Case study by Pendal Group (formerly BT Investment Management)

| Contributor | George Bishay, Portfolio Manager, Pendal Group Limited (formerly BT Investment Management) |

|---|---|

|

Market participant type |

Asset manager |

|

Total AUM |

US$76.2 billion (as of 31/03/2018) |

|

Fixed income AUM |

US$13.9 billion (as of 31/03/2018) |

|

Operating country: |

Australia |

|

Case study focus: |

Example of how S factors affect credit risk assessment |

Background to the investment case

Coca Cola Amatil (CCL) is one of Asia-Pacific’s largest bottlers and distributors of alcoholic and non-alcoholic beverages. The majority of its products are non-alcoholic and high in sugar. For many years, Pendal Group Limited (Pendal) has held concerns regarding headwinds from structural shifts in consumer demand for healthier options and regulatory risks relating to sugar consumption and their associated impacts on corporate profitability. Pendal has held an underweight position in CCL across its Australian fixed income funds for a number of years, given these concerns.

ESG factor which drove in the investment decision

Pendal’s position on the company reflects its view that the social risks around high sugar and its links to diabetes and obesity have not been priced in to the issuer’s credit spread and hence Pendal expected CCL’s credit spreads to underperform over time. There are also regulatory risks surrounding potential imposition of sugar taxes in key markets. From a financial perspective, CCL’s credit spreads have been tight and, in Pendal’s view, have not factored in social risks relative to similarly rated issuers.

Pendal’s credit analysis process incorporates fundamental issuer analysis and proprietary quantitative modelling to assess investment opportunities. In particular, the credit selection framework focuses on four categories:

1. Business profile (such as competitive position and quality of management);

2. Financial profile (such as cash flow metrics and debt maturity schedules);

3. Risk factors (including regulation and funding sources); and

4. Valuation factors (such as relative value, technical and covenants strength).

ESG factors are typically captured in the business profile and risk factors categories.

Pendal’s credit selection framework is based on an integrated credit research approach that includes considering its equity team’s research as well as internal and external ESG research. Pendal’s issuer research is significantly enhanced through collaboration with its equity teams to obtain insights from their investment analysis and direct company engagements, as well as discussions with Pendal’s head of responsible investments regarding ESG issues that are deemed material to the issuer being reviewed. This broadened research approach promotes a more dynamic process with greater awareness of market conditions.

Another avenue through which ESG factors are incorporated is through explicit sustainability (best of sector) and ethical screens that are applied across Pendal’s dedicated sustainability fixed income funds. For these strategies, each credit issuer is rated on a comprehensive set of ESG categories. Issuers with ESG scores that do not meet the quality threshold are excluded from the fund’s investable universe. In this case, CCL’s poor ESG rating excluded the issuer from the investable universe of Pendal’s dedicated sustainability strategies even before the bottom-up credit selection process outlined above was applied.

Both the credit selection process (applied across all of Pendal’s income and fixed interest funds) and the dedicated sustainability screening process incorporate internal and external sources of ESG information. The third-party ESG data providers conduct in-depth analysis of issuers’ (CCL in this example) non-financial characteristics and risks using their independent ESG research.

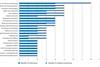

Market implications

As can be seen from the chart below, CCL credit spreads underperformed against similar consumer sector peers in 2017 and into 2018 as social trends changed and competition intensified (see figure below).

In April 2017, the soft drink bottler issued a profit warning based on volume and price pressures as its core high-sugar products have struggled with dwindling demand. Pendal’s investment case was further reinforced in March 2018 after CCL was downgraded from BBB+ to BBB by Fitch, reflecting continued deterioration in the performance of the company’s Australian business due to structural challenges (falling demand for carbonated soft drinks) and increased competition in still beverages. CCL’s credit spreads have continued to underperform since this latest credit rating downgrade.

Key takeaways

Pendal’s bearish view of CCL and the issuer’s ongoing underperformance reinforced its own core investment philosophy that a company’s approach to managing ESG issues can provide valuable insight into its exposure to negative incidents and that value can be added through incorporating ESG factors into the credit selection process. In particular, the above case study is an example of how ESG considerations can be a source of risk mitigation in fixed income investing. Material ESG risks should be factored into credit valuations, otherwise investors can be exposed to negative events (such as a credit rating downgrade) and their investments could subsequently underperform the market.

Download the full report

-

Shifting perceptions: ESG, credit risk and ratings – part 2: exploring the disconnects

June 2018

ESG, credit risk and ratings: part 2 - exploring the disconnects

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

Currently reading

Currently readingCase study: Coca Cola Amatil