By Irene Monasterolo, Assistant Professor of Climate Economics and Finance, Vienna University of Economics and Business

Climate change represents a new source of risk for finance, thus challenging traditional stress-testing approaches. We present a consolidated climate stress-test methodology, which introduces climate uncertainty and complexity in financial risk valuation, and its policy application in collaboration with leading financial institutions.

Climate risks and financial stability: insights from climate stress-testing

Since former Bank of England governor Mark Carney’s landmark speech in 2015, central banks and financial regulators have increasingly recognised the potential impacts of climate risk, and of a disorderly transition to a low-carbon economy (usually referred to as climate transition risk), on individual and systemic financial stability.

In this regard, a group of central banks and financial regulators created the Network for Greening the Financial System (NGFS), aiming to support investors’ climate-related financial risk disclosures and highlighting the importance of running climate stress-tests (NGSF 2019).

While these recent concerns come from the community of financial supervisors, they are aligned with a stream of academic research that has developed since 2017 around a seminal work on financial system climate stress-testing (Battiston et al. 2017).

This has created a conceptual and analytical framework through which to test those concerns, by quantitatively assessing forward-looking climate risks in individual investors’ portfolios. The framework embeds future climate and economic trajectories, developed by the Integrated Assessment Models (IAM) (Kriegler et al. 2013) and reviewed in the Intergovernmental Panel on Climate Change (IPCC) reports, in traditional financial risk metrics and methods used by academics and practitioners, such as the Value at Risk (VaR) and stress-testing.

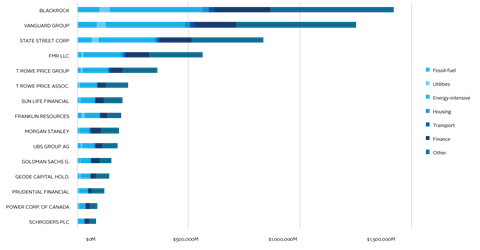

Battiston et al. (2017) found that individual financial actors have large direct and indirect exposures to the Climate Policy Relevant Sectors (CPRS) – economic activities that would lose value and become stranded assets in a disorderly low-carbon transition.

These exposures amount to more than 40% for the equity portfolios of pension funds and investment funds (Figure one).

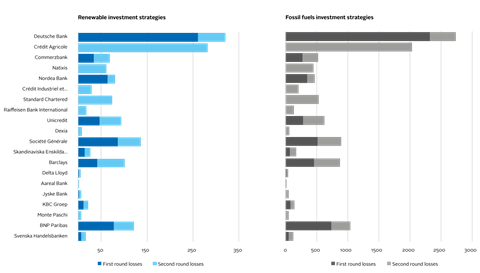

By introducing Climate VAR when considering micro-level climate transition risks, such as the exposures of financial institutions to individual financial contracts, they find that banks with a “brown” strategy incur large losses (Figure two).

These could be amplified by financial interconnectedness, with implications on asset price volatility and financial stability (Monasterolo et al. 2017).

The methodology has now been incorporated into the CLIMAFIN tool to price climate-related financial risks under deep uncertainty (Battiston et al. 2019a).

Challenges for conducting climate stress-tests

Stress-testing exercises are widely used by central banks and financial regulators to assess the resilience of the financial sector to shocks. However, the characteristics of climate change differ significantly from those considered in traditional stress-testing exercises, making the latter inadequate in the context of climate risks.

Climate change risk is forward-looking and characterised by deep uncertainty and tail events (Weitzman 2009), tipping points (Solomon et al. 2009, Lenton et al. 2019) and non-linearity (Ackerman 2017), leading to potential domino effects (Steffen et al. 2018). Most important, climate risk is endogenous, because the realisation of climate scenarios depends on policy-making decisions and investors’ decisions (e.g. on portfolio decarbonisation), based on their beliefs (Battiston and Monasterolo 2019). This confronts us with the need to consider multiple scenarios and equilibria with unknown probabilities, i.e. a condition for decision-making under uncertainty.

In contrast, the macroeconomic and macro-econometric models used for stress-testing by central banks are characterised by market clearing prices, linear shock transmissions, representative and intertemporal optimising agents, and an aggregate representation of the technologies that are relevant for the transition, e.g. energy. In addition, standard financial risk valuation relies on average values, historical market information and backward-looking benchmarks (Battiston and Monasterolo 2019).

Using the right models is crucial to correctly informing risk management strategies and prudential regulations, and to avoid underestimating or miscalculating risks that could trigger financial instability. This also helps us to understand how finance can be a driver or a barrier to achieving climate targets.

From theory to practice: a five-step approach to climate stress-testing

In CLIMAFIN’s Climate Stress-Test, we consider shocks caused by a disorderly transition from a business-as-usual scenario (BAU) to a scenario characterised by the introduction of a climate policy, such as a carbon tax (P) that allows us to achieve the Paris Agreement 2°C target. From this we developed a five-step approach (Battiston et al. 2017):

1. Identify the financial contracts that are exposed to climate transition risks based on the issuer’s sector as well at the technological profile of their business lines (e.g. for utility companies the share of electricity from fossil versus renewable sources).

