| Author | Claudia Gollmeier, CFA, CIPM, Senior Investment Officer |

|---|---|

|

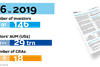

Market participant |

Asset Manager |

|

Total AUM |

US$43.3 billion (as at October 2018) |

|

FI AUM |

US$43.3 billion (as at October 2018) |

|

Operating country |

Global |

Action area:

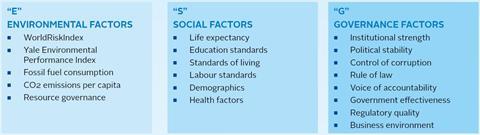

- Materiality of ESG factors

The investment approach

ESG factors have always been an integral part of Colchester Global Investors’ (Colchester) investment process for developed and emerging economies. We believe that countries with stronger governance, healthier and more educated workforces, and higher environmental standards tend to produce better economic outcomes. Typically, this leads to more stable debt and currency paths, which are associated with better risk-adjusted returns.

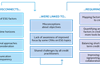

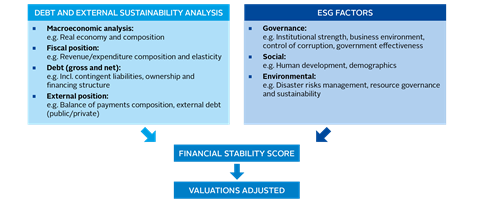

Colchester integrates its assessment of ESG factors into its analysis of a country’s balance sheet (see below).

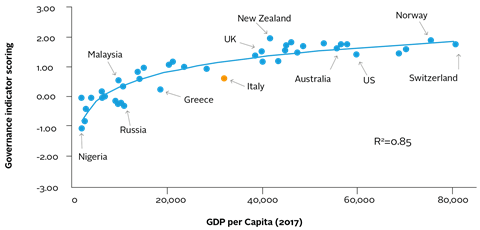

Unsurprisingly, governance is the most important factor when considering sovereign bonds. Not only is stronger governance correlated with higher GDP per capita (see below), it also strongly influences social and environmental factors, as government policies define the framework within which social and environmental outcomes are determined. There is evidence to support the belief that better social conditions – healthcare, educational standards, labour conditions, etc. – have a positive impact on economic outcomes. The positive correlation (R2 = 0.68) between educational standards and per capita GDP is one example. Similarly, a strong link can be found between environmental performance index and a country’s economic outcome (R2 = 0.72). Academic research also supports the notion that countries with higher governance standards tend to have more effective environmental policies.

The investment process

ESG factors are integrated holistically - not formulaically - into our investment valuation framework. Countries are assigned a proprietary financial stability score (FSS) that combines an assessment of their overall balance sheet strength and ESG factors (see below). Bond and currency scores range from +4 to –4, and a country may be excluded from the investment universe if its ranking falls below –4. Colchester penalises a country’s balance sheet for weak ESG factors (for example, Russia), but does not increase the FSS for strong ESG factors. ESG and country research is undertaken by Colchester’s investment team, who also engage with stakeholders, where possible, during country research trips. Such engagement and potential impact is more limited and, by definition, more challenging in the sovereign space compared with corporations.

Colchester invests on the basis of real yields and real exchange rates, adjusted for the FSS. Portfolio construction is based on a standard mean-variance optimisation framework with risk measures and investment guideline constraints. The latter include, among others, client-specific credit limits, which can range from minimum ratings of AA- to below investment grade. The position size is generally a direct function of risk-adjusted potential real returns. Should two countries have equal real yields (unadjusted for their FSS), the one with the higher FSS would be favoured. Specifically, a country with stronger ESG factors is likely to have a higher comparative FSS score that enhances its attractiveness relative to the country that has weaker ESG factors. Underpinning this assessment is the belief that the former is likely to have a better economic outcome and deliver better medium-term returns.

The investment outcomes

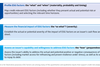

The Italian case study below shows how Colchester’s investment process identifies material ESG issues and how these are addressed.The structural weakness in the Italian balance sheet is long-standing. Political instability has prevented successive governments from implementing lasting structural reforms and limited the country’s growth potential. While Italy compares unfavorably to most other developed world economies on most ESG indicators, weak governance underpins much of this underperformance. Such weaknesses have facilitated tax evasion and corruption, led to inefficient resource allocation, hampered productivity growth and promoted growth in the shadow economy. An inefficient bureaucracy and a complex, slow legal system also increases transaction costs and inhibits activity.

Italy also underperforms across a number of social and environmental factors. While educational standards appear comparable with other OECD countries, Italy suffers skills mismatches, particularly with lower skilled workers, which affects wage and productivity growth. This translates into very high youth unemployment (35 percent as of 2017) and a school drop-out rate (14 percent as of 2017) which is high compared with its peers.

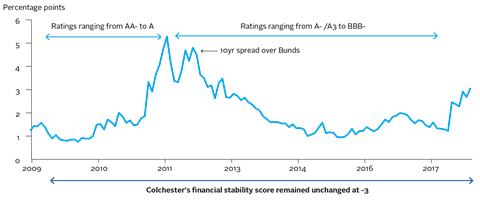

In summary, whilst Italy has made some reform progress recently, has low private sector debt, and is a member of the EU, it has high government debt, structural rigidities, unstable governments and weak levels of governance and social factors. Our assessment of these ESG factors weighs on Italy’s overall FSS, leaving it at the lower end of our FSS range, at -3. Given that these weaknesses have been inherent in its balance sheet for several years, Italy’s FSS has remained unchanged over the past 10 years. Notwithstanding market volatility and credit rating agency pronouncements, the key drivers of Italy’s financial stability have not materially changed over many years (see below). Italy’s potential real yield (FSS-adjusted) relative to other markets, combined with risk management, kept Colchester’s Global Bond Programme underweight the Italian bond market prior to the eurozone crisis. When valuations became more attractive, the bond programme established a gradual overweight in mid-2012, despite the unchanged balance sheet. As Italian yields fell in absolute and relative terms to Germany, Colchester subsequently reduced its exposure to Italian bonds.

Key takeaways

Colchester has incorporated ESG factors within its investment process since the inception of the firm. Colchester believes ESG factors are an important consideration when assessing a country’s financial stability. Stronger, more stable balance sheets combined with positive ESG factors have been associated with better financial outcomes. Incorporating this analysis into our investment process has been beneficial to Colchester’s long-term performance track record.

Download the report

-

Shifting perceptions: ESG, credit risk and ratings: part 3 - from disconnects to action areas

January 2019

ESG, credit risk and ratings: part 3 - from disconnects to action areas

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

- 11

- 12

- 13

- 14

- 15

- 16

- 17

- 18

- 19

- 20

- 21

- 22

Currently reading

Currently readingCase study: Colchester Global Investors

- 23

- 24

- 25