Analyses of governance factors such as remuneration and financial auditing are common among bond investors, but few systematically integrate a wide range of ESG factors into credit analysis.

Corporate governance factors (e.g., a company’s accountability, risk management and director independence) can have strong links to credit strength. Corporate scandals linked to fraud and bribery frequently lead to punitive fines, loss of licence to operate and greater scrutiny from regulators. Conversely, well-managed companies tend to be more aligned with bondholder interests, while corporate transparency keeps bondholders better informed of exposure and management of risk.

Social issues, such as poor health and safety standards or community relations, can also affect creditworthiness if poorly managed. Strike action and productivity have a significant impact on operations. In addition, if governments introduce further regulation to address environmental trends such as climate change, then certain sectors are likely to experience rising operation costs and falling demand for carbonintensive products or activities, particularly in energy production and coal mining.

- For more information on the links between ESG factors and corporate credit risks, see Corporate bonds: Spotlight on ESG risks

The materiality of different ESG factors depends on the sector the issuer operates in. Investors either determine their own ESG indicators and scores for each issuer or source information from external research providers.

| ENVIRONMENTAL | SOCIAL | GOVERNANCE |

|---|---|---|

| Climate change | Human rights | Shareholder rights |

| Biodiversity | Employee relations | Incentive structure |

| Energy resources and management | Health and safety | Audit practices |

| Biocapacity and ecosystem quality | Diversity | Board independence and expertise |

| Air pollution | Customer relations | Fiduciary duty |

| Water scarcity and pollution | Product responsibility | Transparency/accountability |

“I think integrating ESG is one of the most powerful things investors can do. Putting a price tag on ESG factors using a market mechanism will provide the right incentive structure over time for the corporate sector to deal much more consciously and strategically with ESG issues. If we don’t change behaviour, we don’t change much.”

Manuel Lewin, Zurich Insurance

Key considerations for corporate bond investors

- Assessing governance risks can limit surprises, such as sudden or aggressive changes to financial policy, management structure and short-term incentive plans.

- Develop a bottom-up approach for addressing ESG risks to corporate creditworthiness and leverage crossover where it exists with equity research teams.

- ESG integration should be considered an important aspect of any fixed income investing.

- Identify material ESG risks relative to sector by narrowing down larger lists and back-testing.

- Apply sector-specific weights to determine overall ESG score or rating.

- When will an ESG factor be material? Consider changes in materiality for different durations.

- Conduct ESG analysis on subsidiary and parent company.

- Consider disclosure in bond prospectuses and covenants as part of governance analysis.

- Consider ESG analysis as a possible tool to identify relative value trades.

- Private placements provide significant opportunities for ESG integration and engagement and for investors to manage ESG risks.

- Corporate bonds are subject to eevent risk f, which can show up as a regulatory, litigation or reputational liability to the company.

- Responsible investment in high-yield bonds shares more characteristics with equity investing . greater risks but more engagement opportunities.

Applying sector weightings to E, S and G factors

Having decided which ESG criteria to integrate into credit analysis, investors need to measure and weight them as part of an aggregated ESG score or rating. Most agree that governance should be weighted most heavily, as these factors relate more closely to management quality and overall creditworthiness. There is little consensus on the importance of environmental and social measures, as these can vary by sector.

Different ESG lenses should be applied to different business sectors. While governance is universally important, environmental issues such as water stress are only likely to be material for certain sectors, such as extractives, food and beverage, and agricultural companies. For airline companies, fuel efficiency may be a key environmental and financial metric. A carbon-efficient issuer is less likely to be susceptible to fuel price volatility. If fuel costs rise, the issuer will be under less pressure to cut other costs to preserve revenues. In addition, a less carbon-intensive airline fleet will typically fare better under possible future carbon regulations. Cathy Roy, CIO at Calvert Investments, says that its analysis “shows that airline companies with younger, more energy-efficient fleets have higher appraised values and thus perform better on collateral coverage metrics in enhanced equipment trust certificate deals”, thereby making for a more attractive long-term investment proposition.

“Five or six years ago we decided to weight each indicator by sector. For example, we weight the social part higher than the environmental part for banks, whereas for energy companies it would be the other way around.”