2. Identify a set of Climate Policy Shock Scenarios based on energy transition scenarios (e.g. provided by the IPCC (2018), by the NGFS (2019) and Bolton et al. (2020)). Develop a consolidated database of economic scenarios (derived from IAM and other established climate economic models) to derive estimates of shocks in sector-wide economic output (e.g. low-carbon versus carbon-intensive) and countries. Shocks are computed as a relative difference in sectors’ output between the two trajectories (BAU and P). The disorderly transition can be understood as a temporary out-of-equilibrium economic shift (i.e. a jump) between two separate equilibrium trajectories.

3. Compute the adjustment on the Probability of Default (PD) conditioned to the Climate Policy Shock on firms and individual financial contracts (e.g. equity holdings, corporate and sovereign bonds, loans). Compute the climate spread for individual sovereign and corporate bonds, i.e. the adjustment in the bond spread conditional to a given Climate Policy Shock Scenario.

4. Compute the adjustment on key financial risk metrics for gains and losses at the level of investors’ portfolios e.g. the Climate VaR, which represents the worst-case loss, for a chosen confidence level, conditional to a Climate Policy Shock Scenario.

5. By applying financial network models that account for risk reverberation driven by financial interconnectedness (Battiston et al. 2012, Roncoroni et al. 2019), run a climate stress-test to assess the potential losses for the financial sector and the implications on systemic financial risk.

This framework reconciles the deep uncertainty of climate transition risk and its interplay with financial risk into the existing stress-test exercises used by financial supervisors.

Policy applications and recommendations

The climate stress-test approach proposed here has been further developed and applied to several policy exercises in collaboration with central banks and financial regulators:

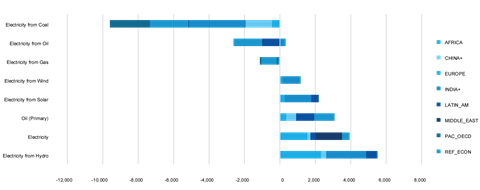

- In 2018, Monasterolo et al. used the CLIMAFIN methodology to assess the carbon risk exposure of overseas energy infrastructure portfolios from the China Development Bank and Export-Import Bank of China (totalling 199 loans worth just over US$228 billion). They found that the banks’ exposures to losses induced by climate transition risk ranged between 4% and 22% of their portfolios.” In particular, under a stringent 2C-aligned climate policy scenario (i.e. StrPol 450) characterised by the introduction of a carbon tax and countries’ fragmented action, negative shocks on project loans’ value affect in particular coal power generation in the Chinese and bordering countries’ region (i.e. CHINA+), and oil and gas power generation in former ex-USSR and transition countries (i.e. the Reforming Economies). In contrast, positive shocks are associated to renewable energy projects, in particular in hydropower in the African region and nuclear in Pakistan. The scenarios and shocks are computed using the GCAM Integrated Assessment Model and the LIMITS database, while the shocks are in USD billion (Figure three).

- In 2019, Battiston and Monasterolo priced forward-looking climate transition scenarios and economic trajectories in the PD and value of sovereign bonds, introducing the climate spread metrics, and applied it to the non-monetary policy portfolio of the Austrian National Bank (OeNB), focusing on OECD countries. They found that countries where low-carbon sectors play a large economic role have lower bond yields and climate spread relative to countries where fossil fuels still play a large (direct or indirect) role (Figure four).

Figure four: Climate policy shock (tight policy scenario) computed with GCAM and WITCH on OECD’s sovereign bonds value and climate spread. Notice that positive shocks on the yield correspond to negative shocks on the value of the sovereign bond. Climate spread: 2,45=245 basis points. Source: Battiston and Monasterolo (2019)

| Geo region | Model region | WITCH: bond shock (%) | WITCH: yield shock (%) | GCAM: bond shock (%) | GCAM: yield shock (%) |

|---|---|---|---|---|---|

| AUSTRIA | EUROPE | 1.3 | -0.16 | 0.13 | -0.02 |

| AUSTRALIA | REST_WORLD | -17.36 | 2.45 | n.a. | n.a. |

| BELGIUM | EUROPE | 0.84 | -0.1 | 0.03 | 0 |

| CANADA | PAC_OECD | -5.21 | 0.67 | -18.29 | 2.61 |

| POLAND | EUROPE | -12.85 | 1.75 | -2.49 | 0.32 |

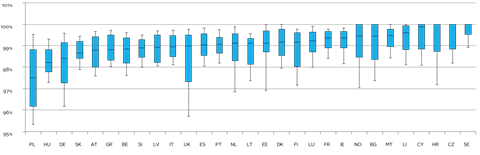

- In 2019, in the first collaboration between climate economists, climate financial risk modelers and financial regulators (the European Insurance and Occupational Pension Fund Authority), Battiston et al. (2019b) used the CLIMAFIN framework to assess the climate transition risk of European single insurers’ sovereign bond portfolios. They found that the potential impact of a disorderly transition is non-negligible in several scenarios (Figure five). Given the importance of sovereign bonds in insurance portfolios, this risk deserves to be regularly monitored.

