By Daniel Garrett, The Wharton School of the University of Pennsylvania; and Ivan Ivanov, Federal Reserve Bank of Chicago

A variety of environmental, social and governance (ESG) policies have proliferated at financial institutions, ranging from support for employee abortion rights to limits on firearm sales to emissions targets, and the movement of capital associated with these policies has garnered significant attention in capital markets and academic literature.

In response, many states in the US have proposed or passed legislation that limits financial institutions with certain ESG policies from participating in public finance markets. Some states limit the type of financial products local public entities are allowed to purchase. Others simply ban financial services firms with such policies from servicing public or municipal clients.

Meanwhile, these institutions maintain that their ESG positions are based on “ordinary business reasons”, following risk-based frameworks.

In our research paper, we study how regulation limiting ESG policies by financial institutions distorts financial market outcomes.

Large municipal bond underwriters decreasing

In September 2021, Texas barred local municipalities from contracting with banks with certain environmental and firearms policies by enacting two laws – Senate Bills 13 and 19. We use underwriting data from January 2017 through April 2022 to show that the Texas laws led to the abrupt exit of at least five of the most prominent municipal bond underwriters from the state’s public finance market – Citigroup, JP Morgan, Goldman Sachs, Bank of America, and Fidelity. These banks underwrite many of the largest municipal bond issues inside and outside of Texas.

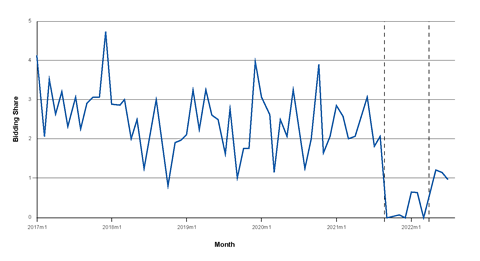

Figure 1: Competitive market share of targeted banks

Texas and its political subdivisions seek roughly US$50 billion in financing through the municipal bond market per year, placing it in the top three states by issuance in the US for the last three years. Prior research reveals that Texas is a competitive market. Figure 1 shows how the competitive bidding share among the five targeted banks changed over time. Before the anti-ESG laws, the five banks made up just over a quarter of bidding volume in Texas, but this share drops to zero immediately following the enactment of the laws.

As the graph indicates, it was not obvious before September that any institutions would leave Texas over these laws, partially because of the speed with which the laws went through the legislative process. Each institution was given a choice: change or renounce the ESG policies targeted by the Texas laws, or lose access to the Texas public finance market. During the first eight months since the laws were enacted, we estimate that these banks lost between US$54 million and US$95 million in underwriting profits by giving up their municipal underwriting business in the state.

Our paper examines the impact of the Texas laws on the municipal bond market in the state during the first eight months after law enactment. Using the varying exposure of government issuers to the targeted banks, we measure the impacts of these laws on borrowing outcomes.

A change of strategy

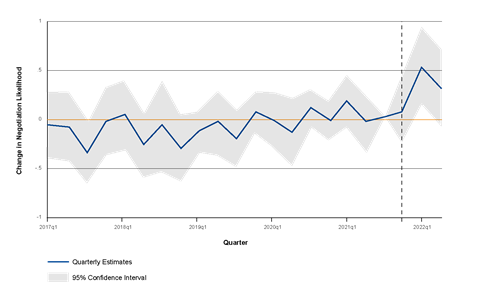

Municipal bond issuers may be able to mitigate the impact of the Texas laws by changing the way they bring bonds to market. Issuers can either hold a competitive auction, where different underwriters bid on the bond offering, with the lowest yield-to-maturity bid winning the auction, or negotiate the bond offering directly with an underwriter. Negotiated sales allow underwriters to better place the issue with investors when market or issue uncertainty is high. We find that issuers that rely heavily on the targeted banks opt into negotiations to soften the perceived large volatility in the auction market. Figure 2 shows this shift in placement type over time.

Figure 2: Change in likelihood of negotiation

By comparing the most and least affected borrowers in Texas over several years before the laws were enacted, we can verify that these two groups of borrowers have not historically been different from each other. However, after the enactment of the anti-ESG laws, the most affected borrowers experience a large change in uncertainty that manifests as an economically important move away from competitive sales.

Despite the adjustment in borrower behaviour, borrowing costs for issuers in Texas still increase by approximately 10 basis points after the enactment of the laws, with an additional standard deviation (24%) in reliance on the targeted banks. This empirical pattern is true whether we compare them to peer borrowers in Texas, outside of Texas, or a synthetically created group of observably identical issuers.

This increase in yields translates to an additional US$300 million to US$500 million in borrowing costs on the US$31.8 billion in municipal bond issuance during the first eight months following enactment of the laws.

We provide evidence of several mechanisms behind this substantial increase in costs. First, moving to a negotiated sale can cost slightly more than a competitive sale on average. Second, the bonds are placed with investors through a larger number of smaller trades, which can indicate higher costs of intermediation. Third, as potential underwriters are removed from the market, the remaining underwriters are able to consolidate their market power, and competition in the market may decline.

To quantify the first two mechanisms, we use a calibration of cost estimates from prior literature and from conditional average dealing costs for each underwriter. Our estimates suggest these mechanisms explain less than 20% of the increased costs for Texas borrowers. When exploring the third mechanism, we study the remaining auction sales in the market. Affected borrowers have large decreases in the number of participating bidders and a sizable increase in the variance of submitted bids – consistent with decreasing competition and increasing markups.

What we learned from the Texas anti-ESG experience

It is challenging to reliably establish the associated long-run effects of the Texas experience with anti-ESG laws. We note in Figure 1 that the targeted banks re-entered the Texas market in a more limited manner starting in May 2022, and, consequently, we are unable to conclusively establish whether the state of Texas or the financial institutions changed behaviour, or what would have happened if the banks had not re-entered.

However, several lessons are clear. First, banks value their ESG policies and chose to leave the Texas public finance market instead of abandoning ESG policies. Second, political subdivisions in Texas faced large uncertainty in the months following the enactment of these laws and moved away from competitive sales to negotiations. Finally, borrowers in Texas paid significantly more for external finance during this period than their counterparts outside of Texas.

These economic forces suggest that even in states with historically competitive public finance markets, the loss of competition from anti-ESG laws and the resulting adverse effect on borrowing costs may be significant.

This paper was presented at the PRI Academic Network Week 2022.

The PRI’s academic blog aims to bring investors insights from the latest academic research on responsible investment. It is written by academic guest contributors. Blog authors write in their individual capacity – posts do not necessarily represent a PRI view.