Emirhan Ilhan, Frankfurt School of Finance & Management; Philipp Krueger, University of Geneva and Swiss Finance Institute; Zacharias Sautner, Frankfurt School of Finance & Management; and Laura T. Starks, University of Texas at Austin

Financial market efficiency relies on timely and accurate information regarding firms’ risk exposures. An increasingly important risk exposure relates to climate change. Climate risks can originate from more severe and more frequent natural disasters, government regulation to combat a rise in temperature, or climate-related innovations that disrupt existing business models (Litterman 2016; Krueger, Sautner, and Starks 2019). Consequently, high-quality information on firms’ climate risk exposures is necessary for making informed investment decisions and efficient pricing of the risks and opportunities related to climate change.

While many regulators and investors acknowledge the fact that firms’ climate risk exposures are important, they also believe current climate risk disclosure practices are insufficient. For example, Mark Carney, Governor of the Bank of England, called for more to be done “to develop consistent, comparable, reliable, and clear disclosure around the carbon intensity of different assets” (Carney 2015). In a similar spirit, Yngve Slyngstad, CEO of Norges Bank Investment Management, commented on the difficulty of obtaining climate risk-related data by saying that “the only surprise […] is how hard it is to get the data […] I think it will take years to get good data from the majority of companies we are invested in.” (Reuters 2018)

On a more positive note, there have been attempts by regulators, governments, and NGOs to address the shortcomings in current climate risk disclosures. For instance, in 2015, the Financial Stability Board initiated the Task Force on Climate-related Financial Disclosures (TCFD), with the objective of developing voluntary climate-related financial risk disclosures. On behalf of investors representing over US$87 trillion in assets under management, CDP collects climate-related information through a questionnaire. In addition to these initiatives, some countries have started to mandate climate-related disclosures. For instance, since 2013 the U.K. has required quoted companies to disclose their carbon emissions (Krueger 2015; Jouvenot and Krueger 2019), a requirement that has been extended to include unquoted companies from 2019 onwards. Since 2016, France requires institutional investors to report the carbon footprints of their investment portfolios.

While these initiatives suggest that investors increasingly demand climate-related information for their decision making, little systematic evidence exists on how institutional investors think about such disclosures. To fill this gap in knowledge, we surveyed institutional investors about their views and preferences with respect to climate-related disclosures.

The importance of climate risk reporting

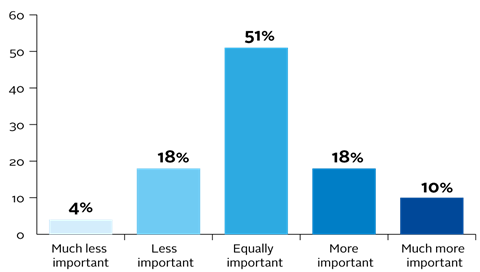

We found that the survey respondents share a strong general belief that climate disclosure is important. As Figure 1 illustrates, 51% of respondents believe that climate risk reporting is as important as traditional financial reporting, and almost one-third considers it to be more important. Only 22% of respondents regard climate reporting as less (or much less) important than financial reporting.

The risks climate change poses on firms are frequently divided in three distinct categories: physical risks, technological/transition risks, and regulatory risks. In terms of their relative importance, concerns about physical climate risks matter the most for the perceived importance of climate reporting, while regulatory risks matter the least. The emphasis on physical risks may be because such risks tend to be more firm and location specific, requiring relatively precise information about a firm’s exposure to evaluate them. The investors would then have lesser ability to gather the information and greater need for firm disclosure. In contrast, regulations tend to apply the same way to all firms in a given industry and often even in a country.

Investors’ views on current disclosure practices

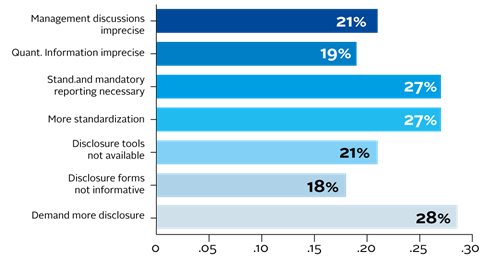

In order to better understand investors’ views on the informativeness of climate risk disclosures, we asked the investors a series of questions on how they perceive current qualitative and quantitative disclosure practices. Figure 2 shows the responses to these questions. The figure displays the percentage of investors who “strongly agree” with the given statement on the current disclosure practice.

