This report summarises the outcomes of the Investor Initiative for Sustainable Forests (IISF). The partnership between the PRI and Ceres aimed to tackle commodity-driven deforestation within cattle and soybean supply chains at investee companies. We did this by coordinating an action-driven coalition of 44 investors with US$6.8trn in assets under management.

We also wanted to address ESG issues related to soft commodity production, such as poor working conditions, land rights and impact on indigenous peoples.

The engagement tracked investee companies’ policies, implementation, disclosure and performance on deforestation-related practices each year between 2017 and 2020, and the results are presented in this document. This report also sets out recommendations for continuing stewardship activities in this area.

To view the full report, including an appendix of benchmark indicators that we used to score companies, download the PDF version.

Why tackle commodity-driven deforestation?

Forests are essential to the planet’s ability to regulate climate and water cycles, host biodiversity, prevent soil erosion, and directly sustain the lives of 1.3 billion people. Deforestation is often linked to human rights abuses, such as land grabbing and modern slavery.

Agricultural expansion accounts for 80% of deforestation worldwide. The World Resources Institute’s Global Forest Review identified cattle, palm oil and soy as the commodities most likely to replace forested land between 2001 and 2015. Cattle pasture occupied 45.1 million hectares (Mha) of deforested land, accounting for 36% of agriculture-related tree cover loss. Oil palm (the area that the oil palm trees occupy) ranked second (10.5 Mha), followed by soy (8.2 Mha).

The State of the World’s Forests report, written by the Food and Agriculture Organization of the United Nations, highlights that deforestation is continuing at alarming rates, although with marked regional differences. Continued investor action is crucial to ensure commodity production is decoupled from environmental degradation and human rights abuses.

IISF Objectives and Company asks

The IISF’s overall objectives were to:

- Improve transparency and quality of disclosure on the source and materiality of certain commodities, and how they move through the supply chain;

- Achieve full commitment by companies to eliminate deforestation and human rights violations throughout the entire supply chain;

- Improve traceability and supplier verification approaches for deforestation-risk commodities throughout the supply chain; and,

- Encourage collaboration to develop standards, policies, certifications, and/or tools to facilitate deforestation-free supply chains.

More specifically, companies across cattle and soy value chains were asked by investors to improve their practices in four key areas:

- Policy: A publicly-disclosed, commodity-specific deforestation policy with a quantifiable, time-bound commitment covering the entire supply chain and sourcing geographies.

- Traceability: A traceability commitment that is time-bound, quantifiable and covers direct and indirect suppliers, tracking the percentage of commodity procurement that is traceable to product origin.

- Supplier assurance: A publicly disclosed process for monitoring and verifying supplier compliance with their no-deforestation policy and a clear process for non-compliant suppliers.

- Disclosure: Public disclosure of the percentage of commodity sourced in line with their no-deforestation policy.

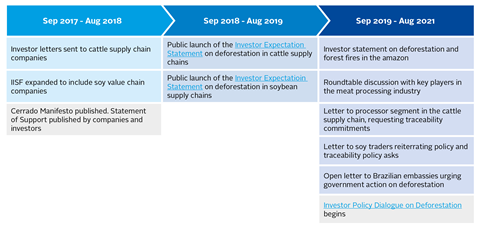

A brief timeline of the IISF

The diagram below summarises key IISF milestones, with blue boxes showing IISF-led actions, and grey boxes representing significant external events.

Methodology

A total of 44 investors engaged with 43 companies (for each company there was at least one lead investor) across the cattle and soybean value chains.1 Various segments of the supply chain were engaged, including consumer goods / staples (10), clothing and apparel (2), retail / food service (19), as well as traders and processors (12). The geographic focus of the engagement was primarily Latin America and specifically Brazil, due to its key role in commodity-driven deforestation.

