These documents covering multi asset classes with a deep dive into equity markets show the detailed analysis modelled by Vivid Economics and the implications for portfolio construction and engagement. The analysis shows that investors need a thematic flexible approach to portfolio construction if they are to maximise return through the transition, building new tighter integration between engagement, company level analysis and portfolio construction. The conclusions have major implications for traditional strategic asset allocation and how asset owners in particular need to involve their entire suite of service providers in helping to build solutions.

Investors can learn how the IPR framework links its key components from the geo-political, institutional and technological drivers of an acceleration through to the asset valuation results. The summary shows the high level asset class results and summarises the portfolio construction challenges for investors.

Review of the IPR elements

Asset owners and diversified investors will be keen to understand how a disruptive acceleration of the transition impacts various asset classes. Each asset classes uses a different bottom up methodology to calculate the liabilities imposed by the forecast policies and then to calculate the net competitive position of the companies and assets in each asset class.

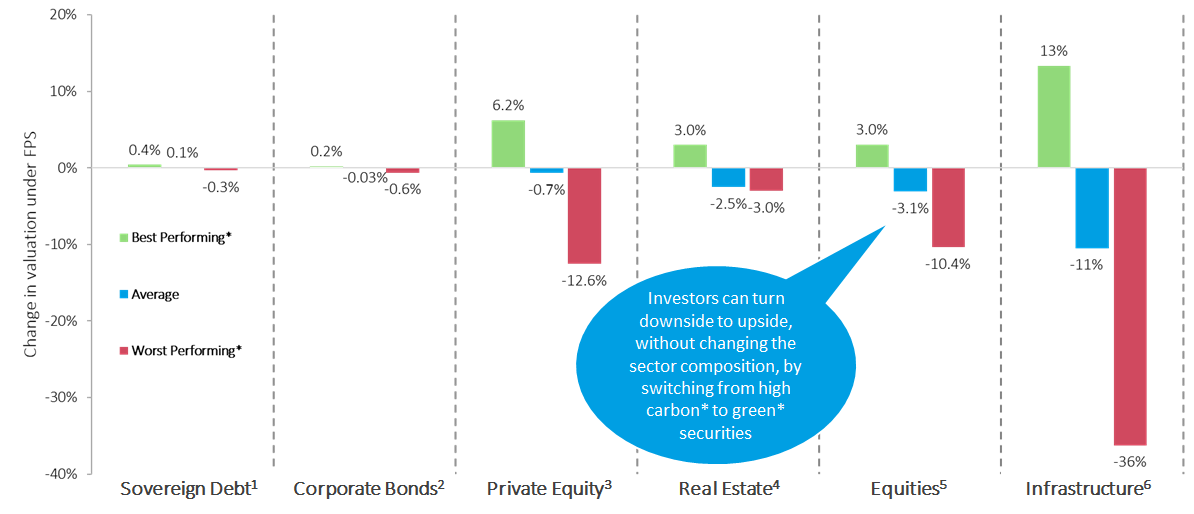

Quantitative results: the big opportunities are by tilting portfolios towards greener options within asset classes - especially in green infrastructure

Diversified sophisticated investors who conduct strategic asset allocation can see how an inevitable policy response challenges traditional techniques and creates a drive for more flexible portfolio construction methods. The analysis shows what options are available for investors seeking to look forward at transition risk rather than relying on historical data.

Investors can see how a “Capital Recycling” approach will yield optimal results whilst highlighting the challenges of adjusting allocations in each asset class for a single thematic issue.

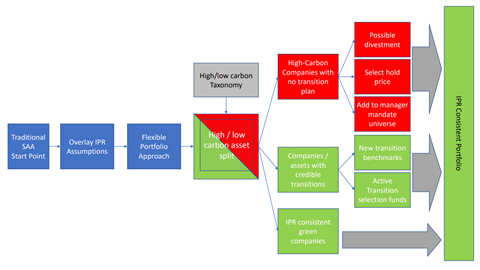

Implications for Portfolio Construction (PDF)

Critically, IPR shows how investors will need to conduct additional work to integrate company level analysis for those companies in transition into their investment selections This requires deeper analysis at company level such as the work done by Carbon Tracker using IPR. This has important implications for company engagement strategies. Investors will need to ask:

- Which companies have credible transition strategies?

