An implication of both the consideration of the corporate perspective on engagement, and a broader definition of value, is the reconsideration of how engagement success is defined.

Companies, like investors, consider the success or failure of a particular engagement in relation to specific criteria that reflects their own goals and interests. This criteria may be related to their own organisation (corporate-centric criteria), or to the investor that engages them (investor-centric criteria).

Hence, following and extending the logic of the three dynamics of value creation presented earlier, we can identify:

- A communicative dimension of success that corresponds to information exchange;

- A knowledge-based dimension of success that reflects the learning opportunities engagement enables;

- A political dimension of success that points to transformation of behaviour obtained through the relationship-building activities of actors involved in engagement.

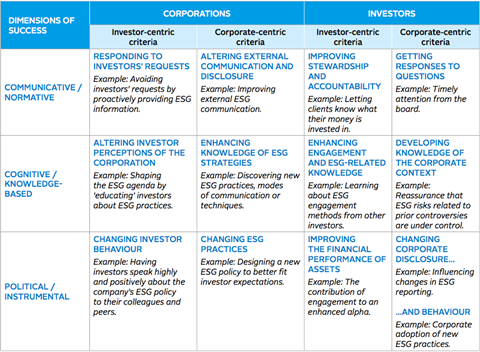

Table 2 maps these dimensions of success while considering their focus (i.e. corporate centric vs. investor centric) for both corporations and investors. The table sheds light on important differences between corporate and investor perceptions of what makes engagement successful.

Indeed, Table 2 suggests that the communicative dimensions of success only constitute one of the avenues used by actors to gauge engagement success. Some interviewees consider that success is simply “when investors are happy with the answer”, and regard a situation where engagement does not take place as successful, because “all the required ESG information is already externally communicated”. Ironically, one interviewee commented that success could be defined as “when investors are satisfied with the answer and do not come back with questions”. Such answers justify the fear that some corporations approach ESG engagement as a box-ticking exercise (VBDO, 2014).

Yet, these concerns cut both ways. Several corporate interviewees said that some investors were not necessarily interested in their business model and process, but just wanted to check their internal framework to demonstrate that they had completed their due diligence. On the investor side, this potentially superficial dynamic consists of getting answers to specific questions, without trying to learn much more through the engagement process. Such an approach is unlikely to improve stewardship and deliver robust accountability to beneficiaries or clients.

Furthermore, our research suggests that engagement provides learning opportunities beyond enhanced communication, which in turn suggests that a broader definition of engagement success is needed. Strikingly, investors and corporate interviewees alike tend to regard a successful engagement as one in which they have “learned something new”, that can help them to advance, for example, their practice of engagement (investor side), the management of ESG issues (corporate side), or their knowledge of an ESG issue associated with a specific controversy or industry (both sides).

More interestingly, our results reveal that the improved knowledge of the corporate context that is often mentioned by investors as an important criteria of successful engagement (see, for example, O’Sullivan & Gond, 2016), relates directly to the possibility of developing a genuine two-way discussion about the ESG issues at stake.

“I really appreciate when I meet an investor who’s done some homework beyond just reading articles or some sound bites, which are usually very negative towards us. Then you have a more meaningful discussion. It’s a much better use of our time if they’ve done a little bit of background work we and we can really get into the issues.”

SD& IR, Agribusiness, Asia

On the corporate side, the enhancement of ESG knowledge therefore seems to depend closely on investors’ efforts to add to their own ESG understanding. Here, a ‘virtuous cycle’ of ESG knowledge production may be triggered which serves both parties, provided that the learning opportunities inherent in engagement are recognised by both sides.

In addition, some companies define success as having altered the perception or evaluation of their ESG practices by investors. Several interviewees operating in companies that are well-advanced regarding ESG issues consider engagement as a way to ‘educate’ investors and the market in general about specific ESG issues, and the best approaches to addressing these issues.

“Educating ESG investors on a topic, and what’s involved from a business perspective, helps them understand that solutions tend to be more collaborative than win/lose. They’re more a negotiated outcome versus somebody wins and somebody loses.”

SD, Food processing & retail, US

For some of our interviewees, a successful engagement is when investors are sufficiently impressed to communicate externally about the corporations’ ESG practices. Following this logic, ESG engagement may not only produce an expected change on the corporate side, in relation to ESG practices, for example, but can also be regarded by companies as a way to influence investor behaviour. Accordingly, investors can become a ‘corporate ambassador’, speaking positively about the ESG practices of the corporation to their colleagues and peers.

For a small number of corporate interviewees, this view of successful engagement justifies a shift from a reactive to a proactive approach to ESG engagement, for example through the creation of a dedicated position bridging the investor relations and sustainability functions, and the proactive targeting of long-term and/or ESG investors as relevant capital providers.

Table 2. Contrasting Corporate and Investor Perceptions of Engagement Success

Download the full report

-

How ESG engagement creates value for investors and companies

April 2018

How ESG engagement creates value for investors and companies

- 1

- 2

- 3

- 4

- 5

- 6

- 7Currently reading

(Re)defining engagement success

- 8

- 9

- 10