(Updated October 2021)

- The US Presidential election and the Net Zero China 2060 target in particular show the “inevitability” of policy response to climate change. Exactly what, when and how remains the issue. In March 2021, we updated our core Policy Forecasts from 2019 and considered potential accelerations as well as implications for investors.

- We updated these forecasts again in October 2021 to reflect developments leading up to COP 26 and also detailed the importance of just transition considerations.

- Many of the policy developments during the latter half of 2021 confirmed our earlier March policy forecasts and there were no significant changes in terms of global emissions implications.

- As net zero commitments accelerate across the globe, our updated IPR 2021 Policy Forecasts outline the policies that are expected to be deployed by 2025 to begin meeting those targets.

- Forecasts offer markets and institutional investors the crucial next layer of detail on when, where and how these commitments will start to shift the macroeconomic context through forceful policy implementation across a range of key policy levers.

- The IPR policy maker toolbox is growing and policy makers will build on carbon pricing, coal phase outs and ICE bans and increasingly set ambition in policy to address hard to abate sectors such as industry and agriculture

- Carbon Border Adjustment Mechanisms (CBAM) were core to our 2019 forecast and are now widely discussed and closer to implementation

- Corporations themselves are creating their own “policy” or strategies around Net Zero and certain industries such as Autos are moving ahead of government policy.

- The US infrastructure package favouring low carbon has been reduced but is prioritising climate related proposals.[1] Even if watered down somewhat we see regulatory and state action as maintaining momentum.

- The run up to COP26 in Glasgow in November has seen the US and other countries, raise ambition in submitted NDCs.

- IPR has used the Paris Agreement Ratchet framework for milestones on policy announcements. COP26 is in effect the delayed 2020 Ratchet. Hence it is not expected to deliver the full IPR Forecast suite. The next significant event in the Paris process is the 2023 Global Stocktake on the way to the 2025 Ratchet.

IPR Policy Forecast (summary)

IPR climate policy acceleration

IPR Investor Summary Brief – March 2021 / Updated October / Dec 2021

In 2019, the PRI commissioned a ground-breaking analysis of inevitable policy responses by governments around the world, to meet the 1.5 degrees Paris ambition. We released a paper outlining these policies, which along with the IPR 2019 Forecast Policy Scenario, lead to some of the world’s largest institutional investors and financial institutions committing to using it as a scenario. In 2020, we did it all again.

The IPR 2021 policy forecast released October 2021 is a thoroughly revised and updated set of policy forecasts, reflecting even further detailed research on current and proposed policies, with input from a global survey of policy experts.

The questions for risk forecasting are when and how this acceleration in response will come, what policies will be used, and where the impact will be felt. IPR 2021 forecasts responses by 2025 that it will be forceful.

Why is it inevitable? The need to act on climate is pressing

- The need to act on climate is rising up the policy agenda

- Climate action will create substantial shifts in global investment needs, driving down demand for assets that increase emissions, and driving up demand for assets that avoid or reduce them

- Financial markets today have not adequately prepared for the likely policy response to climate change.

What is the IPR2021 policy forecast and what does it do?

- A high-conviction policy-based forecast of forceful policy response to climate change and implications for energy, agriculture and land use

- Identifies key sources of climate policy-driven opportunity and risk in these sectors

- Prepares investors to better manage exposure to these risks in their portfolios

IPR 2021 forecasts higher policy ambition across eight key policy levers

Markets have been highly volatile in the past year and determining what has been priced in or not sector by sector is complex. In the longer term the trends set out in the IPR FPS remain crucial for portfolio construction.

What makes IPR2021 different to other forecasts?

- Future energy scenarios typically provide either business-as-usual trends or idealized futures in which climate action is immediate, gradual, and coordinated.

- While investors agree that the policy response will be delayed, abrupt and disruptive, few scenarios map out the implications of such a future

Through a robust real-world analysis that works up from the policy and technology developments that are already in place as well as those which are most likely to emerge, we forecast a number of key climate-related policy developments.

In short, IPR 2021 shows the policies which will have significant implications for the real economy and society within the near term.

The summary and detailed papers outline and explain the basis of the forecast, details the expected policies and outlines when they will come into effect in each of 21 countries representing 78% of economic activity, 74% of energy use and 77% of CO2 emissions.

IPR 2021 top ten policy forecasts

| Carbon pricing | 1 | Carbon Border Adjustments Mechanisms (CBAMs) for carbon will become increasingly a policy option. This could lead the United States to announce a national carbon pricing system by 2025, and signal a strong carbon price path to reach a backstop of $65 by 2030. |

|---|---|---|

| 2 | The European Union’s evolving commitments will deliver substantial carbon prices. By 2030, we expect EU policy to backstop an EU ETS carbon price of $75/tCO2 to ensure longterm action toward decarbonization in heavy emitting sectors. | |

| Coal | 3 | In India, rapidly evolving Indian policy and prospects for market reforms and pricing has already ended further investment in new coal. |

| 4 | China will end construction of new coal fired power production after 2025, driven by new policies to facilitate its 2060 net zero target and ongoing market liberalisation. | |