To assess company progress, benchmark studies were conducted by consultants Aidenvironment each year between 2017 and 2020. Company practices were assessed across four categories: (1) policy and strategy, (2) implementation, (3) disclosure and (4) performance. The latest full set of benchmark indicators is included in the appendix in the PDF version of this report.

We assessed overall progress using 2017-2020 data for the 37 companies which were engaged throughout. Additional companies were added and others removed throughout the IISF – these companies were not included.

To assess progress on specific engagement objectives, a selection of indicators per category were analysed. Aidenvironment scored companies through a systematic approach, based on publicly available information, including all relevant policy documents, annual and sustainability reports, progress reports and sustainability dashboards, press releases and news items. The consultants checked consistency through targeted Google searches, membership lists of relevant multi-stakeholder initiatives and company scores across other appropriate benchmarks.

The IISF project was expanded in its first year to include soy as well as cattle supply chain companies, and the benchmark indicators were also changed. Therefore, only benchmark data from 2018 onwards was used to indicate progress on individual indicators, but we are using 2017 data for average company scores. Scores should be taken as a general snapshot of company performance.

Attributing change in company behaviour to investor engagement is extremely difficult and we do not attempt to do so. This is due to the complexity of deforestation, and the challenge of linking investor engagement to specific corporate actions when there are multiple pressures on companies (e.g., market dynamics, consumer awareness, changes in legislation etc.). Results are nonetheless presented as a proxy or indication of progress in those companies that were engaged.2

Overall Results

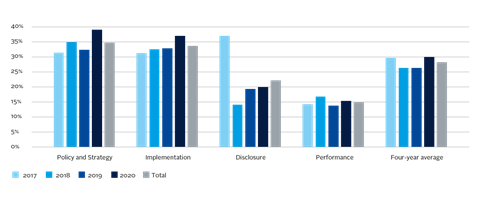

At the overall and individual category level (policy and strategy, implementation, disclosure, performance), only very modest improvements were noted. Between 2017 and 2020, improvements in company scores were mainly attributed to improvements in policy and strategy (32% to 40%) and implementation scores (32% to 37%). Performance saw the smallest increase in scores, from 14% to 15% over the same period. Disclosure also saw some improvement (14% to 20% between 2018 and 20203).

These overall findings align with the worsening situation we have witnessed, with primary rainforest destruction increasing by 12% from 2019 to 2020, and Brazil seeing the highest levels of primary forest loss of any country globally, with a total loss of 1.7 million hectares.4

While disappointing, engagement should not be seen as futile. Rather, deforestation is a complex, systemic issue which merits more sophisticated stewardship strategies that focus on real-world outcomes (see the Insights and Recommendations sections).

Figure 1: Average company scores over the four categories between 2017 and 2020

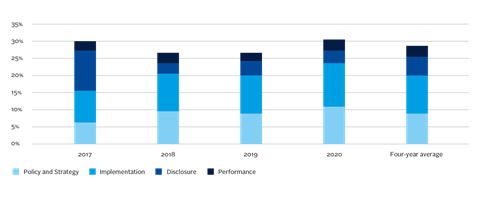

Figure 2: Average company scores: How much did each category contribute to the total?

Findings by Engagement Objective

Objective 1: Policy and strategy

The initiative’s first ask was for companies to adopt a publicly-disclosed, commodity-specific deforestation policy with a quantifiable, time-bound commitment covering the entire supply chain and sourcing geographies.

