Integrating ESG factors is beneficial for investment decision making. Increasing numbers of asset owners and investors can agree on this, but there is a growing realisation that deeper analysis is required.

More and more, investment analysts are demanding further quantitative work on ESG issues and the impact they can have on returns.

With this in mind, a number of recent research papers have begun exploring the impact of the incorporation of ESG factors on the volatility of stock performance.

ESG Factors and Risk-Adjusted Performance: A New Quantitative Model by Kumar Nallan Chakravarthya et al takes what it describes as conventional financial wisdom, which suggests that less risk leads to lower returns, and turns this on its head.

The paper’s main argument centres on the belief that the incorporation of ESG factors provides companies with lower volatility in their stock performance when compared with their peers in the same industry.

Other key findings from the report include research suggesting that ESG factors have a different effect on each industry, and that companies that pursue an ESG agenda generate higher returns.

The authors underpin their findings through the use of their own quantitative model, which they use to show evidence of the link between ESG factors and investment riskadjusted performance. They argue however that this relatively narrow focus overlooks the importance of further investigating the impact of ESG issues on risk. Among the questions that they pose are:

- Is there a difference in the average of the standard deviation of stock prices of ESG positive companies compared to non-ESG stocks?

- Is it possible to quantitatively demonstrate this difference and establish that firms that consider ESG issues bear less risk compared to non-ESG stocks?

- Given that lower risk has traditionally meant lower financial returns, how can ESG investment really offer a viable investment strategy?

ESG investing = higher risk-adjusted returns

Until now, most studies have either focused on defining and evaluating ESG factors and their impact on stock returns or centred on specific investment vehicles such as private equity funds. Instead, this paper analyses stocks by industry in the hope of showing that efficient investment strategies can be developed around listed equity funds or mutual funds. The authors argue that what is different about their model is that it considers factors – notably constant internal and external interactions – beyond the historical assumption that higher risk produces higher returns. The research suggests that, by considering those interactions, the hidden value becomes apparent.

Therefore, the argument becomes not lower risk equating to lower returns, but that lower risk produces the same or higher returns, namely higher riskadjusted returns.

Spotlights on industries

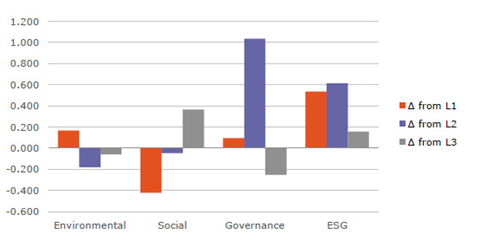

A key finding of the report is that ESG factors affect each industry differently. A total of 12 industries were studied. Energy proved to be the most volatile industry, and insurance the least. In the reference group, the difference between the two was 47%, while in the ESG group there was much less volatility, with just 11% difference. This would suggest that if ESG factors are taken into account when investing in the energy sector, some of the potential risks could be mitigated.

The report found that ESG factors affect each industry differently.

The model also revealed that lower risk did not necessarily translate into lower returns. A total of eight out of the 12 industries showed better returns for ESG companies than their peers. Across all industries, the positive effect on equity return averaged out at 6.12%. Considering the eight industries where ESG factors had a notably positive impact, the average rose to 14.08%. Energy, food and drink, and healthcare showed the most positive results, while conversely a negative impact of ESG factors on returns was seen in the car, banking, durables, and insurance sectors.

Looking at these figures in greater depth, the model showed that equity investments in non- ESG companies could bear as much as 28% or more risk annually when compared to investments in ESG companies in the same industries.

Overall, the differences in volatilities were more pronounced in the group of non-ESG companies than in the ESG ones, prompting the authors to conclude that ESG practices could help companies reduce risk, with the amount depending on industry. Using popular measures for comparing risk-adjusted returns provided some interesting insights. The Sharpe ratio is calculated as the expected return per unit (volatility); so the higher the ratio, the greater the efficiency of the investment. Using this over the 12 industries showed that, with the exception of banking, energy and materials, the Sharpe ratio for ESG stocks in the other industries was on average 7.67% greater than those of the reference stocks in the respective industries.

