By Rajna Gibson Brandon (University of Geneva), Simon Glossner (University of Virginia – Darden School of Business), Philipp Krueger (University of Geneva & Swiss Finance Institute), Pedro Matos (University of Virginia – Darden School of Business) and Tom Steffen (Osmosis Investment Management)

The practice of responsible investing, whereby institutional investors incorporate environmental, social, and governance (ESG) issues into their investment processes, is no longer a fringe phenomenon. Nothing illustrates this better than the tremendous growth of the Principles for Responsible Investment (PRI) network. Our research shows that PRI signatories now manage half of the public equity assets held by institutional investors globally. Despite the increasing importance of PRI signatories in financial markets, there is only limited academic evidence on the portfolio consequences of signing up to the PRI’s Principles.

In our paper, Responsible Institutional Investing Around the World, we examine whether PRI signatories walk their (ESG) talk. Our research is the first to use the data from PRI Reporting & Assessment Framework, which PRI signatories use to report on their responsible investment activities annually. We match the signatories’ publicly available reporting data with archival data on institutional investors’ global equity portfolio holdings. To measure how serious PRI signatories are about taking ESG issues into account, we calculate a value-weighted ESG score for each institutional investor’s stock portfolio based on ESG scores from three prominent data providers (Refinitiv, MSCI, and Sustainalytics). We call these investor portfolio scores ESG footprints.

Do PRI signatories walk the (ESG) talk and have better ESG portfolio footprints?

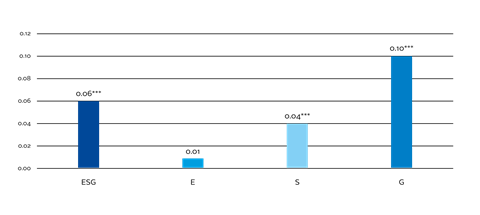

We start our analysis by showing that institutions seem to join the PRI for reasons that are related to societal values as well as commercial benefits (higher investor flows). More importantly, we find that institutions that joined the PRI exhibited significantly better ESG footprints on average than those who did not (6% of a standard deviation increase in ESG scores), as highlighted in Figure 1, which captures the difference in the total ESG footprint between PRI signatories and non-signatories.

The differences between PRI and non-PRI investors’ portfolio footprints can mainly be found in the social and governance dimensions: surprisingly, there is no evidence that PRI investors have statistically significantly better environmental footprints than non-PRI investors. We also examine whether PRI signatories change their behaviour as a result of committing to the Principles and show that institutional investors generally improve their portfolio ESG footprints after signing up, relative to non-signatories.

One of the drivers of improvement is the staggered adoption of country-level investor stewardship codes, which set out how investors should incorporate ESG factors into their investments through stewardship activities. In fact, after a stewardship code is introduced in a country, institutions domiciled there are more likely to become PRI members.

Figure 1: Difference in portfolio ESG footprints between PRI and non-PRI signatories

Are there regional differences among PRI signatories?

The pressure on institutional investors to integrate ESG issues into their decision making is likely to vary around the world. Environmental and social norms are relatively stronger in Europe, where responsible investing has been more broadly practiced. In contrast, the motivation to account for ESG factors might be more commercially driven (e.g. to attract investor flows) in other geographies.

There are also important differences in the regulatory requirements across jurisdictions. For example, in the United States, there is an open debate over whether fiduciary duties should include the consideration of ESG factors.

The analysis in Figure 1 masks the possibility of such regional differences among PRI signatories. Exploring potential cross-country differences, we find that PRI signatories located outside the United States have better portfolio-level ESG footprints than non-PRI investors in all three ESG dimensions.

Strikingly, however, the ESG footprints of US-based PRI signatories tend to be no better than the footprints of non-PRI US investors. We also find no evidence that US investors improve their portfolio-level ESG footprints after joining the PRI, despite them being the largest group of new signatories in recent years. Overall, we conclude that there is evidence that PRI signatories walk the (ESG) talk, except in the US, where our findings suggest that greenwashing might be an issue.

Do PRI signatories’ ESG footprints differ according to the extent to which they embrace ESG issues?

