Case study by Futuregrowth Asset Management

| Authors | Angelique Kalam, Manager, Sustainable Investment Practices; and Kearon Gordon, Investment Analyst |

|---|---|

|

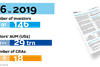

Market participant |

Asset Manager |

|

Total AUM |

US$13 billion (as at October 2018) |

|

FI AUM |

US$12.5 billion (as at October 2018) |

|

Operating country |

South Africa |

Action area:

- Materiality of ESG factors

The investment approach

We believe that integrating ESG analysis into our overall investment decision-making processes leads to better investment decisions and more sustainable returns. We seek to identify non-financial risks (ESG, management, operational etc.) that could impair the credit quality and sustainability of our investments to improve their analysis, assess risks and promote better standards of practice. Our credit strategy promotes independent and in-depth analysis of borrowers. We apply fundamental credit analysis and internal risk measures to analyse, screen, identify and price risks, and negotiate rates and terms. We use a range of criteria to ensure that the risk-reward trade-off is appropriate. We see ourselves as a long-term funding partner and, as such, we view sustainability as key to understanding risk.

Key considerations:

- there is no standardised framework for analysing companies on sustainability issues;

- credit analysts should apply their knowledge as a qualitative overlay to financial, operational and other risk analysis;

- considering ESG factors improves the analysis of all investments by promoting improving standards of practice;

- identifying risks that could affect the cost of funding such as operational disruptions is important;

- ESG indicators are one of many credit risk tools that should form part of a holistic credit process;

- rates charged for loans should be appropriate for the risk-reward assumed; and

- good governance practices and processes are fundamental in assessing the sustainability of a company.

The investment process

We use the example of our approach to analyse MTN Group (MTN), an African telecommunications network provider, to illustrate our investment process. Futuregrowth has had opportunities to acquire debt exposure to MTN through auctions and the sell-down of debt from other financial institutions. The Futuregrowth Credit Team held discussions to consider these opportunities, with a focus on the company’s governance issues. Key considerations were whether we could address the risk through only considering short-term exposures, and whether the returns would sufficiently compensate our clients for the risk associated with the counterparty.

ESG factors aside, MTN’s financial fundamentals paint a positive credit picture. However, once ESG factors are considered, a weaker credit view emerges, owing to poor governance practices and seemingly a culture of non-compliance with regulations. Following several significant and publicised risk events (see below) we downgraded the counterparty multiple times over the past few years. While we consider credit rating agencies, our ratings are based on an internal assessment of the risk of default based on financial and non-financial metrics (including ESG factors). Our internal ratings are generally more conservative than those of the ratings agencies. MTN’s credit rating was downgraded from Baa3 to Ba1 by Moody’s in June 2017, citing the weakening credit profile of the government of South Africa (SA), and the resulting downgrade of the SA sovereign rating to Baa3 and a negative outlook. Moody’s subsequently placed MTN Group on review for a further downgrade in September 2018.

Credit factors

MTN’s financial fundamentals weakened dramatically in the 2016 and 2017 financial years, including profitability, as a result of a US$5.2 billion fine by the Nigerian Communications Commission for regulatory failures (the disconnecting of unregistered SIM cards). Some of its revenue growth challenges originated from losing many customers off the back of regulatory failures, coupled with the inherently volatile macro-economic markets MTN operates in. However, the balance sheet remains relatively strong and it continues to generate a healthy cash flow, allowing it to service its debt. MTN is, however, significantly more geared than its competitors. Some of the fundamentals have shown signs of normalisation, and, if the trend continues, it would improve our view of the financial strength of the group.

Governance factors

In addition to the financial and credit fundamentals, we focused on governance factors. For example, we evaluated and reviewed governance structures as well as broader indicators of MTN’s legal and regulatory investigations and sanctions in recent years. We found an absence of governance and risk management specialists on MTN’s board, though there are some individuals with experience in higher-risk territories in Africa. Historically, the group had no standalone Risk Committee – this task was delegated to the Audit Committee. Additionally, MTN operates in a highly regulated environment, across numerous jurisdictions and often in politically conflicted or troubled regions with nuanced legal and regulatory environments. In isolation, this presented heightened risk, including legal and regulatory non-compliance. Its operating environment added to our concerns about existing governance weaknesses. And while there is racial diversity on the board, gender diversity is lacking.