| 5 | The United States will end all coal-fired power generation by 2030, through a combination of emission performance standards and carbon pricing at the Federal and State levels, combined with market forces. | |

| Clean power | 6 | The United States will implement a binding and credible 100% clean power standard for 2040, ending unabated fossil electricity generation. |

| Zero Emission Vehicles | 7 | China, France, Germany, Italy and Korea will end the sale offossil fuel cars and vans in 2035. Jointly these largemarkets will accelerate the auto industry transition toelectric drive, and precipitate further policy actioninternationally. |

| Industry | 8 | All major industrial economies including the US, Germany,Japan and China will require all new industrial plants, ledby steel and cement, to be low-carbon by 2040, through acombination of emissions performance standards and carbonpricing. |

| Agriculture | 9 | The US, Canada, Australia and other major agriculturalproducers will have comprehensive mitigation policy in placeby 2025 to reduce emissions from production of crops andlivestock.pricing. |

| Land use | 10 | Major tropical forest countries will end deforestation by 2030, with domestic policy responding to internationalclimate finance and corporate supply chain pressures. |

2020: A year of big movement in climate policy

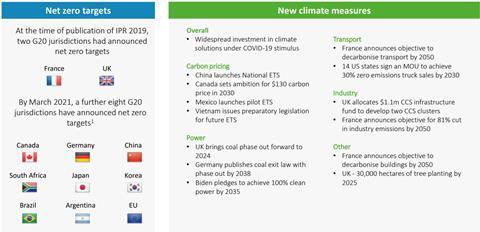

Since our landmark IPR 2019 policy forecast, governments around the world have realised just how urgent stringent and robust climate policy action needs to be to avert the dramatic effects of climate change which we are already witnessing today. A number of countries, cities and corporates have pledged ‘net zero’ emissions and a host of other climate policies have been implemented including even more countries committing to phasing out coal from their power system, banning the sale of ICE vehicles and even more ambitious carbon pricing regimes.

Since 2019, major net zero commitments and new climate measures in leading countries have raised prospects for an accelerated policy response

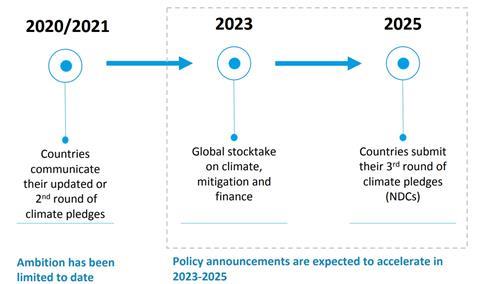

2021-2025: Pressure Grows

Although 2021was a big year, the Paris Agreement ‘ratchet mechanism’ – starting with the Global Stocktake 2023 and leading to the third round of climate pledges in 2025 – will put further pressure on policy makers to tackle climate

This pressure for policy action will continue to increase and come from all angles – environmental, social, and economic. Upward pressure will come from electorates and businesses and be further fuelled by fears over national security. Perhaps most critically, such a rapid policy shift is further enabled by advances in technology cost and performance, and the drive by major economies to lead in these emerging industries.

Timing: Paris Ratchet process triggers a cumulating policy response into 2025 Growing awareness of climate issues and an international framework for accelerating action, with added energy security impetus makes forceful policy responses likely

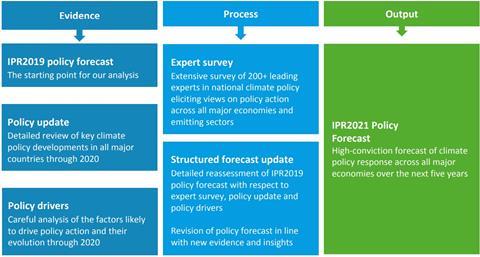

A bottom up, granular and transparent approach

In 2020 and 2021, a team of researchers at Vivid Economics in collaboration with Energy Transition Advisors and climate policy experts across the consortium, undertook research that followed a robust and transparent approach along the following principles:

Our approach to Forecasting

- Focussed on 21 countries (G20, splitting up EU and adding Nigeria and Vietnam) representing more than 75% of global GDP

- Grounded in an expansive qualitative and quantitative analysis of recent announcements, commitments, initiatives and trends in each region

- Underpinned by transparent and realistic assessments of likely policy developments based on an expert survey for each of the 21 countries built over 9 months and with over 200 global policy experts participating across all countries

The IPR2021 Policy Forecast was informed by a rigorous evidence review and large-scale survey of country climate policy experts

Downloads

IPR 2021 Policy Forecast - Executive Summary

PDF, Size 1.61 mbIPR - climate policy acceleration

PDF, Size 0.71 mbIPR 2021 Policy Forecast – Detailed Resource

PDF, Size 4.16 mb

References

[1]April 2022 update: The $1.2 trillion bipartisan Infrastructure Investment and Jobs Act was passed on November 5, 2021 and includes $7.5 billion in investments for electric vehicle infrastructure and $65 billion in clean energy transmission and the grid.

Topics

What is the Inevitable Policy Response?

- 1

- 2

- 3

Currently reading

Currently readingThe Inevitable Policy Response 2021: Policy Forecasts

- 4

- 5

- 6

- 7