Cae study by Aegon Asset Management

| Authors | Emanuele Fanelli, Responsible Investment Manager; and Jesus Martinez, Portfolio Manager |

|---|---|

|

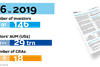

Market participant |

Asset Manager |

|

Total AUM |

US$361 billion (as at December 2017) |

|

FI AUM |

US$276 billion (as at December 2017) |

|

Operating country |

Global |

Acion areas:

- Materiality of ESG factors

- Organisational approach

The investment approach

Aegon Asset Management Netherlands believes that ESG factors are an important component of sound fundamental credit analysis, driving alpha and helping to manage downside and tail risk. Though not always referred to as ESG-related, the underlying concepts have helped to define our investment methodology for decades, and remain an important and evolving part of our investment process. In recent months, we have been conducting in-depth analysis of the opportunities and challenges related to ESG integration in sovereign debt markets.

Integration is not without its challenges. On the qualitative side, traditional CRAs are not always fully explicit about how ESG factors are considered in their methodologies. On the quantitative side, data quality, availability and timeliness limit our flexibility when assessing ESG factors, and our confidence in third-party scores is limited by black-box methodologies. More generally, the financial materiality of ESG factors for sovereigns is subject to the intricacies of development economics. Academic and practitioner research on the issue is still in its infancy, which complicates the assessment because of the multidimensional elements of ESG factors in country assessments.

The investment approach

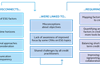

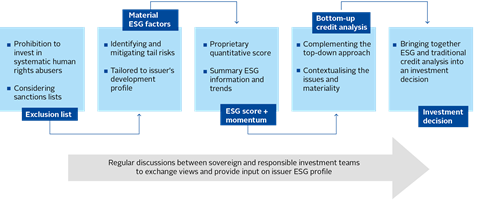

We created a proprietary ESG score for countries with the overarching goal of identifying the financial impact of those factors on sovereign creditworthiness. Therefore, next to our exclusion list that prohibits some countries based on global norms and sanctions, we have developed a proprietary quantitative score.

The score is computed by converting data from public sources into ESG factors, capturing aspects such as institutional strength or climate action. The materiality of those factors is then determined statistically. Since not all factors affect countries in the same way, we differentiate the materiality analysis by country income group, which allows for a more nuanced and realistic approach to ESG factors in sovereign risk assessment. The weights determined by this analysis are then used to aggregate factors into a quantitative ESG score and three sub-scores, which are adapted to each country’s level of development as measured by their GNI per capita and classified by the World Bank (see below).

Our ESG score therefore measures the ESG risk that each country faces given its level of development. We also use a measure of ESG momentum to capture trends in the ESG performance of a country. These measures provide us with a dynamic summary view of the ESG strengths and weaknesses of sovereign issuers. The underlying data are always readily available, with poor performances that might not be revealed in an aggregated score flagged for further research. Sovereign credit analysts also conduct bottom-up research to complement and clarify the insights from our quantitative methodology (see see below).

The combination of bottom-up and top-down approaches gives the investment team a holistic view of the ESG risks and their materiality to a sovereign issuer’s creditworthiness. Further, the responsible investment team advise the investment team at each stage of the process, exchanging views and providing insights into the risks identified, ensuring that the investment team can gradually take more ownership of the process as their knowledge of the issues increases in each cycle.

The investment outcomes

The following case study on Portuguese government bonds shows how our process identifies material ESG issues when analysing sovereign debt markets and how these are addressed.

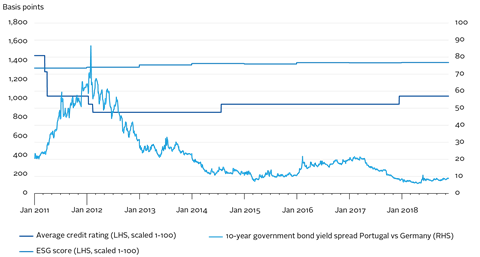

The outbreak of the sovereign crisis in 2012 caused Portugal to be downgraded to below investment grade by all three rating agencies. It took the country five years to regain its former investment-grade status, following severe fiscal adjustments (in 2017 by S&P Global Ratings and Fitch Ratings, and by Moody’s Investors Service in 2018). Since 2012, economic growth has been key to building confidence and stability in the country’s bond market. Portugal’s GDP growth in the last five years has been increasing, after an average of -2 percent in the period after the sovereign financial crisis, and reaching 2.8 percent in 2018. Furthermore, its debt to GDP ratio has recently decreased, having stabilised in 2013-2016.

Credit ratings deteriorated at a similar speed as Portugal’s spread differential against Germany 10-year Bonds, peaking in the second half of 2011 (see below). Relevant short-term indicators such as the ability of the country to access wholesale markets caused investors to adopt a cautious outlook. However, our methodology showed a stable and relatively high score as compared to other countries in the same income group.

Such stability in our proprietary ESG score of Portugal does not reflect the reality of the underlying items that did move during this turbulent period, smoothing out the result. This effect shows that a single number does not describe the complex reality of an issuer, and how necessary it is to evaluate and develop a professional judgement based on accurate and relevant data.

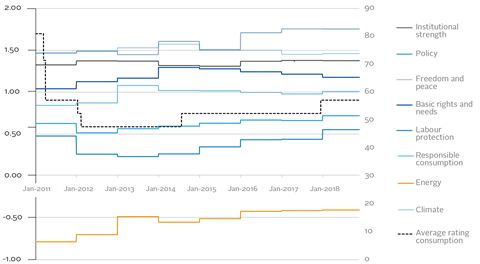

Figure 50 shows how labour protection and policy deteriorated significantly in 2012, mainly due to the implementation of reforms that were aimed at achieving a more flexible economy, which led to salary devaluation. That effect was compensated by generally positive momentum from other indicators such as basic rights and needs or institutional strength.

Since 2012, the reforms have continued and affected several aspects of the Portuguese economy. An example is the steps taken to reduce the energy tariff deficit and increase the use of renewable energy, which started to pay off as of 2013. While most of these policy actions improved the long-term sustainability prospects of the country, valuations remained expensive and ratings were kept low, increasing the attractiveness of Portuguese bonds even before market indicators started improving.

Key takeaways

Our takeaways include that:

- developing and implementing a proprietary score and process helped us build a deep understanding of the issues and opportunities related to ESG factors in sovereign portfolios;

- a one-size-fits-all quantitative approach is not suited to the realities of the sovereign debt market;

- our ESG integration process is not set in stone – we refine our approach each time we go through a cycle of analysis and increase our knowledge and understanding of the issues; and

- our proprietary analysis also helps us meet our client reporting obligations.

Download the report

-

Shifting perceptions: ESG, credit risk and ratings: part 3 - from disconnects to action areas

January 2019

ESG, credit risk and ratings: part 3 - from disconnects to action areas

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

- 11

- 12

- 13

- 14

- 15

- 16

- 17

- 18

- 19

- 20

Currently reading

Currently readingCase study: Aegon Asset Management

- 21

- 22

- 23

- 24

- 25