By Itay Goldstein, University of Pennsylvania; Alexandr Kopytov, University of Hong Kong; Lin Shen, INSEAD and Haotian Xiang, Peking University

The appetite for environmental, social and governance (ESG) investing has increased rapidly over recent years[1] but the implications for financial markets and asset pricing are far from clear.

Our paper studies how ESG investing affects asset price formation. We seek to understand the informational content of asset prices, and how they should be interpreted when ESG investors play a substantial role alongside traditional investors.

What normally drives asset prices?

Traditionally, an asset price is thought to be a simple yet powerful signal about the present value of future cash flows. However, this view relies on the assumption that all investors only value financial payoffs (e.g., dividends or coupon payments).

The presence of ESG investors that value both financial returns and the ESG performance of their portfolios challenges this view.

While heterogeneity in financial markets has always existed, this is different – as different investors are valuing an asset for different reasons.

Modelling different asset price drivers

We build a model in which investors trade a stock whose payoff consists of financial (for example, regular earnings) and ESG risky components (for example, carbon emissions).

The financial market is populated with two groups of investors that receive informative signals about both components but have distinct preferences about them. Traditional investors value only the financial payoff and green investors value both payoffs. Importantly, these green investors include individual investors that directly value ESG performance alongside ESG fund managers whose compensation and reputation hinge on their ability to identify ESG assets.

As such, asset prices are driven by both factors and may be informative about cash flows and ESG performance.

Since there is only one price to reflect two factors, trading for one factor naturally dilutes useful information contained in the price about the other. For example, the ESG component makes the price a noisier signal about regular cash flows to traditional investors, as they have a hard time understanding whether a high asset price is driven by high future cash flows or good future ESG performance.

The source of information in the price is the trading activity by the two groups: each group trades with information they have about the dimension they care about and against information they have about the other dimension. Upon receiving positive information about a firm’s ESG performance, green investors would increase their demand for the firm’s stock, driving up the price, while traditional investors would reduce their demand, depressing the price. Consequently, trades by traditional and green investors make the price noisier and contaminate the informativeness of the two factors.

Two pricing regimes

This can lead to two regimes in the pricing of a stock.

In the traditional regime, the stock price is mostly driven by the financial component and is informative to traditional investors. Green investors that care about ESG performance cannot learn much about it from the price and thus consider the stock risky. As a result, it is mostly traded by traditional investors that do not introduce the ESG information to the price.

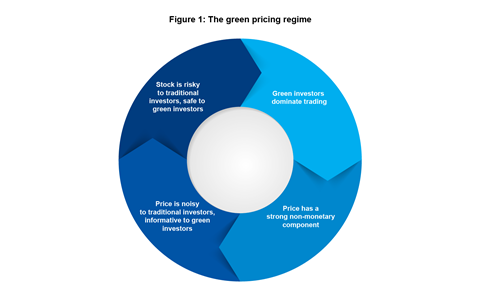

In the green regime, the opposite is true: green investors actively trade the stock, the price is strongly associated with ESG performance and is noisy to traditional investors that then perceive the stock as risky and do not actively trade it. Figure 1 illustrates how the green regime emerges out of this self-reinforcing loop. A similar process can operate to bring about the traditional regime.

We show that the green regime becomes possible when enough investors in a stock have ESG preferences. As green investors become more prevalent, stocks are increasingly likely to move from a traditional regime to a green regime, and their prices might reveal very different things than traditionally expected.

What are the cost of capital implications?

Our model reveals that the growth of investors that consider ESG factors in the financial market might cause a firm’s costs of capital to increase.

As asset prices start to react more to ESG information and less to cash-flow information, traditional investors see the price as noisier, and so for them stocks become riskier to trade. As a result, they require a higher expected return as compensation, which can increase the firm’s cost of capital.

Evidence on the link between expected returns and ESG performance has been mixed. Some papers find that green firms have a lower cost of capital (Hong & Kacperczyk, 2009; Bolton & Kacperczyk, 2021), while others document similar or even higher cost of capital for green firms (Derwall, Guenster, Bauer, & Koedijk, 2005; Avramov, Cheng, Lioui, & Tarelli, 2021).

Existing theories suggest that firms with good ESG performance tend to enjoy a lower cost of capital because green investors are willing to pay a premium for their greenness.

Our paper reflects this, but we also point out a new channel. Green investors tend to divest traditional firms and invest in green firms; therefore, their stock prices are likely to reflect more ESG information while being less informative about cash flows. This makes green stocks riskier to trade for traditional investors and can increase green firms’ cost of capital.

What are the implications for ESG disclosure?

Despite the growing interest in ESG investing, there is a lack of clarity and consistency in the definition and measurement of firms’ ESG performance. To address this, policy makers have tried to improve the quality of ESG information available to investors.

For example, in May 2020 the SEC Investor Advisory Committee recommended updating public company reporting requirements to include ESG factors, while the EU regulator has put in place a disclosure regulation that requires market participants and financial advisers to provide ESG-related information about certain financial products (Regulation EU 2019/2088).[2]

While such advances intend to help investors make informed decisions, our model highlights some unintended consequences.

A basic effect is that better ESG information benefits all investors by providing them with more precise information and helping them interpret prices more clearly.

However, green investors that value the ESG payoff directly benefit disproportionally more from better ESG information. Following an improvement in ESG information, they start to face less risk and so they trade the stock more aggressively. This introduces even more ESG information to the price and makes it less informative about cash flows to traditional investors.

Takeaway

Many investors in modern financial markets care about the ESG performance of their portfolios. Their growing appetite has spurred the asset management industry into launching numerous ESG funds.

The presence of ESG investors and ESG funds reshapes price formation and changes the information content of asset prices. Given that interest in ESG factors is likely to continue, it is crucial for practitioners and regulators to update their views on how asset prices should be interpreted.

Our paper shows that prices might fall into different regimes – green or traditional – and that ESG appetite might have some undesirable effects on the quality of information in the market and firms’ cost of capital.

This paper was presented at the PRI Academic Network Week 2021. Please access the recording here.

This blog is written by academic guest contributors. Our goal is to contribute to the broader debate around topical issues and to help showcase research in support of our signatories and the wider community.

Please note that although you can expect to find some posts here that broadly accord with the PRI’s official views, the blog authors write in their individual capacity and there is no “house view”. Nor do the views and opinions expressed on this blog constitute financial or other professional advice.

If you have any questions, please contact us at [email protected]

References

[1] According to the Global Sustainable Investment Alliance, about US$17.1 trillion of assets in the United States were invested considering ESG factors in 2020, a significant increase from US$6.6 trillion in 2014.

[2]According to Carrots & Sticks, there are more than 600 ESG reporting requirements across over 80 countries, including the world’s 60 largest economies (Carrots & Sticks, 2020).

Avramov, D., Cheng, S., Lioui, A., & Tarelli, A. (2021). Sustainable Investing with ESG Rating Uncertainty. Journal of Financial Economics.

Bolton, P., & Kacperczyk, M. (2021). Do Investors Care about Carbon Risk? Journal of Financial Economics, 517-549.

Carrots & Sticks. (2020). Sustainability Reporting Policy: Global Trends in Disclosure as the ESG