The responses demonstrate a widespread perception that current quantitative and qualitative disclosures are imprecise and insufficiently informative. These responses imply that the current voluntary reporting regime does not fully enable informed investment decisions by investors, at least for firms with large exposures to climate risks. This could be one reason why climate risks are considered difficult to price in equity markets, an issue we next address in more detail.

Investors’ views on climate risk mispricing

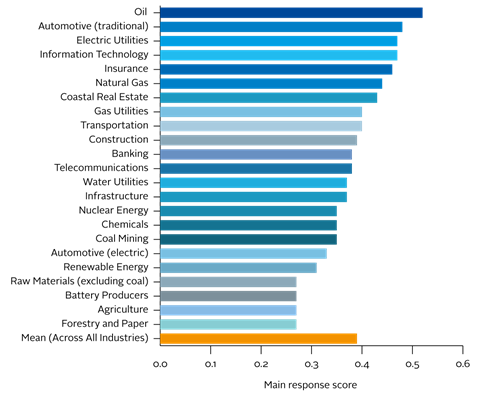

We first asked the investors how much mispricing they see in different sectors of the economy. The responses could range between “valuations are much too low” (coded with a score of -2) and “valuations are much too high” (coded as +2). We specifically asked about misvaluations related to climate risks and opportunities. Figure 3 shows that the respondents generally believe that current equity valuations are too high across all sectors of the economy, as reflected in the positive average response scores. Overvaluations are perceived as strongest in the oil, traditional automotive, electric utilities, and insurance sectors.

We then studied whether the investors’ opinions on the availability and quality of current climate reporting are related to the perceived underpricing of climate risks in equity markets (i.e., climate-related overvaluation of firms). We found that respondents who believe that current reporting is lacking also perceive more mispricing in current equity valuations. An important consequence of this finding is that better disclosure may contribute to a more efficient pricing of climate risks. In fact, this implication is consistent with a view expressed by Michael R. Bloomberg, Chair of the TCFD, who stated that “increasing transparency makes markets more efficient, and economies more stable and resilient.”

Conclusion

Our analysis indicates that investors find climate risk reporting highly important for their investment decisions. However, current disclosure practices are seen as insufficient, both in terms of quality and quantity. Likely as a result of this, many investors perceive that equity valuations do not fully reflect the risks related to climate change. More and better reporting on climate risks may be helpful in improving the correct pricing of climate risks and may, as a result, preserve financial stability.

This blog is written by academic guest contributors. Our goal is to contribute to the broader debate around topical issues and to help showcase research in support of our signatories and the wider community.

Please note that although you can expect to find some posts here that broadly accord with the PRI’s official views, the blog authors write in their individual capacity and there is no “house view”. Nor do the views and opinions expressed on this blog constitute financial or other professional advice.

If you have any questions, please contact us at [email protected].

References

The research paper underlying this article is available here

Carney, Mark, 2015, Breaking the tragedy of the horizon-climate change and financial stability, Speech 29 September, Bank of England, Lloyds of London.

Christensen, Hans B., Luzi Hail, L., and Christian Leuz, 2019, Economic analysis of widespread adoption of CSR and sustainability reporting standards, Working Paper, Chicago Booth School of Business.

Jouvenot, Valentin and Philipp Krueger, 2019, Reduction in corporate greenhouse gas emissions under prescriptive disclosure requirements, Working Paper, University of Geneva.

Krueger, Philipp, 2015, Climate change and firm valuation: Evidence from a quasi-natural experiment, Working Paper, Swiss Finance Institute.

Krueger, Philipp, Zacharias Sautner, and Laura T. Starks, 2019, The importance of climate risks for institutional investors, Review of Financial Studies, forthcoming.

Litterman, Bob, 2016, Climate Risk: Tail Risk and the Price of Carbon Emissions—Answers to the Risk Management Puzzle. Hoboken, NJ: John Wiley & Sons.

Matsumura, Ella M., Rachna Prakash, and Sandra C. Vera-Munoz, 2014, Firm-value effects of carbon emissions and carbon disclosures, TheAccounting Review 89, 695-724.

Plumlee, Marlene, Darrell Brown, Rachel M. Hayes, and R. Scott Marshall, 2015, Voluntary environmental disclosure quality and firm value: Further evidence, Journal of Accounting and Public Policy 34, 336-361.

Reuters, 2018, Norway wealth fund builds tool to analyse climate risk to portfolio, available at https://reut.rs/2CREuIs

Verrecchia, Robert E., Essays on disclosure, Journal of Accounting and Economics 32, 97-180.