Case study by BlueBay Asset Management LLP

| Author | My-Linh Ngo, Head of ESG Investment Risk |

|---|---|

|

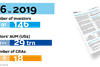

Market participant |

Asset Manager |

|

Total AUM |

US$59.6 billion (as at June 2018) |

|

FI AUM |

US$59.6 billion (as at June 2018) |

|

Operating country |

Global |

Action area:

- Materiality of ESG factors

The investment approach

BlueBay believes that ESG factors can potentially have a material impact on an issuer’s long-term financial performance. Since 2013, we have operated an ESG investment risk management framework across all our managed assets. It involves identifying and assessing material ESG risk factors and integrating these in portfolio construction.

Our efforts to date have centred on working with our credit analysts to share ESG risk insights on an ongoing basis. In 2018, we went a step further, implementing an issuer evaluation process to incorporate ESG risks more systematically into our fundamental credit analysis across our public debt investment teams.

The process was designed to help us achieve the following goals:

- systematically evidence and document ESG integration pre-investment;

- better allow for, and reflect on, how ESG dynamics may play out in FI investing (compared with equities), as well as potentially between different debt strategies;

- advance our understanding of how ESG risk factors may impact different issuer types such as corporates, sovereigns and state-owned enterprises;

- complement ESG insights gained from third parties with in-house knowledge and expertise;

- promote ownership and accountability by having credit and ESG analysts involved in the ESG review process; and

- use insights to inform ESG engagement priorities.

The investment process

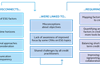

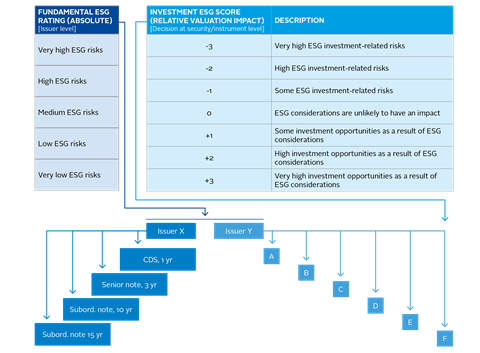

For corporates and sovereigns, the issuer ESG evaluation template generates two ESG metrics (see figure):

- A Fundamental ESG Rating which indicates our view on how well the issuer manages its material ESG risks. There can only be one Fundamental ESG Rating per issuer, e.g. at the ticker level, across BlueBay. This Fundamental ESG Rating is co-owned by the credit analyst(s) and ESG team.

- An Investment ESG Score which reflects an investment view on the extent to which ESG risk factors are considered relevant to valuations. The Investment ESG Score is specific to a decision on a security/instrument level, e.g. at the International Security Identification Number level. Each investment team may assign different Investment ESG Scores, meaning there may be multiple scores for a single issuer. We can therefore consider ESG investment materiality over varying time frames and risk-reward profiles. This Investment ESG Score is owned by the credit analyst/portfolio manager.

Ultimately, the issuer ESG evaluation process enables our credit and ESG analysts to express their ESG views on an issuer before making an investment. The views can then be taken into account by portfolio managers when constructing their portfolios and making investment decisions. However, they are not prescriptive, as there may be valid reasons why the portfolio managers take an investment position that contradicts the ESG signal.

We have disaggregated the management of material ESG risks by the issuer from the investment materiality, as this enables us to better understand the extent to which ESG risks are indeed investment-relevant and in which circumstances. This level of transparency is particularly important in a FI environment, where the asset class operates differently to equity, and ESG factors play out in different ways. Such insights inform our wider knowledge and understanding of ESG FI dynamics, and ultimately allow us to make more informed investment decisions.

A pilot version of the issuer ESG evaluation process was trialled in 2017 by a single investment desk, and further refinements were made as a result of the learnings among a wider group of analysts. It was formally launched in August 2018.

Some key points associated with the template and process are:

- While the specific content of the templates for sovereign and corporates differ, both follow similar principles, have broadly similar structures and generate consistent ESG metrics.

- There can only be a single ESG evaluation completed per issuer, even if an issuer may be relevant for different investment strategies (e.g. investment-grade, high-yield or emerging market debt).

- To encourage credit analysts to think about analysis from a different perspective (ESG), the process has been designed so they lead on the initial ESG evaluation in terms of the Fundamental ESG Rating, which is then submitted to the ESG team for review. The ESG team must confirm the proposed Fundamental ESG Rating, as this is co-owned by the credit and ESG analysts.

- The Investment ESG Score is more dynamic than the Fundamental ESG Rating, and is expected to be updated more frequently.

- The two ESG metrics are integrated into our internal investment holdings and trade monitoring platforms, which enable investment teams to access this data along with conventional issuer credit metrics.

The investment outcomes

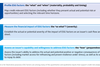

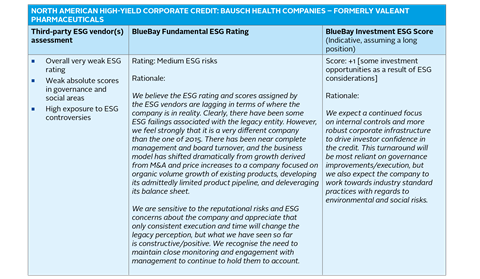

The initiative is already generating value by formalising ESG integration in fundamental credit research and investment decision processes, providing insights into ESG FI dynamics, as well as fostering active ownership and accountability. The example below shows how the in-house issuer ESG evaluation process allows us to explain a view which differs to the ESG vendor assessment, and expresses the nature of the investment materiality.

Key takeaways

The initiative is enabling us to undertake ESG integration more systematically at the fundamental credit research level, although our process will likely evolve and be refined over time, as ESG integration is an iterative process. Our key takeaways so far include:

- Identifying materiality by quantifying ESG risk factors: some analysts have commented that while ESG risks may be discussed in credit meetings and with portfolio managers, having this formal process means they need to express their ESG view in a more quantitative way to make the risks more tangible to grasp.

- Providing an explicit signal to inform investment decisions: the ESG metrics serve as a communication tool from the analysts to the portfolio managers, which they will need to consider alongside other investment factors such as fundamentals, technicals and valuation during their portfolio construction.

- Mutual learning, promoting debate and dialogue: analysts have found that by being directly accountable for the evaluation of ESG risks, they better appreciate how these credits are viewed from an ESG perspective, expanding the way they look at credits. The process has already generated debate and discussions with regards to whether assigned Fundamental ESG Ratings and/or Investment ESG Scores are valid, and the extent to which consistency between teams is needed.

- Promoting ownership and accountability: while having access to third-party ESG vendor data is useful in helping to formulate an initial view, our framework has encouraged investment teams to build on this to formulate their own views on ESG risk factors, particularly where they differ from third parties.

Download the report

-

Shifting perceptions: ESG, credit risk and ratings: part 3 - from disconnects to action areas

January 2019

ESG, credit risk and ratings: part 3 - from disconnects to action areas

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

- 11

- 12

Currently reading

Currently readingCase study: BlueBay Asset Management LLP

- 13

- 14

- 15

- 16

- 17

- 18

- 19

- 20

- 21

- 22

- 23

- 24

- 25