Case study by Nomura Asset Management

| Author | Jason Mortimer, Senior Portfolio Manager |

|---|---|

|

Market participant |

Asset Manager |

|

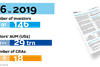

Total AUM |

US$450 billion (as at 30 September 2018) |

|

FI AUM |

US$156 billion (as at 30 September 2018) |

|

OPERATING COUNTRY: |

Global |

Action area:

- Materiality of ESG factors

The investment approach

The launch of a specialised investment-grade corporate debt strategy led Nomura Asset Management to develop a quantitative ESG risk and portfolio analysis framework focused on corporate sustainability issues material to credit investors. Our research showed that credit portfolios of higher ESG quality have fewer rating downgrades and higher Sharpe ratios, two key performance measures for FI. Companies in this strategy’s investment-grade universe operate in mature, asset-heavy industries and regulated sectors, vary in terms of corporate governance quality and business ethics risk, and have exposure to long-term challenges such as asset impairment from the low-carbon transition. This creates opportunities for credit quality and performance differentiation from ESG integration.

However, traditional external ESG ratings by specialised service providers often reflect governance materiality from an equity shareholder perspective, in ways that may differ or conflict with credit investor priorities. These ESG ratings often emphasise growth opportunities from sustainability that are difficult for debt holders to monetise. As FI investors, we are primarily concerned with the potential for ESG factors to materialise as downside to our investments, so an ESG assessment focused on credit-material, downside risks is necessary. Our challenge was to design a quantitative framework to assess the ESG quality of corporate credits, complementing the team’s existing fundamental (i.e. qualitative) approach to ESG integration. We believe the quantitative framework will improve the sustainability and quality of the strategy’s financial returns, and – via the market price signal and capital allocation – send a clear message to companies that outperformance in sustainability issues is a key feature of their assessment by investors.

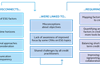

The investment process

We augmented our existing fundamental ESG credit research with a quantitative framework for identifying and assessing ESG quality, with focus on downside credit risks.

The quantitative framework has two steps:

- Mapping industries against sustainability issues that are financially material, credit-focused, and have identifiable downside risk potential, to derive industry-specific ESG weights; and

- Quantifying the ESG quality of corporate credits by applying the weights derived in step one to our own assessment of ESG performance, based on industry-specific, credit-relevant, and downside-risk focused sustainability issues.

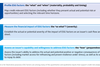

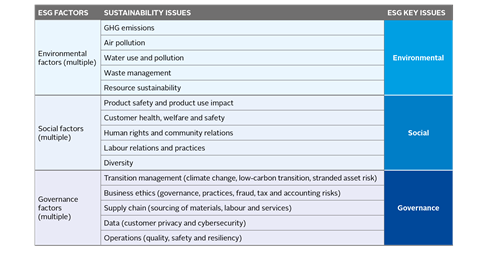

For step one, we identified a starting set of ESG factors that are potentially relevant to corporate credit assessment by referencing SASB, GRI, CDP, PRI resources and in-house expertise. We consolidated these ESG factors into a set of sustainability issues, and categorised these into ESG key issues (see below).

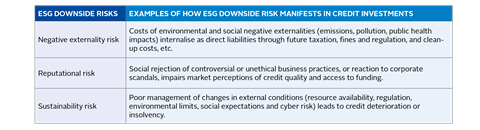

A key requirement for our quantitative framework was that it only includes credit-relevant sustainability issues for each industry if it had specific downside potential risks. Firstly, we defined these as negative externality risk, reputational risk and business sustainability risk (see below).

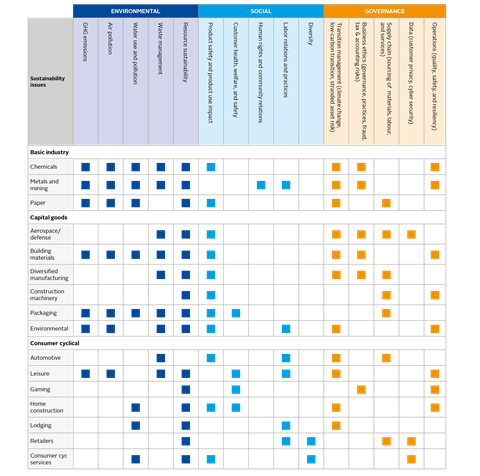

Subsequently, for each sector, we considered as material only sustainability issues with a clear link to financial credit quality (see below).