The following indicators were selected to assess this objective:

| Indicators | Max Score | Scoring Explanations |

|---|---|---|

|

Presence of a commodity-specific policy outlining approach to achieving a deforestation-free supply chain |

1 |

1 = commodity-specific policy, or generic policy with soy, beef or leather as a priority commodity 0.5 = generic, non-commodity-specific, or other commodities prioritised 0 = no policy |

|

Policy outlines time-bound, quantifiable commitments to achieve a deforestation-free supply chain |

1 |

1 = commitment that is time-bound and quantifiable 0.5 = unquantifiable, generic commitment 0 = no commitment |

|

Deforestation policy requires companies to go beyond legal compliance |

1 |

1 = yes 0.5 = pilots / initiatives that go beyond legal compliance 0 = no |

|

Evidence of progress achieved against public commitments, reported with an established frequency |

1 |

1 = progress reported with established frequency 0.5 = progress reported ad hoc 0 = no progress reported |

Table 1: Average Policy and Strategy indicator scores 2018-2020

| Year | 0 | 0.5 | 1 |

|---|---|---|---|

|

Presence of a commodity-specific policy outlining approach to achieving a deforestation-free supply chain |

|||

|

2018 |

19% |

33% |

48% |

|

2019 |

19% |

38% |

43% |

|

2020 |

16% |

27% |

57% |

|

Policy outlines time-bound, quantifiable commitments to achieve a deforestation-free supply chain |

|||

|

2018 |

48% |

4% |

48% |

|

2019 |

46% |

19% |

35% |

|

2020 |

30% |

32% |

38% |

|

Deforestation policy requires companies to go beyond legal compliance |

|||

|

2018 |

93% |

0% |

7% |

|

2019 |

81% |

16% |

3% |

|

2020 |

76% |

19% |

5% |

|

Evidence of progress achieved against public commitments, reported with an established frequency |

|||

|

2018 |

70% |

4% |

26% |

|

2019 |

62% |

14% |

24% |

|

2020 |

57% |

19% |

24% |

There has been a slight (+9%) increase in companies that have a commodity-specific deforestation policy, while the number of companies with no policy has decreased very slightly (-3%).

Overall, the percentage of companies without a time-bound deforestation policy or commitment decreased (from 48% to 30%). Despite this, it seems new commitments were generally not quantifiable and time-bound, with those scoring 0.5 (i.e., not fully meeting requirements) increasing by 28% and those scoring full marks for time-bound, quantifiable policies decreasing from 48% to 38%.

The traders, processors and producers segment saw the largest percentage increase in companies that have a deforestation policy (those scoring 0 on this indicator decreased from 71% in 2018 to 30% in 2020). However, as of 2020, a high percentage of companies in this segment (40%) still have commitments that are either non-quantifiable or non-time-bound, reflecting the overall trend.

Table 2: Policy outlines time-bound, quantifiable commitments to achieve a deforestation-free supply chain – by sector

| Sector / Year | 0 | 0.5 | 1 |

|---|---|---|---|

|

Consumer Goods / Clothing & Apparel |

|||

|

2018 |

30% |

10% |

60% |

|

2019 |

33% |

17% |

50% |

|

2020 |

25% |

33% |

42% |

|

Retail / Food Service |

|||

|

2018 |

50% |

0% |

50% |

|

2019 |

53% |

13% |

33% |

|

2020 |

33% |

27% |

40% |

|

Traders / Processors / Producers |

|||

|

2018 |

71% |

0% |

29% |

|

2019 |

50% |

30% |

20% |

|

2020 |

30% |

40% |

30% |

Objective 2: Traceability

The second company ask was for a traceability commitment that is time-bound, quantifiable and covers direct and indirect suppliers, tracking the percentage of commodity procurement that is traceable to product origin.

The following indicators were selected to assess this objective:

| Indicators | Max scores | Scoring Explanations |

|---|---|---|

|

Evidence of traceability commitment that is time-bound, quantifiable, and covers the entire supply chain |

1 |

1 = yes 0 = no |

|

Percentage of commodity procurement that is traceable to origin |

100% |

Table 3: Evidence of traceability commitment that is time-bound, quantifiable, and covers the entire supply chain – all companies

| Year | 0 | 0.5 | 1 |

|---|---|---|---|

|

2018 |

85% |

7% |

7% |

|

2019 |

73% |

24% |

3% |

|

2020 |

68% |

24% |

8% |

Uptake of traceability commitments that are time-bound, quantifiable and cover the entire supply chains is slow. While the percentage of companies that have some form of commitment increased by 17%, most companies (68% in 2020) still lack any form of traceability commitment. Only 8% of companies benchmarked scored full points on this indicator in 2020 (up 1% from 2018).

