In September 2015 the global community, represented by all 193 member states of the United Nations (UN), adopted the Sustainable Development Goals (SDGs). The 17 SDGs and 169 individual targets will guide the global community’s sustainable development priorities from now until 2030 and seek to “stimulate action […] in areas of critical importance for humanity and the planet”.

Countries, NGOs, companies and investors are all needed to help achieve the 17 SDGs and the 169 underlying targets. Never before has the global community set out such an ambitious agenda – and the need to meet the challenges is urgent: the UN Commission on Trade and Development (UNCTAD) estimates that meeting the SDGs will require US$5 trillion to US$7 trillion in investment each year from 2015 to 2030. In order to unlock this opportunity, it will be critical for investors to re-orient their investment flows towards the new innovative products and services focused on finding solutions to achieve the SDGs. In their recently published “taxonomy”, Dutch pension managers APG and PGGM have identified investment opportunities linked to 13 of the 17 SDGs and demonstrated areas they consider potential “sustainable development investments”, bridging the gap between the UN’s targets and tangible investment opportunities.

While government spending and development assistance will contribute, they are expected to make up no more than US$1 trillion per year, so new flows of private sector capital will be key, either through new allocations or by re-routing existing capital flows.

“At its essence, sustainability means ensuring prosperity and environmental protection without compromising the ability of future generations to meet their needs.”

Ban Ki-Moon, Secretary General, United Nations

The global SDGs are a clear call to action for the private sector. Some of the SDGs are easier to contribute to than others; sometimes public policy changes are needed and will be made to make certain SDGs more investable. Sometimes it is easier to address an SDG through investment decisions; sometimes it is easier to incorporate the SDG in active ownership. But either way, investors will be asked to contribute.

So why should investors care about the SDGs?

| FIDUCIARY DUTY The SDGs are an articulation of the world’s most pressing sustainability issues and as such act as the globally agreed sustainability framework. The SDGs can support investors in understanding the sustainability trends relevant to investment activity and their fiduciary duties. |

||

| RISKS | OPPORTUNITIES | |

|---|---|---|

| MACRO | By the nature of their investments, asset owners that choose to hold a diversified portfolio, investing in a wide range of asset classes and geographies, will be exposed to the global challenges that the SDGs represent. Failure to achieve the SDGs will impact all countries and sectors to some degree, and as such create macro financial risks. | Achieving the SDGs will be a key driver of global economic growth, which any long-term investor will acknowledge as the main ultimate structural source of financial return. |

| MICRO | The challenges put forward by the SDGs reflect that there are very specific regulatory, ethical and operational risks which can be financially material across industries, companies, regions and countries. | Companies globally moving towards more sustainable business practices, products and services provide new investment opportunities. |

Many PRI signatories believe that their investments in companies (and other entities) will only be profitable in the long term if societies and the financial system develop in an equitable and sustainable way.

Additionally, ultimate beneficiaries (participants in pension funds, clients of insurance companies, etc.) increasingly demand that all parties in the investment chain (markets, asset holders and managers) take their broader long-term interests, and those of future generations, into account.

The preamble to the Principles for Responsible Investment, signed by more than 1,750 signatories, states: “We recognise that applying these Principles may better align investors with broader objectives of society.” The SDGs act as welcome guidance as to what the “broader objectives of society” are, and should play an important role in the development of a responsible investment agenda for the years ahead. As the largest responsible investment initiative in the world, representing more than half of the world’s professionally managed assets4, the PRI is best positioned to help set that agenda. Our roadmap towards achieving these objectives is outlined in our Blueprint for responsible investment.

“We believe that an economically efficient, sustainable global financial system is a necessity for longterm value creation. Such a system will reward long-term, responsible investment and benefit the environment and society as a whole.”

PRI Mission

“Driving sustainable development in line with the UN SDGs will create a more prosperous world, to live in today and to pass on tomorrow.”