To complete step one, we used our credit materiality map to derive industry-specific weights for each ESG key issue. ESG key issue weights are a function of the number of sustainability issues per ESG key issue, for each industry and relative to all other industries. The underlying concept is that industries naturally have varying degrees of exposure to ESG risks, but the factors with the highest exposure in relative terms determine which are the key drivers of ESG risk pricing, and ultimately contribute the most to determining ESG quality. Relying on our proprietary credit materiality map to attribute these weights ensures objectivity and internal consistency.

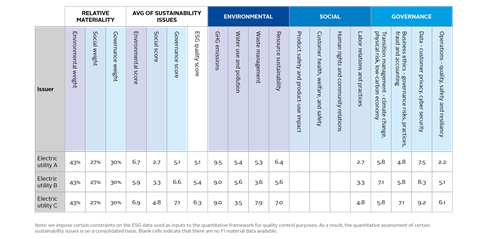

In step two, we generate weighted corporate ESG quality scores, based on our assessment of performance against credit-material sustainability issues. We assess the material sustainability issues for each company with a score based on the average of a sub-set of corporate ESG factors from a third-party ESG ratings provider. Sustainability issue scores for each company are aggregated as three ESG key scores, and finally as an overall ESG quality score based on that company’s industry-specific weights derived in step one. By only incorporating data from credit-material ESG factors, and deriving ESG weights from our mapping of credit and downside risk-based materiality, we aim to improve the usability of the quantitative framework with outputs that are transparent and relevant to the decisions we make in our credit investment process.

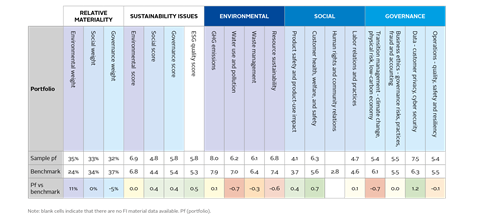

These steps are integrated into our security selection and portfolio construction process to augment our fundamental analysis of credit and qualitative ESG considerations. Individual corporates can be objectively evaluated based on ESG quality and sustainability issue scores, independently and versus industry peers, at the global, regional and country level to identify credit-material areas of relative strength and weakness for further analysis (see below). Aggregate data provides insight into performance across material ESG and sustainability risks across the portfolio (see below). Portfolio-level ESG quality statistics can be compared to targets or benchmark indices to identify potential areas of underperformance. Based on these results, analysts and portfolio managers conduct targeted follow-up analysis, which can result in changes to the portfolio.

The investment outcomes

Our ESG quality assessment has a direct impact on security selection and portfolio construction. In one case, an insurance company (external credit rating BBB-) under consideration for portfolio inclusion was internally rated positively on financial factors but ranked low on social and governance quality. Further investigation revealed sustainability concerns from concentrated and entrenched leadership, and weak responsible investment practices. As a result, the credit was not included in the portfolio.

In another case, ESG quality analysis of a prospective model portfolio with high exposure to environmental and governance key issues revealed that the model portfolio in aggregate underperformed in these areas. This was traced to an emerging market oil and gas credit (external credit rating BBB+) with exceptionally poor performance in waste management, environmental sustainability and operations safety. Despite this credit’s attractive risk-adjusted spread, we replaced it with a higher ESG quality credit that also fulfilled the investment mandate. Clear communication of our quantitative ESG framework to issuers will, we expect, work to “complete the circuit” by highlighting how and why specific sustainability issues matter in their assessment, thus encouraging improvement across all companies.

Key takeaways

The development and application of this quantitative framework aids our ESG analysis by focusing on sustainability issues with identifiable downside credit risk elements. The in-depth look at external ESG rating agency factors used as inputs to our framework highlighted the need for these data providers to produce more granular data for investors to apply tailored, flexible approaches across asset classes. We plan to further explore the alpha potential of ESG and credit risk-adjusted corporate spreads, the integration of corporate and sovereign ESG ratings, and the introduction of a duration element to the weighting formula.

Download the report

-

Shifting perceptions: ESG, credit risk and ratings: part 3 - from disconnects to action areas

January 2019

ESG, credit risk and ratings: part 3 - from disconnects to action areas

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

- 11

- 12

- 13

- 14

- 15

- 16

- 17

- 18

Currently reading

Currently readingCase study: Nomura Asset Management

- 19

- 20

- 21

- 22

- 23

- 24

- 25