Table 4: Evidence of traceability commitment that is time-bound, quantifiable, and covers the entire supply chain – by sector

| Sector / Year | 0 | 0.5 | 1 |

|---|---|---|---|

|

Consumer Goods / Clothing & Apparel |

|||

|

2018 |

90% |

0% |

10% |

|

2019 |

92% |

0% |

8% |

|

2020 |

75% |

8% |

17% |

|

Retail / Food Service |

|||

|

2018 |

80% |

10% |

10% |

|

2019 |

73% |

27% |

0% |

|

2020 |

87% |

13% |

0% |

|

Traders / Processors/ Producers |

|||

|

2018 |

86% |

14% |

0% |

|

2019 |

50% |

50% |

0% |

|

2020 |

30% |

60% |

10% |

The traders, processors, producers segment saw the largest improvement in this area. In 2018, 86% of companies in this segment had no traceability commitments, while now the majority (70%) have a traceability commitment – but only 10% of these meet all requirements (time-bound, quantifiable, covering both direct and indirect suppliers).

The consumer goods segment saw some small improvements, with those scoring 0 decreasing by 15%, and 17% of companies in this sector achieving full scores. Retail / food services saw a backslide in commitments, with the latest benchmark showing zero companies have adequate commitments and 87% have no traceability commitments.

Table 5: Percentage of commodity procurement that is traceable to origin

|

2018 |

16% |

|

2019 |

12% |

|

2020 |

14% |

The percentage of commodity procurement that is traceable to origin remains low and has experienced some backsliding.

Objective 3: Supplier assurance

The third company ask was for apublicly disclosed process for monitoring and verifying supplier compliance with their no-deforestation policy and a clear process for non-compliant suppliers.

The following indicators were selected to assess this objective:

| Indicators | Max Scores | Score Explanations |

|---|---|---|

|

Evidence of internal monitoring / verification of direct (tier 1) suppliers across all geographies |

1 |

1 = all geographies 0.5 = restricted to Amazon biome 0 = no evidence |

|

Evidence of internal monitoring / verification of indirect (tier 2 and beyond) suppliers across all geographies |

1 |

1 = tier 2 and beyond 0.5 = tier 2 only partially verified 0 = nothing beyond tier 1 |

|

Company’s verification of suppliers is conducted by a third party, and third-party verification reports are publicly available |

1 |

1 = yes 0.5 = partially 0 = no |

|

The percentage of commodity suppliers that comply with company’s deforestation policy |

100% |

Table 6: Evidence of internal monitoring / verification of direct (tier 1) suppliers across geographies - all companies

| Year | 0 | 0.5 | 1 |

|---|---|---|---|

|

2018 |

70% |

7% |

22% |

|

2019 |

51% |

24% |

24% |

|

2020 |

46% |

27% |

27% |

In 2020, most companies (54%) monitored tier 1 suppliers in some form. The number of companies conducting partial monitoring of their supply chains has increased by 20%, while those conducting fully satisfactory monitoring activities have increased by 5% since 2018. The number of companies not monitoring tier 1 suppliers has decreased by 24% since 2018, from 70% to 46%.