The climate stress-test presented here allows future climate risks to be incorporated in the assessment of firms’ or countries’ financial solvency. As such, it can inform investors’ risk management strategies and financial regulators’ policies to allow for a smooth transition and preserve financial stability. However, the complexity and novelty of the analysis requires the relevant climate shock scenarios and financial risk metrics and methods to be identified by financial supervisors together with the scientific community, to ensure the exercise is credible and relevant.

This blog is written by academic guest contributors. Our goal is to contribute to the broader debate around topical issues and to help showcase research in support of our signatories and the wider community.

Please note that although you can expect to find some posts here that broadly accord with the PRI’s official views, the blog authors write in their individual capacity and there is no “house view”. Nor do the views and opinions expressed on this blog constitute financial or other professional advice.

If you have any questions, please contact us at [email protected].

References

Ackerman, F. (2017). Worst-Case Economics: Extreme Events in Climate and Finance. Anthem Press.

Battiston, S., Puliga, M., Kaushik, R., Tasca, P. and Caldarelli, G. (2012). Debtrank: Too central to fail? financial networks, the fed and systemic risk. Scientific reports, 2, 541.

Battiston S., Mandel A., Monasterolo, I., Schütze, F. and Visentin G. (2017). A climate stress-test of the financial system, Nature Climate Change 7 (4), S. 283.

Battiston S. and Monasterolo I. (2019). A climate risk assessment of sovereign bond portfolios. Working paper in collaboration with OeNB, available at SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3376218

Battiston, S., Mandel, A. and Monasterolo, I. (2019a). CLIMAFIN Handbook: Pricing Forward-Looking Climate Risks Under Uncertainty. Available at SSRN: 3476586.

Battiston, S., Jakubik, P., Monasterolo, I., Riahi, K. and van Ruijven, B. (2019b). Climate risk assessment of sovereign bonds’ portfolio of European insurers. In: European Insurance and Occupational Pension Authority (EIOPA) Financial Stability Report, December 2019.

Battiston, S. (2019). The importance of being forward-looking: managing financial stability in the face of climate risk. Financial Stability Review Banque de France, June.

Bolton, P., Despres -Luiz, M., Pereira, A., Silva, D. A., Samama, F., and Svartzman, R. (2020). The green swan - central banking and financial stability in the age of climate change. Retrieved from www.bis.org

Carney, M. (2015). Breaking the Tragedy of the Horizon: climate change and financial stability. Speech given at Lloyd’s of London by the Governor of the Bank of England, 29.

Kriegler, E., Tavoni, M., Aboumahboub, T., Luderer, G., Calvin, K., DeMaere, G., Krey, V., Riahi, K., R¨osler, H., Schaeffer, M. and Others (2013). What does the 2 C target imply for a global climate agreement in 2020? The LIMITS study on Durban Platform scenarios. Climate Change Economics, Vol. 4(04) Special issue on implementing climate policies in the major economies: an assessment of Durban Platform achitectures- results from the LIMITS project , pp.1-30.

Intergovernmental Panel on Climate Change (IPCC) (2018). Global warming of 1.5 C. An IPCC Special Report on the impacts of global warming.

Lenton, T. M., Rockström, J., Gaffney, O., Rahmstorf, S., Richardson, K., Steffen, W., and Schellnhuber, H. J. (2019). Climate tipping points — too risky to bet against. Nature. Nature Research. https://doi.org/10.1038/d41586-019-03595-0

Monasterolo I., Battiston S., Janetos A. C. and Zheng Z. (2017). Vulnerable yet relevant: the two dimensions of climate-related financial disclosure. Climatic Change, 145(3–4), 495–507.

Monasterolo I., Zengh J.I. and Battiston S. (2018). Climate-finance and climate transition risk: an assessment of China’s overseas energy investments portfolio. China & World Economy, 26 (6), 116-142

Network for Greening the Financial System (2019). A call for action Climate change as a source of financial risk. First comprehensive report.

Roncoroni A., Battiston S., Escobar Farfan, L. O. and Martinez-Jaramillo S. (2019). Climate risk and financial stability in the network of banks and investment funds. Available at SSRN https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3356459

Solomon, S., Plattner, G. K., Knutti, R., and Friedlingstein, P. (2009). Irreversible climate change due to carbon dioxide emissions. Proceedings of the National Academy of Sciences of the United States of America, 106(6), 1704–1709. https://doi.org/10.1073/pnas.0812721106

Steffen, W., Rockström, J., Richardson, K., Lenton, T. M., Folke, C., Liverman, D., … Schellnhuber, H. J. (2018). Trajectories of the Earth System in the Anthropocene. Proceedings of the National Academy of Sciences of the United States of America. National Academy of Sciences. https://doi.org/10.1073/pnas.1810141115

Weitzman, M. L. (2009). On Modeling and interpreting the economics of catastrophic climate change. The Review of Economics and Statistics, XCI (1).