A Climate Transition Forecasting Consortium

What is IPR

The Inevitable Policy Response (IPR) aims to prepare institutional investors for the portfolio risks and opportunities associated with a forecast acceleration of policy responses to climate change. IPR contends that governments will be forced to act more decisively than they have thus far, leaving financial portfolios exposed to significant transition risk.

Commissioned by PRI in 2018, IPR is led by Vivid Economics and Energy Transition Advisors (ETA). Combined with Research Partners and investor Strategic Partners, this forms the IPR Climate Transition Forecasting Consortium.

Acceleration, Ratchets and Implications for Investors

Government action to tackle climate change remains insufficient to achieve the commitments made under the Paris Agreement. Yet as the realities of climate change become increasingly apparent, it is inevitable that governments at national and international levels will be forced to act more decisively than they have so far.

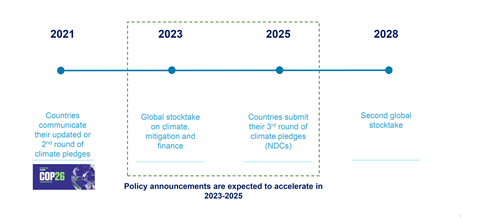

IPR forecasts general acceleration in policy responses to 2025, driven in part by continuing pressure for change, increasingly evident at multilateral fora and again at COP 26 and expected at the 2023 Stocktake and the 2025 Ratchet.

Disorderly Transition

IPR assesses that those policy responses will increasingly be forceful, abrupt, and disorderly leaving financial portfolios exposed to significant transition risk.

To help prepare markets and institutional investors for the impacts of this policy acceleration and a disorderly transition IPR models in detail the impact of the forecasted policies on the energy system, food & land use system and real economy.

This acceleration and general implications for investors is set out in the in the Forecast Policy Scenario (FPS).

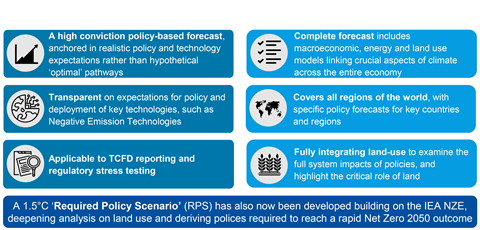

IPR has also published a new 1.5C Required Policy Scenario (RPS) outlining the more ambitious policies that would be required to reach a 1.5C outcome.

Ratchet pressures increase the likelihood that governments will strengthen policy by 2025 and again to 2030

Paris Ratchet process triggers a cumulating policy response into 2025

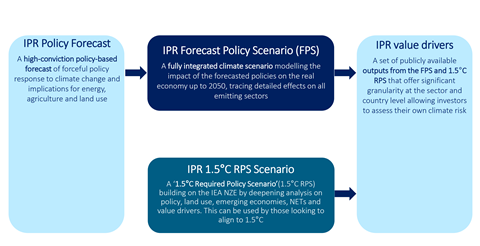

The Forecast Policy Scenario (FPS)

Built by Vivid Economics and Energy Transition Advisors, the 2021 Forecast Policy Scenario (FPS) lays out the major climate policies that are likely to be implemented in the 2020’s and quantifies the impact of this response on the real economy and various sectors.

IPR publishes detailed modelling of the impact of policy acceleration:

- On key sectors, regions;

- On the implications for energy, land use; and

- On the macroeconomy

Investors should act now to protect and enhance value by assessing the implications of the IPR Forecast for investment beliefs, portfolio risk and identification of opportunities.

The greater the delay in responding, the greater the potential cost.

IPR’s Forcast Policy Scenario (FPS) value data

What makes the IPR FPS unique?

The FPS provides investors with a unique tool for navigating a complex, evolving policy and regulatory landscape – to enhance portfolio resilience and inform strategic asset allocation.

The FPS:

- Provides a realistic outline of the coming policy response through the 2020’s and quantifies the financial risks that it presents

- Is based on working up from what policy and technology developments are most likely to emerge, rather than working backwards from pre-defined target temperatures

- Focused on a timeframe that is relevant to investors

- Models the interaction between impacts of the macro economy, the energy system and the land use system

- Provides a granular analysis that breaks down the impact at the regional, sector and – for the first time – asset level

Our forecast of an Inevitable Policy Response provides an alternative to the IEA STEPS as a business planning case for investors, corporates & regulators to consider

IPR range of applications

The 2021 Forecast Policy Scenario (FPS) is IPR’s current assessment of what is anticipated to happen, in terms of future policy developments and the subsequent impact on emissions reduction and temperature outcomes. If all the forecast acceleration in policy and execution takes place the 2021 FPS assesses a 50% probability of holding temperature increase to 1.8C.