PRI Blueprint for responsible investment

Moving responsible investment from process and business conduct to real-world impact and contribution to the SDGs

Responsible investment is generally understood as a process to incorporate material ESG factors in investment policies, decisions and ownership, and improvement of business conduct. This raises the question to what extent responsible investment has already led to positive outcomes to society.

Responsible investment practices have gained enormous traction in the industry over recent years, which has already aligned investors, investments and active ownership, with the “broader objectives of society” to some extent. Positive outcomes can be realised through three mechanisms: integrating ESG factors in investment decisions, improving ESG performance through active ownership and allocating assets to thematic investments.

Evaluating contribution of current responsible investment practices to real-world impact

Effects of integration

- The assumption behind integrating ESG factors in investment policy and decisions is that it will ultimately affect the cost of capital, lowering the costs of capital for sustainable businesses and increasing the costs for non-sustainable businesses. As a result of the lower costs of capital, sustainable businesses will in the long run crowd out non-sustainable businesses. Meta-studies by Mercer and the University of Hamburg and Deutsche Asset & Wealth Management provide clear evidence that sustainable business practices lead to lower cost of capital and equal or even better financial performance, but despite higher costs of capital, companies with poor ESG management still have sufficient access to capital and companies providing unsustainable products and services may have relatively good ESG risk management (and vice versa). Conventions of finance still point towards practices that don’t reward sustainable businesses sufficiently to drive out unsustainable business.

Effects of active ownership

- Including ESG factors in engagement with investee companies is intended to highlight the materiality of ESG issues, convince businesses to adopt more sustainable products, services and processes and thus improve the risk-return profile of the businesses. Academic research has provided some insight into the positive impact of active ownership on corporate ESG practices and financial performance, but finds the contribution is often focused on process improvements and business conduct rather than real-world impact aligned with the SDGs.

Effects of thematic asset allocations

- One in six PRI signatories (17%) report allocating capital to environmentally/ socially themed investments (e.g. inclusive finance, renewable energy, clean technology, affordable housing). These investments, made under the assumption that they will provide market rate returns as well as positive outcomes to society, are seeing increasing inflows, but the approximately US$1.3 trillion invested in impact investments by PRI signatories is far from the approximately US$75 trillion to US$105 trillion that UNCTAD’s estimates suggest is required from the private sector overall over the life of the SDGs.

Undeniably, current responsible investment practices contribute to the “broader objectives of society”, but the contribution is limited and achieving the SDGs through corporate responsibility and responsible investment will require a more dedicated approach. To meet the challenges of the SDGs, responsible investment should not just look at how ESG risks and opportunities affect the risk-return profile of an investment portfolio, but also how a responsible investment portfolio affects those broader objectives of society.

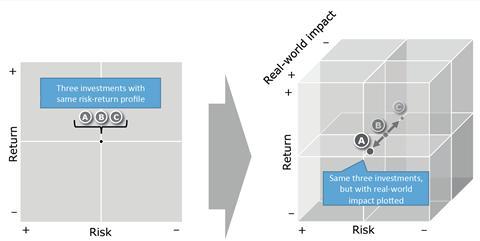

The PRI’s work on investment strategy is introducing a shift towards including a third dimension of “real-world impact” (aligned with the SDGs) alongside risk and return, describing how to embed real-world outcomes in the development of an investment strategy.

“The SDGs are the framework that institutional investors need in order to fulfil their purpose and full potential in the capital markets and society at large, and to be accountable to their beneficiaries.”

Vipul Arora, Co-Founder, Solaron

Produced in collaboration with PwC

![]()

Downloads

The SDG investment case

PDF, Size 2.83 mbEl enfoque de inversion en los ODS

PDF, Size 1.66 mbThe SDG Investment Case - CN

PDF, Size 3.55 mb

The SDG investment case

- 1

- 2

Currently reading

Currently readingInvestors and the Sustainable Development Goals

- 3

- 4

- 5

- 6

- 7