Table 7: Evidence of internal monitoring / verification of direct (tier 1) suppliers across geographies - by sector

| Sector / Year | 0 | 0.5 | 1 |

|---|---|---|---|

|

Consumer Goods / Clothing & Apparel |

|||

|

2018 |

70% |

0% |

30% |

|

2019 |

58% |

17% |

25% |

|

2020 |

58% |

17% |

25% |

|

Retail / Food Service |

|||

|

2018 |

80% |

0% |

20% |

|

2019 |

60% |

33% |

7% |

|

2020 |

60% |

33% |

7% |

|

Traders / Processors / Producers |

|||

|

2018 |

57% |

29% |

14% |

|

2019 |

30% |

20% |

50% |

|

2020 |

10% |

30% |

60% |

The traders, processors and producers segment saw the highest scores in this area. Those receiving full marks for this indicator amounted to just 14% in 2018, with an increase to 60% in 2020. Those scoring zero reduced from 57% to 10%. The retailers and consumer goods segments are lagging, with 7% and 25% having adequate practices respectively.

Table 8: Evidence of internal monitoring / verification of indirect (tier 2 and beyond) suppliers across geographies - all companies

| Year | 0 | 0.5 | 1 |

|---|---|---|---|

|

2018 |

89% |

0% |

11% |

|

2019 |

84% |

8% |

8% |

|

2020 |

65% |

24% |

11% |

Evidence of internal monitoring and verification of tier 2 suppliers is lower than for tier 1. Full scores were only achieved by 11% of companies, which is the same proportion as in 2018. There was only a slight decrease in those scoring zero, from 89% in 2018 to 65% in 2020. Traders also seem to fare better in this area, although only 2% have practices that fully meet the requirements for this indicator.

Those taking up third-party verification are a small proportion of the whole group (16%). Between 2018 and 2020 there was just a 1% increase in those who do this consistently for their entire supply chain, and a 15% increase in those who only use third-party verification for part of their supply chain.

Again, despite slight improvements in implementation practices, performance scores remained low. The percentage of suppliers complying with the company’s deforestation policy remains low, with an average of 14% (a 2% increase compared to 2018).

Objective 4: Disclosure

The fourth company ask was public disclosure of the percentage of commodity sourced in line with their no-deforestation policy.

The following indicators were selected to assess this objective:

| Indicators | Max Score | Score Explanations |

|---|---|---|

|

Company discloses the percentage of its soy, beef or leather produced or purchased that adheres to the company’s deforestation policy |

1 |

Partial scores assigned where disclosure does not apply to full supply chain |

|

The percentage of commodity (soy, beef or leather) procurement that complies with the company’s deforestation policy |

100% |

Table 9: Company discloses the percentage of its soy, beef or leather produced or purchased that adheres to the company’s deforestation policy – all companies

| Year | 0 | 0.5 | 1 |

|---|---|---|---|

|

2018 |

81% |

0% |

19% |

|

2019 |

81% |

8% |

11% |

|

2020 |

70% |

11% |

19% |

There were no significant improvements regarding the proportion of companies disclosing the percentage of deforestation-risk commodities produced or purchased that adhered to their deforestation policy. There was a slight decrease in companies that scored zero (meaning those who did not disclose at all).

Table 10: Average percentage of commodity procurement that complies with its deforestation policy – by sector

| Sector / Year | Average Score |

|---|---|

|

Consumer Goods / Clothing & Apparel |

|

|

2018 |

16% |

|

2019 |

16% |

|

2020 |

29% |

|

Retail / Food Service |

|

|

2018 |

13% |

|

2019 |

5% |

|

2020 |

9% |

|

Traders / Processors / Producers |

|

|

2018 |

18% |

|

2019 |

4% |

|

2020 |

31% |

Unsurprisingly, the average percentage of commodities in compliance with deforestation policies also did not increase by much. It was 21% in 2020, up 6% from 2018. Traders had the highest score in 2020 at 31%, while retail fell back from 13% to 9% between 2018 and 2020.

Insights

Companies made some progress on commitments, policies and implementation. However, performance is lagging.

Since the IISF was launched in 2017, companies have made some progress in updating and improving their existing deforestation commitments. Some have made new commitments to full traceability and to ending deforestation within their supply chain.

