By Tao Li, The University of Florida; Lakshmi Naaraayanan, London Business School; Kunal Sachdeva, Rice University

Sustainable funds – those focused on environmental, social, and governance (ESG) issues, have enjoyed record inflows in recent years, pushing their assets under management to nearly US$2.5 trillion by June 2022, according to research firm Morningstar.

This heightened interest in responsible investing has underlined the role that investment managers play in addressing corporate sustainability issues – including through their voting decisions.

At the same time, there is a growing concern among academics and policy makers that ESG funds may deviate from their investment objectives.[1] The focus so far, however, has been on assessing whether investment managers fulfil their ESG objectives via portfolio selection and evidence is lacking on what incentives drive their voting on shareholder proposals.

In our research paper, we study whether ESG funds trade the long-term sustainability of portfolio companies for greater short-term financial performance, focusing on how these funds vote on ESG proposals at shareholder meetings.

Voting behaviour of ESG funds

In principle, ESG funds care about environmental and social (E&S) issues and shareholder value, and their voting decisions must balance these.

On the one hand, investment managers market these funds as vehicles through which investors can delegate their pro-sustainability preferences. On the other, their fiduciary duty requires them to vote in their investors’ best interests to maximise wealth.

This may lead to funds seeking higher short-term benefits to attract investor flows. Given these conflicting objectives, it begs the question of whether financial incentives drive ESG funds’ voting decisions on E&S issues at shareholder meetings and whether fund investors internalise any costs associated with such actions.

We examine proxy voting by ESG funds, relative to non-ESG funds within the same fund family, on E&S proposals. We deem a fund to be an ESG fund if its name includes keywords such as ESG, SRI, CSR, environment, or social, among others.

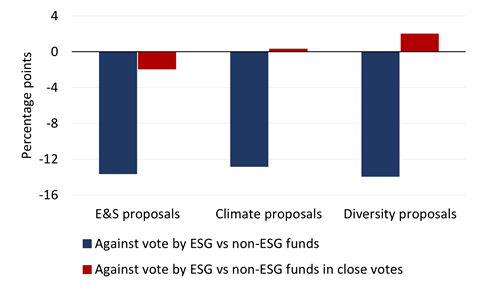

As shown in the figure below, ESG funds are 13.6 percentage points less likely than non-ESG funds to vote against an E&S proposal after controlling for proposal quality.

This is perhaps not surprising given most E&S proposals have failed to garner majority support (the average opposition rate from mutual funds is 63%), leading ESG funds to walk the talk by lending support to the average E&S proposal.

Figure 1: Opposition to E&S proposals by ESG vs non-ESG funds

The difference between ESG and non-ESG funds shrinks to only 1.9 percentage points for close votes – proposals with a winning margin between -10 and +10 percentage points.

These results suggest that ESG funds exaggerate the fulfilment of their sustainability mandate by voting for a proposal unlikely to prevail; however, they become pickier when a proposal vote may be pivotal, as advancing E&S initiatives at portfolio companies may come at the expense of lower financial returns.

Incentives to vote against E&S proposals

A natural question is whether E&S proposals are costly to implement, reducing funds’ incentives to support these proposals and driving the observed voting patterns.

To this end, we focus on close votes involving E&S proposals and measure abnormal stock returns (relative to benchmark returns) of the companies involved on meeting dates. This serves as a proxy for valuation effects associated with the unexpected success or failure of such proposals. Our evidence suggests that on average, E&S proposals that narrowly pass result in lower returns than E&S proposals that narrowly fail.

This indicates that the average investor expects the marginal E&S shareholder proposals to be costly for companies to implement. This is consistent with academic literature on the topic, which finds that improving E&S performance comes at the expense of short-term financial performance.

Voting differences among E&S proposals

Consistent with the financial incentives highlighted, we find that active ESG funds are more likely than passive ESG funds to oppose E&S proposals.

We also show that ESG funds whose fund flows are sensitive to performance are more likely to oppose E&S proposals because of a greater loss of future inflows induced by lower returns. The effect is particularly sizable for climate-related proposals.

Voting patterns are more aligned between ESG and non-ESG funds within ESG-oriented fund families and when these issue E&S-specific voting guidelines.

We find that investors in ESG funds modestly respond to negative E&S votes by withdrawing capital around the vote disclosure date. Consequently, this potentially enables ESG funds to sustain differential voting shown above, even though it likely does not reflect their investors’ mandates on E&S issues.

Takeaway

Taken together, our results highlight that conflicting objectives of advancing sustainability and achieving financial returns can impede improvements in corporate sustainability, due to the perceived performance trade-off required.

Specifically, we document that ESG funds vote differently than non-ESG funds in close votes, with proposals that barely pass generating lower stock returns.

From a policy perspective, this suggests that regulators and investors face an uphill battle to promote an integrated approach to ESG investing that creates long-term value for ESG-oriented investors. In this regard, we believe that the SEC’s proposed rule mandating ESG funds to explain how proxy voting fits into their ESG strategies is a useful first step.

References

[1]The US Securities and Exchange Commission (SEC) launched its Climate and ESG Task Force in 2021 to identify ESG-related misconduct, resulting in charges against funds managed by BNY Mellon and Goldman Sachs Asset Management.