The group did, however, make some positive changes subsequent to the Nigeria fine, including:

- the board and shareholders approved the hire of Rob Shuter as group CEO and Ralph Mupita as CFO, as well as Stephen van Coller as M&A and Strategy Executive (who has subsequently left the group);

- amending its governance structures with the introduction of an executive responsible for governance; and

- the separation of the risk management function to report directly to the board.

However, as at the date of our most recent review, we were not confident that the changes in governance structures implemented by the new management team were sufficient to reduce the risk of non-compliance to an acceptable level. Furthermore, we were also wary that previous governance shortfalls may give rise to legal and regulatory sanctions in future. This view was vindicated by the recent actions taken by the Nigerian Central Bank and the tax authorities.

Implications for spreads

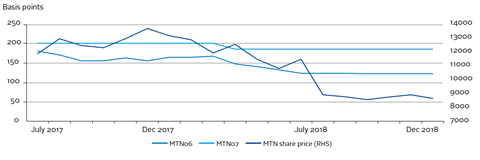

There is limited secondary trading in MTN’s debt and we have not seen major bond spread widening of the listed debt in response to governance risk events in recent years. On the contrary, spreads have remained unchanged, or have even narrowed. We believe this is a consequence of a lack of appreciation in the bond market of these regulatory risks, as well as the fact that most debt investors apply a buy-and-hold strategy. This does not allow for the level of active trading required for spreads to accurately reflect the risks.

In contrast, equity markets have reacted negatively, and MTN’s share prices have fallen significantly over the past year (see below).

The investment approach

MTN is well-positioned in the SA market as well as in the other 22 markets in which it operates (due to the financial fundamentals that suggest a positive credit view and geographic diversity). Margins remain sound, and profitability is recovering following the fine by the Nigerian Communications Commission. Furthermore, markets outside of SA remain high-growth geographies, with MTN set to benefit from increased subscriber levels. This does, however, come with regulatory and political risk within the various jurisdictions MTN operates in, as well as the governance issues noted above, and the fines (in Nigeria) and lawsuit (in Iran) being evidence of some of the most pressing concerns.

Despite recent changes made to the executive, and comments from the CEO about improving the culture of operations, as well as other improvements noted above, the decision was made to not invest in longer-term instruments until reports of regulatory transgressions subside, investors have greater clarity on the Nigerian fine, and the current board and management team show they are committed to implementing new governance processes and policies. However, if the trend of normalising fundamentals continues, our view on the financial strength of the group would likely improve.

Key takeaways

Through this case study, we have demonstrated how the Futuregrowth Credit Team assessed MTN in terms of credit and ESG issues, particularly the company’s governance. We have illustrated what the impact of poor governance can have on our credit outlook, credit rating and investment decision.

While the financial fundamentals appeared relatively sound, poor governance practices in the past presented a significant risk that we did not feel had been adequately priced and hence we have repeatedly declined investment opportunities in the counterparty. We agreed that we would continue to monitor the counterparty as a means of assessing whether the new board and management team has been successful in changing the governance culture of the organisation and addressing legacy governance issues.

We recognise that sound governance is a crucial factor to ensure that companies accessing public capital markets are sustainably managed for the long term. We have found that non-financial issues like ESG do matter, since they can impact a company’s long-term performance and sustainability. As a fiduciary asset manager, we are responsible for managing our clients’ funds in a sustainable and responsible manner that considers an appropriate risk-reward payoff. The end result is to provide sustainable returns that contribute to clients’ long-term return objectives.

Download the report

-

Shifting perceptions: ESG, credit risk and ratings: part 3 - from disconnects to action areas

January 2019

ESG, credit risk and ratings: part 3 - from disconnects to action areas

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

- 11

- 12

- 13

Currently reading

Currently readingCase study: Futuregrowth Asset Management

- 14

- 15

- 16

- 17

- 18

- 19

- 20

- 21

- 22

- 23

- 24

- 25