Pressure, stocktakes and ratchets

As discussed in our March 2021 Policy Acceleration paper, governments have been moving faster in the last 18 months. The November COP 26 in Glasgow has added momentum to policy announcements.

But a significant gap remains between potential emissions reduction impacts and holding temperature increase to 1.5C. Future policy responses will be needed to address this gap.

Pressure for policy action will continue to increase and come from all angles – environmental, social, and economic - fuelled by fears over national security; enabled by advances in technology and upward pressure by civil society, leading investor groups and businesses to act.

Far more so than in the past, these triggers for action are aligning actors in a common direction.

At the same time, the Paris Agreement ‘ratchet mechanism’ – boosted by outcomes in Glasgow around nations reviewing 2030 targets and subject to the scheduled Stocktake in 2023 and 2025 Ratchet, will increase the likelihood that policy announcements to tackle climate change will accelerate through to 2025. This is the focus of the 2021 FPS.

Forecasting the acceleration: Higher ambition- eight key policy levers

IPR has forecast higher ambition across eight policy levers to secure an accelerated and just transition. Multiple announcements at sub national, national and international levels through 2021 and at COP26 at reflect this higher ambition.

- Carbon taxes

- Emissions trading systems

- Border carbon adjustments

- Prohibiting regulations

- Emissions performance standards

- Electricity market reforms

- 100% clean power targets

- Renewables capacity auctions and other support policies

- 100% zero emission vehicle (ZEV) sales legislation

- Manufacturer ZEV obligations

- ZEV consumer subsidies

- Prohibiting regulations for fossil heating systems

- Purchase subsidies for low-carbon heating systems

- Thermal efficiency regulations for new build and retrofit

- Minimum energy performance standards for new appliances

- Emissions performance standards for industrial plant

- Subsidy for new or retrofit clean industrial process

- Methane or nitrous oxide emissions tax or cap-and-trade system

- Subsidy for low-emissions agricultural practices and technologies

- Farmer education and technical assistance programmes

- Strong policy action against deforestation, such as monitoring and penalties, supported by consumer pressure

- Incentives for reforestation and afforestation via domestic action and carbon markets

‘Just Transition’ lens to ensure social and political feasibility

Forecasting the acceleration: Top 10 forecasts of where the impact will be felt

IPR analyses in detail the policies we expect to see implemented and where they will have impact.

They include bans on coal, and on internal combustion engines; an increase in nuclear capacity and bioenergy crops; greater effort on energy efficiency and re/afforestation; wider use of carbon pricing including Carbon Border Adjustment Mechanisms (CBAM) and increasing the supply of low-cost capital to green economy projects.

|

Carbon pricing |

1. Carbon Border Adjustments Mechanisms (CBAMs) for carbon will become increasingly a policy option. This could lead the United States to announce a national carbon pricing system by 2025 and signal a strong carbon price path to reach a backstop of $65 by 2030. |

|

2. The European Union’s evolving commitments will deliver substantial carbon prices. By 2030, we expect EU policy to backstop an EU ETS carbon price of $75/tCO2 to ensure long-term action toward decarbonization in heavy emitting sectors. |

|

|

Coal |

3. In India, rapidly evolving Indian policy and prospects for market reforms and pricing has already ended further investment in new coal. |

|

4. China will end construction of new coal fired power production after 2025, driven by new policies to facilitate its 2060 net zero target, geopolitical trends and risk considerations* |

|

|

5. The United States will end all coal-fired power generation by 2035, through a combination of emission performance standards and carbon pricing at the Federal and State levels, combined with market forces. |

|

|

Clean power |

6. The United States will implement a binding and credible 100% clean power standard for 2040 ending unabated fossil electricity generation. |

|

Zero emission vehicles |

7. China, France, Germany, Italy and Korea will end the sale of fossil fuel cars and vans in 2035. Jointly these large markets will accelerate the auto industry transition to electric drive, and precipitate further policy action internationally. |

|

Industry |

8. All major industrial economies including the US, Germany, Japan and China will require all new industrial plants, led by steel and cement, to be low-carbon by 2040, through a combination of emissions performance standards and carbon pricing. |

|

Agriculture |

9. The US, Canada, Australia and other major agricultural producers will have comprehensive mitigation policy in place by 2025 to reduce emissions from production of crops and livestock. |

|

Land use |

10. Major tropical forest countries will end deforestation by 2035, with domestic policy responding to international climate finance and corporate supply chain pressures. |

Closing the gap to 1.5C: The Required Policy Scenario (RPS)

Even with this rapid transformation, the forecasted changes in the FPS would not yet be enough to keep warming to 1.5C – the temperature scientists have shown to be critical to avoiding the worst impacts and most costly effects of climate change.

To bolster policy advocacy around the world and help prepare the $90 trillion of banks and investors committed to align with net zero by 2050 ambition, the IPR has developed the new 1.5C Required Policy Scenario (RPS).