Christoph Klein, Deutsche Asset & Wealth Management

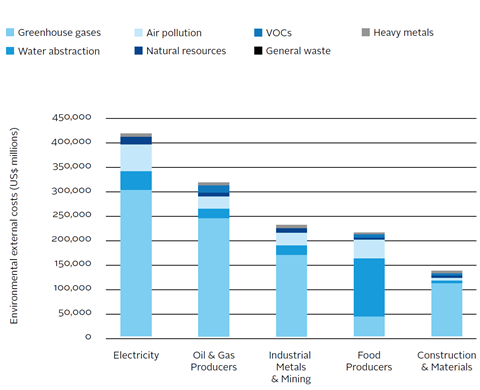

There is a continuing trend in regulations to mitigate or internalise certain external costs. Companies that are not in a position to address these risks may experience higher operating costs or other financial penalties and may be considered less creditworthy as a result.

Focus on environmental issues

The Environment Agency Pension Fund (EAPF) provides pensions for employees and former employees of the UK Environment Agency. It works with its corporate bond manager Royal London Asset Management (RLAM) and ESG research provider Trucost to monitor the total environmental footprint of its corporate bond fund. Integrating this information into the EAPF’s and RLAM’s investment decisions helps account for financially material environmental risks and determine environmentally sustainable investments. EAFP says that “RLAM have found the analysis useful in identifying bonds that are linked to high impact activities and, where practical, replacing them in the portfolio where another bond can meet the same portfolio needs but with less impact.” In 2012 the fund’s environmental footprint was 23 percent lower than its benchmark, the broad-based iBoxx index.

“We think about issues like pollution and ask: Which companies have a solution? Valeo [a French automotive manufacturer] is a good company because it offers weight reduction and stop-start technology for cars and offers ways to reduce CO2 outputs. So we see it increasing market share as demand increases for these types of products.”

Marc Briand, Mirova

Focus on high yield

High-yield issuers by nature, are more susceptible to impacts from ESG risks. Issuers tend to be smaller; many are private companies and, therefore, do not have to report the same information or operate to the same standards. They are more likely to have unconventional governance structures that may be misaligned with creditor interests. As a result, quality of governance is even more central to the process of determining creditworthiness. In addition, investors should focus on an issuer’s capacity to survive low-impact/high-frequency events – for example, how chemicals manufacturers manage exposure to industrial accidents via health and safety standards or how a mining company manages the risks of possible shutdowns due to industrial action.

We’ve done some internal back-testing where we’ve compared the CDS [credit default swap] spread behaviour of a universe of top and bottom ESG performing companies across various leverage thresholds, over an extended timeframe. We generally observed that ESG efficacy was greater in companies with higher leverage. We also observed that those companies that did not disclose any ESG data tended to underperform companies with low ESG scores. This could imply that a lack of transparency is consistent with an even lower ESG profile.”

Kim Nguyen-Taylor, Calvert Investments

Focus on private placements

Private placements are tradable debt securities issued to a relatively small and select group of investors. Private placements do not have to be registered with the US Securities and Exchange Commission (SEC), but the market is regulated by the North American Insurance Commissioners (NAIC). The US$50 billion private placement market is dominated by insurance companies aiming to match insurance liabilities with shorter-term bond issues. These investors tend to take a buy-and-hold approach because the market is relatively illiquid. Credit ratings for privately placed bonds are issued after the bond is issued, and the average issuance period is 12 weeks. Most issues range from US$100 million to US$1billion. These key characteristics mean that private placements are particularly well suited to a responsible investment approach that is quite distinct from normal corporate bonds.

- Relatively poor transparency, the lack of divestment options and relatively large ticket sizes require thorough investor due diligence.

- Longer issuance periods allow investors to engage issuers and identify ESG risks before committing to invest.

- Investors can also use ESG concerns to negotiate with issuers on coupons due to the relatively close relationship between both parties.

- Investors can take up the opportunity to impose disclosure and reporting requirements to more precisely address ESG concerns.

“The process for unlisted investments is very different as opposed to buying a listed bond – this could take a few months before a transaction is approved. In-depth analysis is conducted, so the analyst has a lot of insight into the company.”

Angelique Kalam, Futuregrowth Asset Management

Download the full report

Sponsored by KfW and Union Investment

Fixed income investor guide

- 1

- 2

- 3

- 4

Currently reading

Currently readingAnalysing corporate (non-financial) issuers

- 5

- 6

- 7

- 8

- 9