Case study by Union Investment

We created an ESG valuation framework by selecting different ESG factors for each sector – e.g. CO2 footprint for energy companies, labour standards or product safety for retail companies – and embedding it into our classic fundamental analysis. We apply the framework to individual stocks across all sectors, together with sector analysts and ESG specialists.

While it is hard to quantify the social and environmental risks of holding a stock, we try to evaluate the company’s position and outlook by performing a sensitivity analysis to obtain a range of possible fair values. In our experience, integrating ESG analysis generally works better on negative rather than on positive issues.

In valuing a European sport shoes and equipment manufacturer, we took into account concerns and opportunities of the company’s supply chain labour conditions.

Analysing the ESG issue

There had been criticism of the labour standards, particularly poor wages and overtime, at many of the company’s suppliers and sub-contractors in Southeast Asia. After many years of dialogue with the company and after visiting the contracted factories, we saw gradual improvements in the social standards at the company and its suppliers, including improved risk management and enhanced systematic monitoring of social standards. This reduced reputational risk, enhanced the brand and resulted in employees reporting being more satisfied.

Impact on valuation

We embedded these positive observations into our valuation model in two ways:

Sales

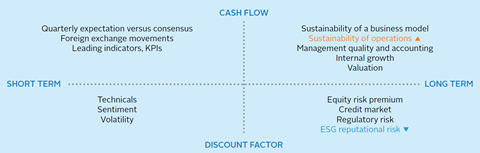

- As we believe that there is a positive correlation between revenue per square feet and social factors such as employee satisfaction, we expect a better sales performance because of a better brand and highly motivated labour forces (at the company and at (sub-)contractors). To take into account the positive implication on sales and cash flows, we increase the market estimates of sales growth by 100 basis points per year.

Discount rate

- Due to implemented measurements, improved risk management and enhanced systematic monitoring of social standards, the company could limit its exposure to public allegations and controversies regarding labour standards. Hence the company’s reputational risk is limited (and has even turned to a reputational benefit compared to its peers), which has implication on our stock valuation model. As a consequence, we decrease the discount rate by 50 basis points.

The sizes of the adjustments are based on past experience with the sector, with the company and its peers, and on the assumption that most other market participants have not integrated sustainability considerations.

Applying the adjusted factors in our valuation model (figure 1) increases the fair value 20%, with the biggest upside coming from the reduced risk factors (about 15%).