By Sehoon Kim and Nitish Kumar, University of Florida; Jongsub Lee, Seoul National University, and Junho Oh, Hankuk University of Foreign Studies

Financing agreements between investors and firms are increasingly taking environmental, social, and governance (ESG) concerns into account, reflecting a growing demand from financial stakeholders and broader society that they do so.

Despite bank loans being the primary source of debt financing for firms around the world, little is known about their role in the rapidly evolving ESG-contingent financing space.

In our study, we document and characterise the growth of sustainable lending globally, investigate the role of loan contracts in incentivising borrowers’ sustainability commitments and highlight the importance of transparent disclosures to alleviate greenwashing concerns.

The rise of sustainable lending

In recent years, the sustainable loan market has grown exponentially, driven largely by the widespread use of general-purpose sustainability or ESG-linked loans, which have terms contractually tied to the sustainability performance of borrowing companies.

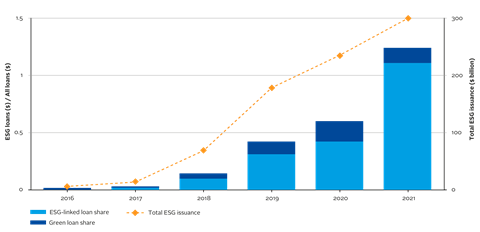

Global sustainable lending activity grew from US$6 billion in January 2016 to US$322 billion in September 2021. As of that month, sustainable lending represented more than one-tenth of the global corporate syndicated loan market, while 90% were sustainability-linked loans (see Figure 1).

Green loans, whose proceeds are earmarked for financing sustainable projects, make up a smaller segment of this market.

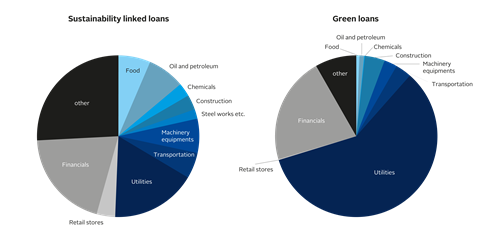

The proliferation of these general-purpose loans has allowed sustainable lending to spread across industries beyond just utilities, where a greater portion of green loans and bonds remain concentrated (Figure 2).

Figure 1. Rise of sustainable lending

Figure 2. Sustainable lending by industry

While sustainability-linked loans originated in European economies with more stakeholder-value oriented rules and regulations, they are now flourishing in the US and across well-developed private credit markets more generally.

What explains the growth of ESG lending?

These loans enable borrowers to credibly signal their ESG commitments to external stakeholders, who increasingly require transparency on firms’ responsible investment practices.

Lenders are also incentivised to supply sustainability-linked loans because of the downside protection that good ESG practices can provide, or in response to regulatory and governmental pressure on banks to conduct their lending businesses more responsibly.

But firms and banks may also engage in sustainability-linked borrowing and lending for greenwashing purposes to showcase an empty emphasis on ESG to stakeholders.

We analyse these possibilities in our study.

Sustainability-linked loans tend to be large – with an average deal size of US$937 million, nearly 80% larger than regular loans. They tend to be issued to larger, safer, and publicly listed borrowers, consistent with the idea that large and economically important firms have strong incentives to demonstrate ESG-friendly practices, given their high visibility and scrutiny from stakeholders.

Such loans are structured mainly through revolving credit facilities and are more likely to be syndicated by larger groups of lenders (often global banks) that have previous relationships with the borrower and have past sustainable lending experience.

They are priced similarly to regular loans at issuance, suggesting that borrowers that meet future ESG performance targets may enjoy lower spreads, according to their ESG performance pricing contracts.

Sustainability-linked loans could be used to effectively monitor, enforce, and renegotiate ESG contingencies in lending contracts – banks, after all, specialise in screening and monitoring their loan portfolio.

However, an important concern that undermines this potential is that large and visible companies and banks facing stakeholder pressure may use their relationships to facilitate greenwashing.

Contractual disclosure quality and greenwashing

We manually assessed the loan disclosures provided by Refinitiv and found that the disclosure of sustainability-linked loan contractual details is generally low, with considerable variation in the amount of information disclosed.

This reflects the difficulty of verifying the validity of ESG loan labels or gauging what real impact they may have in governing borrowers on sustainability issues.

To better understand these and to shed more light on greenwashing concerns, we examine borrowers’ ESG performance around sustainable loan issuances and investigate how this performance varies with disclosure quality.

We find that:

- borrowers and lenders with previously good ESG profiles choose to enter into sustainable loan contracts;

- borrower ESG scores deteriorate after sustainable loan issuance, particularly for loans where the disclosure of ESG-contingent contractual details is poor.

This is consistent with greenwashing – large borrowers and global lenders that both have reputational incentives use their lending relationships to enter into sustainable loan contracts and signal their ESG commitments, without putting these commitments to action.

Investors are vigilant against such greenwashing possibilities, however. We find that stock markets react positively to public announcements of sustainability-linked loan issuance only when the quality of contractual disclosures is relatively high.

Therefore, it is possible that increased public scrutiny and more established disclosure rules will enable the sustainable lending market to mature and develop a more central role in the push towards increased ESG considerations in corporate policies.

Conclusions

Our study complements recent work on the market for green bonds, whose proceeds finance specific green projects (see Flammer, 2021; Tang and Zhang, 2020; Zerbib, 2019; Baker et al., 2022).

The widespread use of general-purpose loans that are designed to incentivise firms across industries to improve their overall sustainability profiles, rather than achieve narrower objectives tied to specific projects, helps to democratise ESG contingent financing.

And banks, much like institutional investors, are uniquely positioned to effectively monitor firms’ progress on ESG considerations.

However, they – and other stakeholders more broadly – need to be vigilant about the potential for greenwashing. Transparent disclosures regarding ESG-related contract terms play an important role in alleviating such concerns.

Overall, our findings contribute to a more complete picture of how ESG concerns are reflected in loan contracts and provide guidance for regulating and instituting sustainable finance.

This full version of our paper can be found here, which was presented at the PRI Academic Network Week 2022.

WATCH HERE

The PRI’s academic blog aims to bring investors insights from the latest academic research on responsible investment. It is written by academic guest contributors. Blog authors write in their individual capacity – posts do not necessarily represent a PRI view.

References

Baker, M., D. Bergstresser, G. Serafeim, and J. Wurgler (2022). The pricing and ownership of U.S. green bonds. Annual Review of Financial Economics, forthcoming.

Flammer, C. (2021). Corporate green bonds. Journal of Financial Economics 142 (2), 499-516.

Tang, D. Y. and Y. Zhang (2020). Do shareholders benefit from green bonds? Journal of Corporate Finance 61.

Zerbib, O. D. (2019). The effect of pro-environmental preferences on bond prices: Evidence from green bonds. Journal of Banking & Finance 98, 39-60.