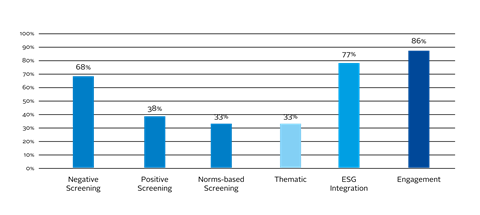

The rich data from the PRI Reporting Framework provides unprecedented detail of how institutions implement responsible investment. The data distinguishes between the main ESG implementation strategies – such as screening, ESG integration or the use of thematic investments – and stewardship activities, such as shareholder engagement.

In addition, the Reporting Framework provides information on the percentage of equity AUM to which a signatory applies a given ESG implementation approach. The data indicates that signatories most commonly manage ESG issues through engagement, integration, and negative screening (see Figure 2). The only strategy that remains niche is thematic investing.

Figure 2: Percentage of PRI signatories that use ESG strategies

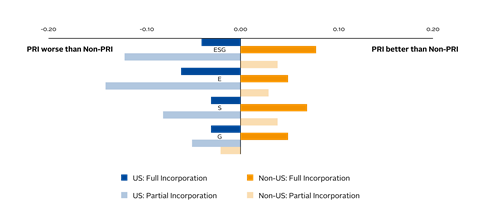

Our analysis then uses the data from the PRI Reporting Framework to study differences between signatories that have fully incorporated ESG considerations into their decision making from those that only do so partially. We classify PRI signatories who apply ESG strategies to only a fraction of their equity AUM (less than 100%) as partially incorporating them. We find that US-based PRI signatories that partially incorporate ESG strategies exhibit significantly worse ESG footprints than non-PRI institutions (see Figure 3).

This raises the interesting question as to why these US institutions still sign up to the PRI even though they do not live up to the commitments this implies. We find that these US investment managers typically only serve a retail clientele (rather than institutional clients who monitor their investment managers more closely) and have ESG problems in their own fund management companies.

Studying investment product-level data, such as mutual funds and separately managed accounts, we further document that US institutions that commit to the PRI experience higher investor flows on all their products (including non-ESG labelled ones). Taken together, these findings suggest that partially committed US-based PRI signatories undertake greenwashing to benefit from the increased interest in ESG investing.

Figure 3: Difference in portfolio ESG scores by PRI signatories depending on full vs. partial ESG incorporation

Do PRI signatories exhibit different holdings-based returns?

Finally, we examine whether there are trade-offs between responsible investing and risk-adjusted investment performance. We compare the yearly buy-and-hold equity portfolio returns of non-PRI investors and PRI signatories based on their level of ESG incorporation. We find that a portfolio’s ESG footprint is negatively correlated with portfolio risk but is not associated with higher average returns or alphas.

Taking a deeper look at specific ESG investment strategies, we document that negative screening, engagement, and integration are associated with significantly lower portfolio risk. We conclude that responsible investing is used as a risk-management tool. Given that we find no evidence that ESG strategies lead to better risk-adjusted returns, our study does not support the doing well by doing good mantra claimed by many industry practitioners.

Takeaways

Overall, our paper documents that there is a disconnect between the commitment of some US-domiciled PRI signatories and their effective ESG portfolio integration. By contrast, in countries other than the US, signatories tend to walk the talk and have better ESG footprints than non-PRI signatories. If signatories walk the talk, they tend to have not only a more sustainable portfolio, but also lower portfolio risks (albeit no better average returns or alpha).

Our findings call for more scrutiny on whether and how institutional investors implement their ESG commitments. The ultimate goal of the PRI – to promote a sustainable global financial system that rewards long-term, sustainable investment and benefits the environment and society – can only be achieved if investors live up to their ESG commitments.

Importantly, our results also highlight that asset owners need to look beyond PRI signatory status when evaluating external investment managers on how effectively they implement responsible investing.

This blog is written by academic guest contributors. Our goal is to contribute to the broader debate around topical issues and to help showcase research in support of our signatories and the wider community.

Please note that although you can expect to find some posts here that broadly accord with the PRI’s official views, the blog authors write in their individual capacity and there is no “house view”. Nor do the views and opinions expressed on this blog constitute financial or other professional advice.

If you have any questions, please contact us at [email protected]