- Which companies do we believe will implement those transition strategies successfully?

- Which companies will successfully transition or show strong progress towards transition before markets reprice assets around 2025?

Asset owner thematic strategy

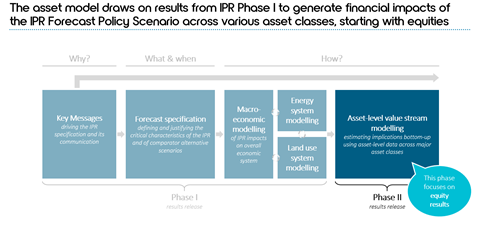

This report is a core component of the Inevitable Policy Response (IPR), a pioneering programme which aims to prepare financial markets for climate-related policy risks. What is “Inevitable” is a further policy response as the realities of climate change become increasingly apparent. The key questions for investors are when this response will come, what shape it takes, and where the impact will be felt. The first phases of the IPR laid out the policies that are likely to be implemented up to 2050, and modelled their impact on the real economy, tracing detailed effects on all emitting sectors in the Forecast Policy Scenario (FPS). This report marks the next phase, taking the FPS results to the financial market level by modelling the impacts on the MSCI ACWI equities[1] and, in early 2020, other asset classes such as fixed income, real estate and infrastructure.

The IPR will provide investors with an essential tool to assess the resilience of their portfolios against a late and forceful climate policy response. At the same time, investors must continue to advocate and engage for earlier and more ambitious climate action to minimise the disruption from a disorderly transition and from physical impacts resulting from global mean temperatures exceeding 1.5°C.

Large spread between stock-market winners and losers

The analysis shows that these critical policies could permanently wipe between 3.1 and 4.5 percent or $1.6tn to $2.3tn off the valuation of a range of companies in the MSCI ACWI index, depending on the timing of repricing. One in five companies are impacted by at least 10% in either direction. The impact is equivalent to the largest 12 to 33 companies on the FTSE100.

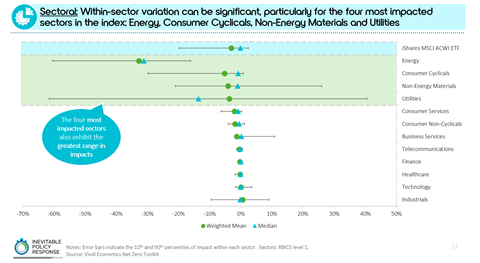

Although overall equity market impacts appear manageable, this masks substantial disruption at the sector and company level that is extremely significant for investors, as major winners and losers emerge between and within key sectors including energy, automobiles, utilities, minerals, and agriculture. For example:

Key findings

- The 100 worst performing companies in the MSCI ACWI lose -43 percent of their current value, equivalent to $1.4tn

- The 100 best performers would gain 33 percent of current value, equivalent to $0.7tn.

- Automakers with the highest investments in EVs could see their value increase by 108 percent

- World’s largest listed coal companies could halve in value (-44 percent)

- The ten largest companies in the integrated oil & gas exploration & production sector by market cap lose nearly a third (31 percent) of current value, or $0.5tn

- Electric utilities with the strongest strategy for renewables could see valuation double (104 percent), while laggards could see valuations fall by two-thirds (-66 percent)

- Miners producing minerals critical for the transition see a 54 percent upside, while those with the smallest share of “green minerals” see valuations halve (-49 percent)

- Agricultural companies with high exposure to sustainable biofuels and production of non-beef protein sources, for which demand is growing, experience gains of at least 10 percent of current value. Those companies heavily exposed to sectors in decline, such as cattle, lose more than -15 percent, with exposure increasing to as much as -43 percent for companies directly associated with deforestation owing to additional legal liabilities, loss of market access, and consumer pressure.

