Untangling the chain of stakeholder interests and incentives requires connecting the business objectives of plan sponsors with the growing demand for ESG incorporation by plan beneficiaries, while working within the fiduciary duty requirements of ERISA.

The primary touchpoint is aligning the plan with corporate values, a growing necessity for engaging and increasing the participation and contributions of millennial plan beneficiaries. This becomes the foundation for convincing ERISA plan sponsors that it is part of their fiduciary duty to incorporate ESG into plan investments.

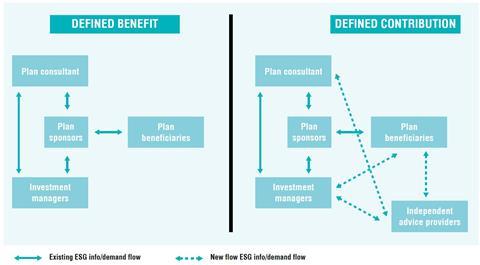

Complexity of defined contribution plans

As shown below, ERISA stakeholder interrelationships – particularly in DC plans – are complex and often have competing goals. The shift in the US retirement market from DB to DC has increased both the intricacies of stakeholder relationships and the associated agency problems.

In a DC plan, the plan sponsor remains the key decision maker within the stakeholder chain. It defines the plan structure and features, selects and monitors investments, and tracks beneficiaries’ use. Consultants and investment managers act as service providers and influencers, responding most directly to plan sponsor requests. However, decision making – including many of those related to ESG – has shifted to plan beneficiaries who now have more power to drive change in the behavior of the plan sponsors, consultants, and managers.

Given the headwinds regarding US policy and regulation around ESG issues, successful strategies for increasing ESG incorporation within ERISA plans are more likely to stem from stakeholder and collaborative initiatives. Given also the shift to DC plans, progress on expanding the incorporation of ESG factors in the immediate future needs to shift to DC-based strategies and stakeholders, including specific beneficiary-oriented recommendations.

Some tactical steps for plan sponsors include:

- Making explicit links between corporate values, CSR, and talent management on the one hand, and retirement benefit provision on the other, by incorporating ESG options into DB and DC investments. Corporate plan sponsors that are signatories of the UN Global Compact, for example, should find it easy to make this connection.

- Establishing best-practice ESG governance through:

- Developing investment beliefs that address ESG incorporation;

- Ensuring that investment consultants have ESG expertise by including selection criteria and questions in consultant RFPs;

- Updating Investment Policy Statements to require ESG analysis when selecting and monitoring investments;

- Requiring investment consultants to ask investment managers how they incorporate ESG;

- Selecting a recordkeeper with ESG products on its platform;

- Requiring investment consultants to include ESG analysis in all performance and monitoring reports; and

- Providing education to DC beneficiaries so they understand what it means to incorporate ESG factors into investments and whether options are included in the core line-up.

- Creating beneficiary-oriented ESG surveys – framed around alignment with corporate values – to assess demand for ESG options in DC plans and to stimulate action by plan sponsors. Survey results would likely lay the groundwork for advice providers/engines, investment managers and consultants to facilitate ESG fund inclusion and actual use.

- Piloting the use of ESG-oriented preferences in independent advice provider/engines to address a key constraint limiting ESG fund use. Plan beneficiaries need advice providers and algorithms that ask about ESG preferences, and which then can lead to asset allocations that include ESG funds.

- Promoting the standardization of ESG disclosure requirements for investment managers and consultants, including a push for transparency of ESG products. These types of initiatives need to avoid ESG industry jargon and focus on the ultimate user: plan beneficiaries.

- Joining industry initiatives, such as the World Business Council for Sustainable Development’s Aligning Retirement Assets project and the Defined Contribution Institutional Investment Association ESG Subcommittee, to improve collaboration between plan sponsors and service providers and tap economies of scale.

Policy to clarify, not drive, ESG incorporation

Despite the secondary role that policy directives are expected to play in driving ESG incorporation in the US, the provision by the DOL of some clarity for fiduciaries on the definitions and taxonomy of ESG factors would create a firmer basis for plan sponsors to continue incorporating ESG into their plans. Given the increased dominance of DC plans in the market, policies that would better inform the plan beneficiaries and protect the interests of individual US workers are also needed. These could include clarity on default investment alternatives and clearer guidance on how fiduciaries can best further the interests of plan beneficiaries.

Shifting the focus to individual investors from institutional players

The US pension system needs to be viewed more holistically, broadening from a policy-centric focus to include a stakeholder approach to the ERISA market. The primary emphasis shifts from institutional actors to looking at how individual beneficiaries structure their retirement investment decisions. This will include bottom-up approaches centered on plan beneficiaries, as well as top-down initiatives with plan sponsors. While the path to driving ESG incorporation for DB plans is clearer and depends primarily on the actions of institutional players, the future growth of ESG incorporation will largely depend on the individual choices of DC plan beneficiaries. Continued growth of ESG in the US will require ESG to be embedded throughout the stakeholder chain.

Untangling stakeholders for broader impact: ERISA plans and ESG incorporation

- 1

- 2

- 3

- 4

- 5

- 6

Currently reading

Currently readingStrategies and recommendations