Case study by Caisse des Depots

| Author | Pascal Coret, Deputy Head of Portfolio Management |

|---|---|

|

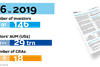

Market participant |

Asset Owner |

|

Total AUM |

US$155 billion (as at December 2017) |

|

FI AUM |

US$116 billion (as at December 2017) |

|

Operating country |

France |

Action area:

- Materiality of ESG factors

The investment approach

Caisse des Dépôts’ (CDC) emerging market (EM) sovereign debt portfolio was set up before the integration of ESG analysis in sovereign debt allocation. Like the developed market portfolio, our EM portfolio is constrained by minimum credit ratings. However, as EM sovereign bonds are more volatile and riskier than developed sovereign debt instruments, CDC realised that an increased exposure to this asset class required a broader analytical framework beyond the usual macroeconomic indicators. Indeed, a lesser level of economic development is often related to a stronger dependency of the economic structure on the primary sector, hence a bigger exposure to physical environmental risks. Furthermore, developing countries by definition do not have the same network of legal, regulatory and supervisory institutions as their developed peers, which can lead to governance issues. In the worst cases, environmental and governance issues can cause social tensions.

The investment process

In building this analytical framework, the exposure of sovereign bonds to material factors had to be identified, measured and ultimately assessed and integrated into the portfolio allocation process. We decided to develop capacity within the team of portfolio managers instead of relying on an external provider.

Our effort to build a new analytical model started with EM countries but was scaled up to cover developed issuers (which on some ESG metrics do not score better than certain developing countries).

We currently collect the time series data of 50 countries (close to the eligible investment universe) through publicly-available databases. We cover three main topics:

- governance indicators, such as government effectiveness or corruption, with a focus on female positions in society;

- social development and inequalities (Gini index, education and health); and

- the environment through indicators on forestry, energy, agriculture, water and air quality.

The data are normalised and each country is assigned a relative score for each environmental, social and governance factor. When possible, a dynamic component is also added to factor in improving (or worsening) trends. The analysis focuses on the main changes.

To adjust for the wealth effect, i.e. the correlation between a country’s revenues and its ESG performance, scores are expressed in relation to the country’s per capita real disposable income. The reasons for this are:

- to avoid only the most developed countries (with the best ESG scores) benefiting from allocations based on raw ESG scores;

- to avoid penalising the least developed countries which would otherwise be deprived of investor flows and development financing; and

- to study if the country’s development model is in line with the Sustainable Development Goals.

The adjustments also magnify the poor scores of developed countries, making the ESG underperformance even more striking.

These proprietary ESG scores complement our more traditional credit risk analysis, which is also performed internally by the team of portfolio managers, while the risk department conducts its own risk appraisal (with ESG integration).

The investment outcomes

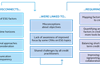

The example below shows how the CDC investment process identifies material ESG issues and how these are addressed by our portfolio managers.

Our FI team initially invested in an EM sovereign debt market based on its strong macro fundamentals (solvency, refinancing capacity, expected growth and revenues). This decision was also supported by strong rating opinions issued by major CRAs at the time.

However, despite being in the first decile of countries ranked by revenue per head, our ESG analysis left this sovereign country in a relatively low position – in the fourth bottom decile – due to relatively poor performance on some environmental (air quality, CO2 emissions and greenhouse gasses in the agricultural sector) and governance metrics (voice and accountability and gender parity). Moreover, there was no significant sign of improvement over time. As a result, our portfolio managers had reservations about the awareness and/or willingness of the ruling administration to address these ESG shortfalls, and questioned the financial performance of the country, despite its apparent soundness based on traditional financial metrics. If the risks associated with these ESG deficiencies had materialised, they would have significantly increased budgetary expenditures. This concern, coupled with the team’s concerns about potential reputational risks, represented a significant downside risk.

We therefore decided to gradually exit the entire position. The portfolio then showed a reduced geographical diversification and a slightly higher financial risk, as measured by average ratings, since the proceeds of the divestitures were reinvested in EM bonds with lower ratings. However, given further markets developments, no specific underperformance due to this reallocation could be identified.

Two major CRAs downgraded the sovereign bond issuer by one notch four to six months after CDC’s complete divestment.

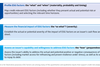

Key takeaways

Adding an ESG analytical framework to go beyond macroeconomic analysis and traditional credit risk evaluation based on financial metrics was time-consuming (particularly developing an internal ESG assessment tool). However, this investment approach paid off with enhanced risk appraisal by FI portfolio managers. The macroeconomic consequences of growing inequalities (within a given country) and exposure to climate change are examples of risk factors that are much better captured when integrating ESG parameters.

Download the report

-

Shifting perceptions: ESG, credit risk and ratings: part 3 - from disconnects to action areas

January 2019

ESG, credit risk and ratings: part 3 - from disconnects to action areas

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

- 11

- 12

- 13

- 14

- 15

- 16

- 17

- 18

- 19

- 20

- 21

Currently reading

Currently readingCase study: Caisse des Depots

- 22

- 23

- 24

- 25