Similarly, using the Treynor ratio, which compares the return earned on a stock against the beta or market risk of a stock as an alternative risk measure to standard deviation, ESG stocks showed higher Treynor ratios against their reference counterparts in nine of the 12 industries. In this case, the average was 11.81%. The exceptions were the car, banking and durables industries.

Size and industry tilts

NN Investment Partners meanwhile sought to evaluate the performance of global equity portfolios that are formed using ESG criteria in its empirical study, The Materiality of ESG Factors for Equity Investment Decisions: Academic Evidence. Among the paper’s key findings are that standard ESG ratings/scores that are typically used in equity selection tend to be higher for larger companies. Notably, much like the quantitative model, this paper also found a variation across industries. The report’s authors warn that this suggests that those using ESG criteria in their portfolio selection without first making the correct adjustments may find themselves with undesirable size and industry tilts in their equity portfolios.

The other key finding, which appears to support traditional thinking on ESG issues, is they often have a medium to long-term outlook. The paper argues that this underlines the concept that changes in ESG scores can be more informative about future returns rather than levels.

Other factors that improved performance included the exclusion from the rankings of firms that exhibited controversial behaviour (bribery, corruption, human rights abuses, pollution, etc.). This suggests that a relatively simple way to improve portfolio performance is to exclude ESG controversies, which again runs contrary to popular belief.

A relatively simple way to improve portfolio performance is to exclude ESG controversies, which runs contrary to popular belief.

Considering the subsets of ESG factors offers a focus for a third report in this area. ESG and Corporate Financial Performance includes 60 review studies and 2,250 unique primary studies and, as such, is the most extensive on the issue to date. It is a meta-study by Deutsche Asset & Wealth Management and the University of Hamburg, on which the PRI provided support on the communication of academic research insights. 62.6% of studies revealed a positive correlation between ESG investing and financial performance.

It looks at the individual impact of each subset of ESG issues, and found that governance issues produced higher positive results, registering 62.3%. Interestingly, governance-related issues also produced the highest percentage of negative correlations. Additionally, the study found that it was more beneficial to apply the subsets individually rather than as a whole.

The paper broke down the asset classes, revealing that bonds and real estate emerged as asset classes in which ESG investing and performance have a strong link.

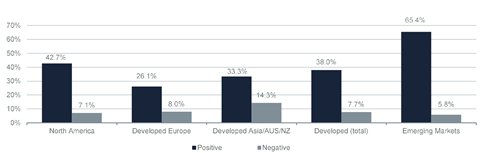

Regional variations were also noted, out of which emerged two distinct patterns: developed markets excluding North America showed a smaller share of positive returns. Europe showed just 26.1% in positive results compared to 42.7% for North America. The second pattern was the strong correlation between ESG and CFP in emerging markets, showing a 65.4% share of positive outcomes.

Governance was brought to the fore in a meta-study produced by The University of Oxford and Arabesque Partners. The report, From the Stockholder to the Stakeholder is based on the examination of over 200 studies. It investigates the business case for corporate sustainability and looks into cost of capital, operational performance and stock price. In terms of considering how sustainability can drive financial performance, it finds that superior governance quality results in better financial performance. It concludes however, that a more granular understanding of ESG issues is needed and that active ownership is the future of sustainable investing strategies.

What these reports highlight is that the materiality of sustainability is undisputed. However, challenges remain and further, deeper research is required to fully understand the impact of the integration of ESG issues on the investment process.

All the reports highlight that the materiality of sustainability is undisputed.

Download the issue

-

RI Quarterly vol. 10: The next frontier for responsible investment

January 2017

RI Quarterly vol. 10: The next frontier for responsible investment

- 1

- 2

- 3

- 4

- 5Currently reading

How ESG investing affects financial performance

- 6