IPR 1.5°C RSP:Summary

The 1.5°C RPS details future policy developments needed to accelerate emissions reduction and hold global temperature increase to a 1.5 °C outcome

Despite rapid transformation, the IPR FPS 2021 changes would still not be enough to hold warming to 1.5°C with Net Zero in 2050, which requires greater action, sooner. Key actions to pursue a 1.5°C outcome include:

- A rapid end to deforestation across the entire globe, ideally by 2025 and before 2030. If not, the energy system has to absorb greater reductions, potentially through bioenergy with CCS (BECCS)

- Crucially, unabated coal fully decommissioned in most advanced economies including China by 2035

- Phase out new fossil cars in almost all markets by 2040 and transition to 100% clean power globally by 2045

The 2021 1.5C RPS calls for much more ambitious policy action over and above what is forecast. The 1.5C RPS specifically targets a 1.5C outcome and reflects the policy gap between the FPS forecasts of what will happen and the level of policy change required to hold temperature increase at a 1.5C outcome.

The 1.5C RPS is comparable to the IEA Net Zero Emissions (NZE) Scenario, but by deepening the analysis of the food and land systems provides the first roadmap of policies needed across both the energy and land use systems to hold temperature increases to 1.5C.

In the FPS, rising carbon prices play a key role in driving change through the economy. But analysis suggests it would not be politically feasible to drive carbon markets and carbon pricing further, and rapidly enough to achieve the required shift.

Accordingly, to push for 1.5C, governments around the globe would need to pursue immediate policy action which directly intervenes in markets to set performance standards, including strict bans, to drive a step change in the energy system:

- Phase out new fossil cars in almost all markets by 2040.

- Transition to 100% clean power globally by 2045.

- Eliminate unabated coal in most advanced economies including China by 2035.

The 2021 1.5C Required Policy Scenario (RPS) is IPR’s current assessment of future policy developments needed to accelerate emissions reduction and hold global temperature increase to a 1.5 Degree outcome.

Looking ahead: NETS in 2030s?

Failure to pursue significant policy changes within the next two to three years would leave a significant ramping up of Negative Emissions Technologies (NETS) in the 2030s as a potential alternative to keep warming to 1.5C.

But given food and land use constraints, and the fact that many technologies are unproven at scale, pushing beyond the already forecasted acceleration in Nature Based Solutions (NBS) would also require significant and urgent policy support.

IPR Investor Value Drivers Database- Support for risk, valuation and transition models

The IPR Investor Value Drivers Database encompasses all FPS variables by region annually, up to 2050, incorporating a total of 300,000 thousand data points.

It provides a direct input into the core valuation and risk models that drive investor decisions and assistance to those investors working towards integrating climate scenarios into their investment strategies.

The database enables asset managers and service providers to incorporate the IPR forecast policy scenarios and underlying short and long term data directly into their valuation models and utilise them as a basis for assessing existing investment beliefs, and determining strategic asset allocation, portfolio construction and corporate engagement strategies.

The database is open source and available as a resource for investor, policy makers and regulators.

Supporting investor action to protect and enhance value

The PRI encourages signatories to engage in forward looking analysis and strategic planning to better prepare for transition and mitigate financial losses associated with an accelerated policy response.

Careful attention is recommended for strategic asset allocation, portfolio structure, governance approaches, and risk management responses.

Specific actions include:

- Creating governance / board approval of IPR as part of the ‘house view’ of climate transition

- Preparing for a more ‘active’ stance in portfolio construction around the transition theme

- Embedding aspects of IPR forecasts into asset manager mandates with associated changes to mandate incentives

- Encouraging asset managers to build products around IPR forecasts

- Placing IPR as a core reference standard in ongoing TCFD disclosures

- Requesting asset consultants to build IPR into SAA and portfolio construction

- Requesting credit ratings agencies to incorporate IPR into assessments

- Use of IPR as a reference standard in stewardship activities and company engagement

- Lobbying policymakers on the inevitability of IPR scenarios to encourage early action

IPR Briefings

For more information on IPR, signatory briefings and presentations, please contact us at [email protected]

Downloads

What is the Inevitable Policy Response?

PDF, Size 2.34 mbIPR Scenario Descriptions

PDF, Size 0.33 mbIPR Investor Summary Brief – December 2021

PDF, Size 2.95 mbThe Inevitable Policy Response Scenarios paper - pathways to net zero June 2020

PDF, Size 2.5 mbIPR Under Biden's Climate Plan - Report November 2020

PDF, Size 1.12 mb

Topics

What is the Inevitable Policy Response?

- 1

Currently reading

Currently readingWhat is the Inevitable Policy Response?

- 2

- 3

- 4

- 5

- 6

- 7