The level of global interest in plastic production, consumption and waste has soared in recent years. While much of this focus has been on the risks and impacts, it is important to recognise that the flexibility and resilience of plastic mean that products made from the material perform many crucial functions in society and across sectors.

The plastic value chain is complex, touching most (if not all) business sectors globally. Therefore, investor portfolios are exposed to an array of risks and opportunities associated with plastic.

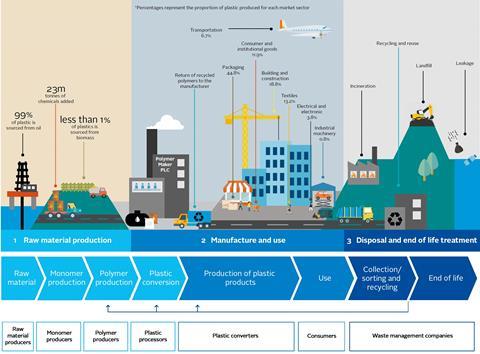

Overview of the global plastic supply chain

Key findings:

- Different sectors will experience near and long-term risks across the plastic value chain, driven by shifting demands for plastic, regulation, changes in supply of raw materials and alternative materials, and access to recycled materials. Starting with raw material production, the oil and gas sector is responsible for fossil-based production. Investors should consider the long-term risks (stranded assets) facing the sector in the future due to potential disruptions in demand for plastic packaging and the supply of alternative materials. On the production of bio-based feedstock, the agricultural products sector will find itself under closer scrutiny amid competing demands for food security and responsible sourcing requirements.

- Related to bio-based feedstock is the topic of bioplastics. There are many misconceptions about bioplastics as investors consider alternatives to conventional oil-based plastic. It is important to note that bio-based materials may or may not be biodegradable, and biodegradable materials that are used as alternatives to plastics may or may not be bio-based. A major challenge is that recycling is only suitable for non-biodegradable (fossil or bio-based) plastics, which is not always clearly signed.

- Global fossil fuel-based plastics production is dominated by large petrochemical companies, including some major oil and gas producers. However, some of these companies are becoming more integrated players in plastic production, providing waste processing solutions and supplying raw materials.

- The containers and packaging sector, as well as related sectors such as food and beverage and consumer goods, face reputational and regulatory pressures to use alternative materials and recycled content at scale. This is creating opportunities for companies to collaborate and find solutions with different players across the value chain.

- While waste management is part of the problem, it is also part of the solution. Less than 20 percent of plastic waste is currently recycled globally and demand for recycled content is outstripping supply. This will be amplified by regulatory disruption in the secondary commodities market.

References

- Ryberg, M. W., Laurent, A. and Hauschild, M., 2018. Mapping of global plastics value chain and plastics losses to the environment. [pdf] Nairobi: United Nations Environment Programme.

- Jambeck, J.R., Geyer, R., Wilcox, C., Siegler, T.R., Perryman, M., Andrady, A., Narayan, R. and Law, K.L., 2015. Plastic waste inputs from land into the ocean. Science, 347(6223), pp.768-771.

- World Bank, 2019. What a Waste Global Database.

- Geyer, R., Jambeck, J.R. and Law, K.L., 2017. Production, use, and fate of all plastics ever made. Science advances, 3(7), p.e1700782.

- Eurostat, 2019. Recycling rates for packaging waste.

- Ministry of Environment, Japan, 2018. Japan’s Resource Circulation Policy for Plastics.

- United States Environmental Protection Agency, 2019. Plastics: Material Specific Data.

- Iniciativa Regional para Reciclaje Inclusivo, 2018. Estudio comparativo de legislación y políticas públicas de Responsabilidad Extendida del Productor – REP para empaques y envases.

- Reloop, 2017. Reloop Releases Global Overview of Deposit Return Systems.

- Geyer, R., Jambeck, J.R. and Law, K.L., 2017. Production, use, and fate of all plastics ever made. Science advances, 3(7), p.e1700782.

- Plastics Europe, 2018. Plastics – the Facts 2018.

About The plastics landscape series

This is the second report in a series aimed at equipping investors with the information they need to understand plastic as a systemic issue, providing a technical overview of plastic and the plastic market, and exploring common concepts.

The series will help investors to identify where and how their portfolios might be exposed to plastic, enabling them to analyse relevant sectors and engage at the corporate and policy levels accordingly.

The first report looked at the challenges and solutions for the plastics system, and the third identifies regulations, policies and influencers of change in how plastic is managed.

Find out more about our work on plastics and the circular economy.

Downloads

Plastics landscape risks and opportunities on the value chain

PDF, Size 1.7 mb塑料:价值链上的风险和机遇

PDF, Size 2.43 mb