- For downstream food and beverage companies, emerging data about supply chain exposure to deforestation suggests that the potential value loss from these compounded risks could be up to -15 percent.

It is important to note that the financial impacts could be greater still. Our forecast also does not include other important risks, such as physical damage from climate change or the kind of financial contagion which often accompanies other major re-pricing events.

What this means for investors – act now

This analysis underscores the extent to which markets are underpricing climate transition risk. That is why the PRI are calling on investors to get real on climate policy risk, and this robust modelling exercise and analysis will enable them to do that, providing our signatories with a tool to understand how their own portfolios are positioned for an abrupt transition and then take action accordingly. Crucially, investors need sector-level analysis and the IPR: Forecast Policy Response provides this.

- Invest: investors can incorporate an IPR into investment processes, sector analysis to inform portfolio construction, including identification of potential winners and losers. The IPR results enable investors to consider how well-positioned their portfolio is and encourages further analysis by investors to feed into investment decisions.

- Engage: investors need to engage companies in sectors operating under business as usual on what their assumptions are and the extent to which they have factored in an IPR; asset owners need to engage managers and all players in the investment chain on what assumptions they are working to and encourage them to incorporate IPR-like thinking. Investors should also ensure the alignment of businesses with the Paris Agreement across the whole value chain and ensuring that lobbying practice – including via trade associations – is aligned with investors’ interests in an orderly transition to net zero as soon as possible.

- Policy advocacy: investors need to step up in pressing governments to act now, not later, on the Paris Agreement, including adopting the key policy levers identified in IPR. Investors can draw on the IPR policy levers and analysis at a regional and sector level.

- Disclose: investors need to disclose how they assess climate risks, drawing on TCFD. Investors need to disclose on how their boards undertake forward-looking climate risk assessment to test the resilience of investment strategy, as per the TCFD recommendations. IPR, alongside Paris Aligned scenarios, offers a way to engage boards and apply forward-looking climate risk assessment, enabling good practice investor disclosure.

PRI will be running a programme to support investors in how to do this, to get involved contact us at [email protected]

A fully integrated modelling framework from policy to financial markets

Value add of the Forecast Policy Scenario (FPS)

- A high conviction policy-based forecast, not a hypothetical scenario that optimizes policy to meet a temperature constraint

- Transparent: on expectations for policy and deployment of key technologies, such as Negative Emission Technologies

- Complete: covers macroeconomic, energy system, and land use models linking crucial aspects of climate risks across the world with detailed results for key regions such as Western Europe, US, Brazil, China, India, Canada, Australia and Japan

- Fully integrating land-use to ensure the full system impacts of policies, and highlight the critical role of nature-based solutions and the land-use system

Equity Portfolio Sensitivity Tool

This tool allows investors to compare their own sector loadings and calculate the valuations differences against an MSCI ACWI benchmark.

Portfolio Sensitivity Tool (XLS)

Data Tables

Some investors may have their own valuation models and so IPR provides key macro outputs that can be adjusted to tailor assumptions that are fed into in-house valuation models.

Downloads

Inevitable Policy Response - Investor Summary - July 2020

PDF, Size 1.69 mbInevitable Policy Response - Asset Class Impacts - July 2020

PDF, Size 3.86 mbInevitable Policy Response - Implications for Portfolio Construction - July 2020

PDF, Size 0.92 mbImpacts of the Inevitable Policy Response on Equity Markets - December 2019

PDF, Size 3.84 mbIPR Portfolio Sensitivity Tool

Excel, Size 80.5 kbIPR Equity Results

Excel, Size 31.64 kbIPR Data Tables

Excel, Size 76.53 kb

Websites

References

[1]The analysis uses the iShares MSCI ACWI ETF as representative of the MSCI ACWISummar