Despite this, the alarming increase in deforestation rates globally over the course of the engagement, particularly in Brazil, highlight that there is a mismatch between companies’ policies, their implementation, and actual reduction of deforestation. This conflict reflects the complexities of deforestation, including its multiple drivers and the multi-stakeholder alignment and coordination required to tackle it, as well as the need for more strategic and forceful stewardship.

There are significant challenges (and therefore potential levers) for investors tackling deforestation, including:

- Political environment. While Brazil has historically had a strong policy framework for safeguarding its forests, including specific institutions monitoring data and developments in this area, enforcement of conservation policies remains weak,5 and more recently it was announced that deforestation will no longer be tracked in the Cerrado. Political support would facilitate better traceability solutions, which are a key lever to better understanding deforestation.6 Brazil’s volatile political climate during IISF activities has been a key challenge for identifying and encouraging deforestation solutions.

- Traceability and data. Company disclosures on sourcing forest-risk commodities are limited. While this is a challenge for investors, methodologies are available for estimating and qualifying deforestation risk.7 Collaborative projects are emerging to help make the best use of available tools and datasets. One example is the Aligned Accountability project, a partnership between Global Canopy, the Zoological Society of London, Trase and the Accountability Framework Initiative, which will collect the best available open data on company performance on deforestation risks in commodity supply chains and create standardised common metrics.

- Supply chain dynamics and complexity. Cattle and soy supply chains are complex (i.e., spanning several continents, multiple segments and stakeholders, and generally not vertically integrated) and have been historically difficult for investors to engage with. Supply chain complexity means it is harder to prevent unsustainable goods being sold. During the engagement, we found that investors would have benefitted from more knowledge of the investee companies that were engaged, including on the geographies where they were based. Where supply chain segments were particularly fragmented, it was hard to engage all relevant companies, especially where they were smaller and / or not publicly listed. Where companies were listed and the supply chain segment was concentrated, at times it was hard for investors to have sufficient influence on companies, due to only holding a small proportion of shares.

Deforestation is a systemic issue –and systems approaches to stewardship are needed to tackle it.

Deforestation has the potential to disrupt the ecological cycles on which society and companies depend. Disruption to ecosystem services provided by the Amazon rainforest, such as the water cycle, climate regulation and protection from disease, has and will continue to have tremendous impacts across multiple companies, supply chains, sectors, markets and economies. As such, deforestation affects investor portfolios beyond narrow definitions of direct exposure. But investors should not be deterred from engaging on deforestation. On the contrary, because of the complexity of the issue, it will be important to incorporate learning from this engagement and other experiences to ensure that future stewardship efforts are more effective and impactful.

Many investors understand this and some are already putting this systemic approach to stewardship into practice with regards to deforestation. Promising developments included:

- Supporting the Cerrado Manifesto. Many investors signed the Cerrado Manifesto Statement of Support8 and some became involved in the steering committee. This group has been pushing for a biome-wide solution to address deforestation, engaging with multiple industry bodies and other stakeholders.

- Initiating policy dialogue. Investors have started to engage with governments through the Investor Policy Dialogue on Deforestation (IPDD), urging them to demonstrate clear commitment to eliminating deforestation.

- Using escalation tools beyond dialogue. Members of the IISF successfully filed a shareholder proposal for Bunge, a food production company, to strengthen its no-deforestation policies. After being endorsed by the company’s board of directors, it was favourably voted upon by 98% of shareholders.9 A similar proposal at ADM achieved an improved commitment from the company, secured in exchange for a withdrawal of the proposal.10

The following are recommendations for continued investor action on deforestation, based on learnings from the IISF. These are not prescriptive, but rather suggestions for how investors can build upon the work of IISF members:

1. Continue pushing for commitments to halt deforestation, with full traceability as a key lever to change company practices.

