Professor Magali A. Delmas, University of California, Los Angeles

Key findings

- A firm may be rewarded by the market for how it manages potential environmental outcomes rather than its actual environmental impact.

- Disclosure raises issues since a firm may have good internal processes, such as reporting yet produce significant amounts of pollution.

- The relationship between a firm’s environmental and financial performance may vary over time. Proactive environmental strategies may be rewarded only over longer term horizons, and in the short term incur a cost.

- Data quality and availability are poor; researchers prefer data required by regulatory mandate that is transparent and standardised.

Magali Delmas’ keynote presentation was based on two recent academic studies conducted with Dror Etzion and Nicholas Nairn-Birch, which questioned whether more Corporate Social Responsibility (CSR) information adds value. Researchers have identified 50 distinct rating approaches, and a third of them have emerged since 2005. The interest and demand for CSR data comes from responsible investors as well as the complexity of defining what social and environmental corporate performance is. Without a universally agreed approach, each provider uses its own proprietary assessment. Yet, does all of this additional information help investors make better decisions?

As a proxy for CSR, Delmas et al. use corporate environmental performance ratings since data are more available and quantifiable.

Their research questions include:

- What do CSR ratings actually measure? Research result: Internal processes, i.e. management systems and external outcomes, such as impact on the environment

- What aspect of CSR does the market respond to? Research result: Internal processes

- When do CSR investments pay? Research result: Over the long term

What do CSR ratings actually measure?

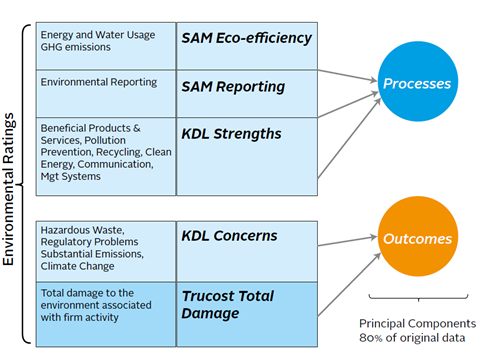

In the first study, Delmas et al. examine data from 475 US companies over a four year time period from 2004 to 2007. The environmental performance data are provided by three organisations: Trucost, KLD Analytics, and Sustainable Asset Management (SAM).

Results show the various environmental performance variables map into two components that explain 80% of the variance in the data. This implies the two components that CSR ratings actually measure are:

Processes

- The process oriented component measures internal management activities that are intended to improve environmental outcomes.

Outcomes

- The outcome oriented component measures the actual corporate environmental impact.

What aspect of CSR does the market respond to?

Next, Delmas et al. assess the relationship of processes and outcomes to financial performance. Only process based measures indicate a positive link, implying the market rewards a firm for efforts but not necessarily results. Cynically, this could mean firms could set up detailed policies and environmental management systems but not focus on how successful they are at mitigating pollution or improving water and energy utilisation.

In addition, when the rating components were evaluated individually (e.g., SAM Eco-efficiency, SAM Reporting, etc.), only one element had a significant link to performance. This could imply there is just too much ‘noise’ in the data - more information does not add more value.

Implications of the research include:

- Process based information may be preferred because it is easier to communicate and evaluate than outcome based information, which is difficult to collect, assess and rank.

- Data quality and the time lag of outcomes based measures may be an issue. Data on environmental impacts may be several years old, for example, toxic release information from 2012 just became available.

- Ratings methodologies may be incorporating more process based measures because of accessibility, with the effect of process based measures influencing market valuation.

- Disclosure on its own is not a panacea. Companies may stand out because of governance, reporting and environmental management systems, but produce a significant amount of pollution.

- Analysis of social data is expected to yield similar results, i.e. data will aggregate into processes and outcomes and process based measures will link to financial performance. This result may be even greater with social data compared to environmental data, due to the complexity of quantifying social performance results - the mere existence of policies to protect workers does not prevent abuses.

Delmas et al. acknowledge that more research needs to be carried out on what information investors use, how they use it and how investors respond to different types of CSR data.

When do CSR investments pay?

The relationship between a firm’s environmental and financial performance may vary over time. In the second study, environmental performance and practices of 900 firms were analysed over a five-year period from 2004 to 2008. Leading providers supplied data on environmental practices, environmental performance, and financial returns, respectively. Results showed a negative relationship between environmental and financial performance in the short-term, whereas the long-term horizon yielded a positive impact. This results suggests that CSR investments will pay off in the long term.

Delmas et al. suggest a short-term oriented corporate manager will forego long-term benefits in order to save money today. On the other hand, a more forward-looking corporate manager may have an incentive to invest in necessary resources and skills now, in order to gain a competitive advantage in the future.

Knowledge surrounding how asset managers react to ESG data within their investment processes and what information is being valued is limited. Delmas suggests field experiments and simulations to better understand investors’ behaviors.

Download the issue

-

RI Quarterly Vol. 5: Highlights from the PRI Academic Network Conference 2014

November 2014

RI Quarterly Vol. 5: Highlights from the PRI Academic Network Conference 2014

- 1

- 2

- 3

- 4

- 5

- 6

Currently reading

Currently readingCSR ratings: does more information add more value?

- 7