This report introduces a core component of the Inevitable Policy Response (IPR): the Forecast Policy Scenario (FPS). The IPR is a pioneering programme which aims to prepare financial markets for climate-related policy risks. What is “Inevitable” is some further policy response as the realities of climate change become increasingly apparent. The key questions for investors are when this response will come, what policies will be used, and where the impact will be felt. The IPR forecasts a response by 2025 that will be forceful, abrupt, and disorderly because of the delay.

The IPR: Forecast Policy Scenario (FPS) models the impact of the forecasted policies on the real economy up to 2050, tracing detailed effects on all emitting sectors, including changes to energy demand (oil, gas, coal), transport, food prices, crop yields, and rates of deforestation. Later in the year, the programme will publish detailed modelling of the implications of the IPR FPS for key asset classes.

Forecast Policy Scenario: Macroeconomic results (PDFs)

A fully integrated modelling framework from policy to financial markets

Markets today lack a strong basis for pricing climate transition risk, and do not seem to have priced in a forceful policy response to climate change within the near-term. According to the PRI’s own analysis, only 2 percent of its signatories which include the world’s largest investors are “strategic” in their assessment and reporting of climate risk.

This leaves portfolios exposed to significant risk. In anticipation, PRI in collaboration with Vivid economics and Energy Transition advisors have developed the Inevitable Policy Response (IPR) project, which includes:

- Forecast policies– A robust real-world analysis outlines and justifies the forecast of what policies the economists expect to see

- The Forecast Policy Scenario (FPS) – introduced in this report, which models the impact of these policies on the overall economic system, tracing detailed effects on all emitting sectors

Value Add of the Forecast Policy Scenario (FPS)

- A high conviction policy-based forecast, not a hypothetical scenario that optimizes policy to meet a temperature constraint

- Transparent: on expectations for policy and deployment of key technologies, such as Negative Emission Technologies

- Complete: includes macroeconomic, energy system, and land use models linking crucial aspects of climate across the entire economy

Fully integrating land-use to ensure the full system impacts of policies, and highlight the critical role of land use

Significant and disruptive consequences

The Forecast Policy Scenario (FPS) reveals a set of striking and highly consequential results for investors and companies.

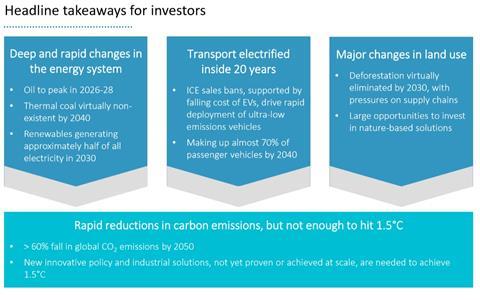

1. Deep and rapid changes in the energy system

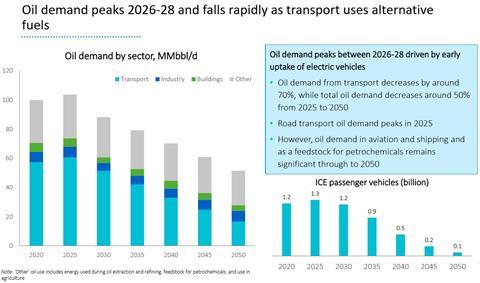

- Oil peaks between 2026-28, driven by a 65% decline in demand from vehicles with internal combustion engines between 2025-2050. Oil in road transport peaks in 2025.

- Thermal coal for electricity generation has reached its peak, and declines rapidly by an average of 6 percentage points per year from 2025 to 2040 at which point it is virtually non-existent

- Natural gas peaks around 2040, playing a role in reducing emissions from heating and decarbonising industry until it is starting to be replaced by zero-carbon electricity from hydrogen from 2040 onwards

- Solar and wind alone will be generating approximately half of all electricity in 2030 and two-thirds of all electricity by 2050. The Forecast Policy Scenario (FPS) expects 74% of power will come from renewables (solar, wind, hydro and others) in 2040.

2. Transport electrified inside 20 years

- Vehicles powered by internal combustion engines (ICE) sharply decline from 2025 and by 2040 ultra-low emissions vehicles outnumber ICE vehicles two to one, driven by 2035 ICE sales bans in Western Europe and China, and 2040 sales bans in USA, Japan and other regions

- ICE sales bans, supported by falling cost of EVs, drive rapid deployment of ultra-low emissions vehicles, making up almost 70% of passenger vehicles by 2040.

3. Deforestation virtually eliminated by 2030, with forests recovering to 1995 levels during the following decade.

- This drives big changes for agricultural commodity supply chains as they adjust to stricter controls on deforestation

- Competition for land results in a significant increase in investments in yield-enhancing technologies, boosting food productivity by 58% between 2020 and, helping to lower food prices as a proportion of household expenditure (from 4.8% to 3.8%) as GDP per capita grows

- Wider land use shifts include growth in bioenergy crops which meet around 10% of global energy demand by 2050

Rapid reductions in carbon emissions, but not enough to hit 1.5C

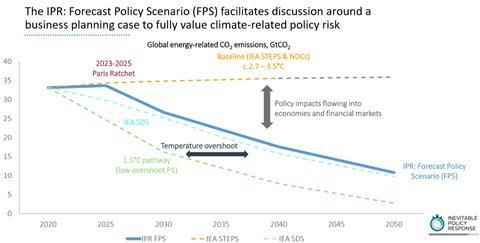

The Forecast Policy Scenario (FPS) expects rapid global emissions reductions, falling 60% from 2020 to 2050 – putting the world on a path towards 2°C – but overshooting the crucial 1.5°C target advocated by scientists. The project identifies three key limits on progress to 1.5°C:

- Lack of meaningful, co-ordinated climate policy before 2023-25.

- Limited deployment of carbon capture and storage (CCS) technology driven by concerns about availability of bioenergy.

Continued rising global consumption of ruminant meat (especially beef) despite a shift in diets towards chicken and plant-based options. The persistence of methane and nitrogen oxide from livestock and fertiliser use offsets the positive story of reduction of 631 GtCO2 e in the land use sector against current baselines.

The Inevitable Policy Response (IPR) therefore includes an ‘aspirational discussion’, which highlights the challenges the 1.5°C ambition will need to overcome given current political and technological realities and pinpoints specific areas where stakeholders need to act now to achieve such goals.

Downloads

Forecast Policy Scenario: macroeconomic results (summary)

PDF, Size 1.95 mbForecast Policy Scenario: macroeconomic results (full report)

PDF, Size 4.43 mbIPR FPS databook 2019

Excel, Size 71.77 kb