Thalia Vounaki, the PRI’s Senior Manager, Data talks the PRI’s Digital Communications Manager, Ruth Wallis, through the major RI trends among PRI signatories

1,710 reporters,a 17% increase |

$86.3trnin AUM, an increase of 6% |

591opted into climate reporting |

Tell me about a day in the PRI data team once the reporting cycle has closed

It’s 1 April. The deadline for signatories to submit their annual responses to the PRI Reporting Framework – a detailed questionnaire on RI organisational practices – has officially passed. The emails from my colleagues start flooding in. When can we access the data with signatory reporting responses? What does this year’s data tell us about ESG practices? Their eagerness is justified and welcome. After all, 205 service providers and 1,710 investors representing US$86.3 trillion submitted their responses to the 2019 Reporting Framework, 17% more than last year. So, as the world’s largest database of investors’ RI practices, it is the go-to source for RI insights and is used to support several of the PRI’s work streams.

And that’s why we run validations on the responses. Lots of them. Indeed, until mid-April we were busy contacting 580 signatories to confirm their responses to questions that our checks picked up.

In which markets has the PRI grown most over the past year?

By the end of March 2019, the amount of PRI asset owner signatories had grown by 16%, reaching 432 with US$20 trillion in AUM. However, there are still two thirds of the top 300 largest pensions that are not PRI signatories, and in some markets the investment industry is not yet fully onboard with responsible investment.

The PRI is growing in both developed and developing markets, with a 71% growth in Asia (+18 investors) and 20% in the US (+52 investors). In total, 433 new signatories joined the PRI in 2018-2019, accounting for 21% of the 2,092 overall. However, these signatories only make up 8% of all PRI signatories’ AUM. This suggests that the latest signatory growth is predominantly among smaller investors.

In addition, the pension industry is managed by thousands of small pension funds in several markets, which adds up to a sizeable segment of the global pension market. These pension funds tend to be resource-constrained and so use asset managers. While most of those smaller asset owners are not PRI signatories, they benefit from the PRI’s signatory base indirectly, as the PRI has an 84% market penetration among the largest 500 asset managers,. By setting minimum requirements investors must meet to maintain signatory status, the PRI is driving change among asset managers, the benefit of which will extend to small asset owners who manage their assets externally.

Overall, we expect strong growth to continue over the next years!

Where have we seen the most progress over the past three years?

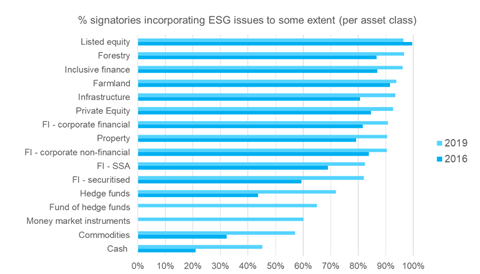

Back in 2016, ESG incorporation was the norm in listed equity, along with farmland, with over 90% of signatories reporting doing so. By 2019, investors have progressed with ESG incorporation in fixed income assets, in particular among SSA bonds (82% compared to 69%) and securitised bonds (82% vs 59%). However, what has been more surprising is the rise of responsible investment in assets not traditionally known for RI; from 44% to 72% in hedge funds and from 21% to 45% in cash assets. This aligns with findings from the 2018 European SRI survey conducted by Eurosif.

The PRI, recognising the need to push RI in hedge funds, released a due diligence questionnaire for hedge funds in 2017 and introduced hedge fund-specific questions in the 2019 Reporting Framework. On fixed income, the PRI published a series of resources for fixed income assets, in particular SSA bonds, and has been an advocate of bondholder engagement.

Did you just say bondholder engagement?

Among the many questions the reporting team receives from signatories, one of the most common is around bondholder engagement, specifically SSA bonds. Indeed, 58% of all SSA bondholders reported in 2019 that they engage on ESG issues. To be fair, most investors who do engage on their directly held bonds do so mostly on less than 50% of their fixed income assets, and just 10% do so on the majority of their SSA bonds. You can read case studies on how PRI signatories do this here.

Climate action is one of the PRI’s strategic objectives, so it is encouraging that 84% of asset owners and 82% of managers report taking action on this. In 2016, just 69% and 62% respectively of the same investors did. The most common steps taken include investing in climate-resilient investments and using emissions data to inform investment decision making.

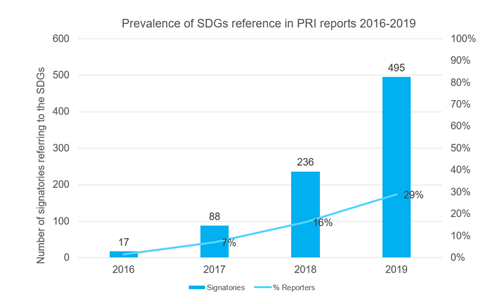

Climate action is also part of the Sustainable Development Goals (SDGs), another strategic focus area for the PRI. Back in 2016, just 17 investors mentioned the SDGs when reporting to the PRI on their RI processes. This is not surprising, since the SDGs were only adopted in September 2015. Fast forward three years, and the appetite to support and align with the SDGs is clear among PRI signatories; nearly 500 investors (27% of investors reporting) refer to the SDGs in their RI reports, specifically in the description of their policies, objectives and processes.

What advice do you have for those eager to use PRI data?

The first thing to point out is that comparing practices year on year is not always insightful. It can take time – sometimes up to two or three years – to implement new processes, especially in large organisations. So, where possible, we look at practices over a three-year period.

The second challenge we face is that our signatory base keeps growing; the amount of investors reporting grew by 60% since 2016, reaching 1,710 in 2019. As newer signatories tend to be in the early stages of their RI journey, the progress made by older signatories can be cancelled out when looking at the data as a whole. So, we also look at changes in practices for subsets of reporters in both years to get a better picture of different levels of progress.

What can signatories expect next on reporting?

Following feedback from 580 signatories, we will be busy implementing changes to the content and structure of the Reporting Framework for the 2021 reporting cycle. There will be minimal changes to the 2020 reporting cycle.

We will publish two snapshot reports based on 2019 data. The climate snapshot will come out in early September and will provide insights as to how signatories are implementing the TCFD recommendations. The second snapshot will showcase asset owner practices on manager selection, appointment and monitoring to accompany the first PRI leaders’ report, and will be out by December 2019.