Tax policy (organisational and board view on corporate income tax):

GSK: “We have a responsibility to our shareholders to be financially efficient and deliver a sustainable tax rate. As part of this approach, we look to align our investment strategies to those countries where we already have substantial economic activity, and where government policies promote tax regimes which are attractive to business investment, transparent in their intent and available to all relevant tax payers, such as the UK Patent Box.”

Novo Nordisk: “In line with our Triple Bottom Line approach as well as the Novo Nordisk Way, our finance policy includes the intention of ‘pursuing a competitive tax level in a responsible way’. ‘Competitive tax level’ implies achieving a tax level around the peer group average. ‘Responsible way’ implies doing business in a way that meets expectations for a good corporate citizen. This means paying taxes where profits are earned in accordance with international transfer pricing rules. It means having a balanced tax risk profile and not engaging in tax-avoidance activities, as well as keeping tax levels stable and predictable.”

Coloplast: “Coloplast sees taxes as an important part of the business as respecting local tax laws and regulations are important to Coloplast’s reputation and brand. ln addition, taxes contribute to the economic value generation in the countries where Coloplast operate. ln Coloplast, taxes are paid where business activities generate value in accordance with internationally accepted standards. Coloplast does not allow commercial needs to override compliance with applicable laws, nor base commercial activities on tax avoidance schemes. All transactions and tax structures must therefore have a business purpose or commercial rationale as a prerequisite, and Coloplast will not engage in tax planning schemes and structures, which Coloplast does not wish to divulge to the tax authorities. Within these principles, Coloplast will pursue tax opportunities if they arise and will proactively obtain knowledge in order to have a competitive effective tax rate and avoid double taxation.”

Tax governance

GSK: “Our Audit and Risk Committee, and the Board, are responsible for approving our tax policies and risk management. The tax affairs of the Group are managed on a global basis through a co-ordinated team of tax professionals, led by the Global Head of Tax, who work closely with the business. Significant decisions are submitted for consideration to the Tax Governance Board, which meets quarterly and comprises senior personnel from across GSK’s Finance Group.”

Novo Nordisk: “All employees in the global tax organisation are aligned on how to deal with taxes in Novo Nordisk and to comply with our objective of ‘pursuing a competitive tax level in a responsible way’. Employees working with tax must henceforth sign the Novo Nordisk ‘Corporate Tax Code of Conduct’’ which specifies five habits of responsible conduct.”

Sage: “The ultimate responsibility for Sage’s tax strategy and compliance rests with the Group Board who ensure that the appropriate framework is in place to oversee the identification and management of tax risk. The Chief Financial Officer (‘CFO’) is the Board member with executive responsibility for tax matters. Day-to-day management of tax affairs is delegated to the Group Tax Director who has a team of appropriately qualified individuals. The Group CFO is appraised regularly of all significant tax developments and participates in all material tax related decisions.”

Tax planning and tax risk management

Johnson & Johnson: “We have a low tolerance for tax risk and reject planning opportunities that are not in line with our values or are inconsistent with our reputation. Where uncertainty exists and when appropriate, we seek clarification from external advisors and/or governmental authorities.”

GSK: “We are not prescriptive on the level of tax risk we are prepared to accept. However, we do not take speculative tax positions where the advice received does not support our position, or those that bring material tax risk. Where there is material uncertainty on the tax treatment of a transaction, external advice is sought before any position is taken. External advisors are also required to adhere to our Code of Conduct.”

ASML: “ASML strives to report and pay taxes in accordance with all relevant tax laws and regulations. We will comply with the letter and spirit of these laws and regulations, meaning that we are committed to complying not only with the detail of the relevant laws, but also their intent.”

Taxes paid linked to commercial activity

Sonic: “Sonic Healthcare does not enter into transactions or structures without commercial substance. The only countries in which Sonic has subsidiaries are those in which we have a substantial operating business presence, in the form of clinical laboratories. These active businesses contribute to the economic growth and healthcare of their country of operation. Sonic has active laboratory operations in Switzerland and Ireland, two countries with relatively low corporate tax rates; however Sonic does not operate any international shared service or financing functions or structures in those countries.”

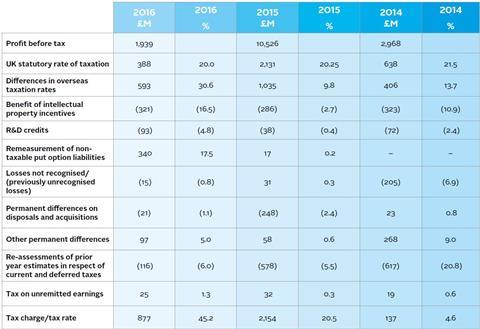

GSK: Tax reconciliation using home country statutory tax rate (see below).

Intuiti: “The Company has a tax holiday in effect for its business operations in Switzerland which will continue until the end of year 2017 to the extent certain terms and conditions continue to be met. This tax holiday provides for a lower rate of taxation in Switzerland based on various thresholds of investment and employment in such jurisdiction. As of December 31, 2016, the Company remained in compliance with the terms of the holiday. At the end of the tax holiday, Swiss taxable income may be taxed at a higher rate depending on the applicable federal and cantonal rules. Tax benefit from the Swiss tax holiday for the year ended December 31, 2016, was approximately $10.0 million, or $0.25 per diluted share.”

Align: “In order to receive the benefit of these incentives, we must hire specified numbers of employees and maintain certain minimum levels of fixed asset investment in Costa Rica. If we do not fulfill these conditions for any reason, our incentive could lapse, and our income in Costa Rica would be subject to taxation at higher rates, which could have a negative impact on our operating results.”

Download the full report

-

Evaluating and engaging on corporate tax transparency: An investor guide

May 2018

Evaluating and engaging on corporate tax transparency: An investor guide

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

Currently reading

Currently readingExamples