to reduce Scope 1 and 2 emissions by a certain date. To achieve their target, GPII will need to consider its office locations and switch to renewable energy tariffs, among other actions.

Participants discussed the benefits of GPs setting firm-level targets: doing so shows their LPs that they take climate risk seriously, it engages their senior management on climate matters and provides portfolio companies with an example to follow.

However, for most private equity GPs, particularly those focused on venture capital, Scope 1 and 2 emissions are likely to be low. It is thus important that they focus on Scope 3 financed emissions that result from portfolio companies and their products and services.

According to the experts, setting SBTs that are validated and approved by the SBTi is the most credible way of doing this. The SBTi guidance recommends that private equity firms set targets for all relevant investments[2] by 2040. GPII’s engagement strategy is focused on driving portfolio companies to adopt an SBT.

When working with portfolio companies on developing their SBTs, GPs need to consider that the SBTi has an approval process and should factor in the time needed to get portfolio company management buy-in and board approval, and to formulate a credible decarbonisation plan.

The discussion also highlighted the fact that portfolio company SBTs are independent of investors – an investee’s annual reporting obligations continue once a GP has exited its investment. Being aligned with a robust SBT avoids GPs and their investees facing accusations of greenwashing.

Only 12 private equity firms have set approved SBTs so far and broader industry uptake is needed – something that initiatives such as the Net Zero Asset Managers Initiative and the iCI can help to facilitate.

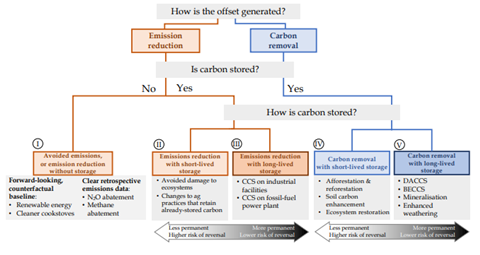

4. Carbon offsetting

The discussion also focused on distinguishing between avoidance and removal offsets, echoing the Oxford Principles for Net Zero Aligned Carbon Offsetting (see Figure 6).

Avoidance offsets prevent carbon from being released into the atmosphere, for instance by protecting a rainforest. Removal offsets look to extract carbon from the atmosphere, using carbon capture technology or by planting trees, for example.

Figure 6: Taxonomy of carbon offsets. Source: University of Oxford (2020) The Oxford Principles for Net Zero Aligned CarbonOffsetting

“How do you investigate the quality of carbon offsets?”

Only 15% of workshop attendees offset their firm-level carbon footprint (excluding their investments), reflecting the fact that this is difficult for private equity GPs to undertake.

The experts recommended that GPs consider the future trajectory of carbon prices in their offset strategies. They added that only offsetting Scope 1 and 2 emissions would have minimal impact on global emissions and that it was best practice to use third-party verified carbon removal offsets for Scope 1, 2 and 3 emissions.

The experts noted that the voluntary offset market is unregulated and open to manipulation, making it difficult for GPs to incorporate offsets within their climate strategies. For example, GPII worked with a portfolio company in the aviation industry to offset its emissions, but the price of offsets rose every week and the underlying projects linked to the offsets became oversubscribed within days, making them hard to access.

The discussion concluded that the private equity industry needs to consider how the net-zero transition will be achieved and to determine how offsetting should happen in practice. The SBTi has released draft guidance, based on consultations, which is now being reviewed by industry stakeholders.

5. Seeking external support

The experts shared the following recommendations for GPs to conclude the session:

- GPs are encouraged to find external partners and support to help them develop their initial climate-related practices (e.g. carbon footprinting) as small ESG teams will not always have the capacity or expertise to undertake or implement these.

- GPs should use the guidance and standards which are available to ensure they meet the expectations of regulators and LPs.

- GPs should collaborate with and learn from peers, both of which are benefits of joining the iCI.

CREDITS: Authors: Diba Ahour, Daram Pandian | Editor: Jasmin Leitner | Design: Will Stewart

Downloads

Introductory climate session for private equity GPs March 2023

PDF, Size 0.8 mb