Encouraging full traceability of commodities to origin will be an important lever in halting deforestation, due to the importance of better understanding where deforestation is happening and which actors are involved. Traceability is also important from a human rights perspective (e.g., identifying labour rights abuses and land grabbing11). New or upcoming due diligence regulations in the UK, EU and the US will also likely intensify the need for better traceability data and tools. Stakeholders in industry, academia and affected communities are initiating projects to improve investors’ ability to access this data.

2. Prepare to escalate when policies do not translate into action and outcomes on the ground. Results for this engagement show that commitments and policies are not enough to make a difference to overall deforestation rates. If investors want to tackle deforestation, it is crucial to focus on influencing positive, real-world outcomes. Should investors not see results, then they should be prepared to use the full range of stewardship tools available to them beyond company dialogue, including filing and voting on shareholder resolutions, applying public pressure tactics and reviewing the role of board members of the companies in question.

3. Multi-stakeholder action is key to tackling deforestation. Collaboration across sectors and supply chains should be a key feature of future stewardship initiatives.

Investors can engage with a broader range of stakeholders through company dialogues with key actors (e.g., banks), by joining policy engagement efforts such as the IPDD, supporting multi-stakeholder initiatives such as the Statement of Support for the Cerrado Manifesto, and collaborating across different supply chains to learn from positive experiences with tools such as certification and / or biome-wide private sector agreements.

4. Integrate interconnected ESG issues into future stewardship activity on deforestation. Deforestation is a systemic issue, and therefore some key levers for action lie beyond the ‘E’ in ESG. Paying living wages can reduce smallholder deforestation,12 for example, and indigenous land rights are a key driver of forest conservation in Brazil.13 It is important to also consider the drivers behind deforestation, such as unsustainable consumption of forest-risk commodities.14 Action in consuming markets should be a feature of any future engagement on deforestation. As any new stewardship strategy is developed, it will be important to consider unintended impacts on, or synergies with, areas for action such as biodiversity, climate, circular economy and other ESG issues.

Individual actions from investors and companies will only have a limited impact. Collaboration is essential to increase supply chain transparency and tackle deforestation.

Next steps

The PRI continues to work on the issue of sustainable commodities and deforestation. For example, we will be producing a document on the results of our sustainable palm oil collaborative engagement. Find out more on our Sustainable Land Use page. Collaborative engagement on deforestation will be relaunched shortly. In addition, investors should also look to be involved in other deforestation initiatives, in particular the IPDD.

Downloads

Investor Initiative for Sustainable Forests - Engagement Results

PDF, Size 5.02 mb

References

1 Of the 43 companies engaged, 13 were exposed to the cattle supply chain only, 16 to the soy supply chain only, and 14 to both

2 Please note: where table rows do not add up to 100%, this is due to decimal rounding in Excel

3 2017 had an average disclosure score of 38%, however this was most likely due to the difference in scoring methodologies

4 Global Forest Watch (2021), Primary Rainforest Destruction Increased 12% from 2019 to 2020

5 WWF (2015), Brazil’s New Forest Code: A guide for decision-makers in supply chains and governments

6 Brazilian Coalition on climate, forests and agriculture (2020), Beef Chain Traceability in Brazil - Challenges and Opportunities

7 KLP, Storebrand and Rainforest Foundation Norway (2020), Deforestation tools assessment and gap analysis: How investors can manage deforestation risk

8 For a full list, see this link

9 Chain Reaction Research (2021), The Chain: Recent Shareholder Votes on Deforestation Reflect Greater Investor Pressure to Reduce Forest Loss

10 Green Century Funds (2021), ADM* Strengthens No-Deforestation Policy, Following Green Century Shareholder Proposal

11 PRI (2020), From farm to table: ensuring fair labour practices in agricultural supply chains

12 See the World Conservation Society’s ‘Forest First’ Approach

13 Baragwanath and Bayi (2020), Collective property rights reduce deforestation in the Brazilian Amazon

14 CarbonBrief (2021), Scientists calculate trade-related ‘deforestation footprint’ of rich countries